Conclusion: Grade = B+ Adidas’ +14% currency neutral global growth in Q1 as well as the company’s increase to both top and bottom line full year guidance continues to demonstrate strong global demand for innovative Athletic Footwear, Apparel & Accessories.

What Drove the Beat?

Adidas’ Q1 outperformance came primarily through upside in top line expectations +17% driven by double digit growth across all business segments with North America & Asia the biggest contributors to the top line. Although Gross margins were down 70 bps in Q1, higher sourcing costs had a (-470bps) impact on the bottom line (directionally, like Nike) but was mostly offset by increased retail penetration & a more favorable product/regional sales mix. All in, Operating margins expanded +113bps as Adidas leveraged opex for the 5th consecutive quarter reaching a trailing 12 month ~8% margin relative to the “Route 2015” goal of 11%. The only real sore spot remains Reebok.

Deltas in Forward Looking Commentary?

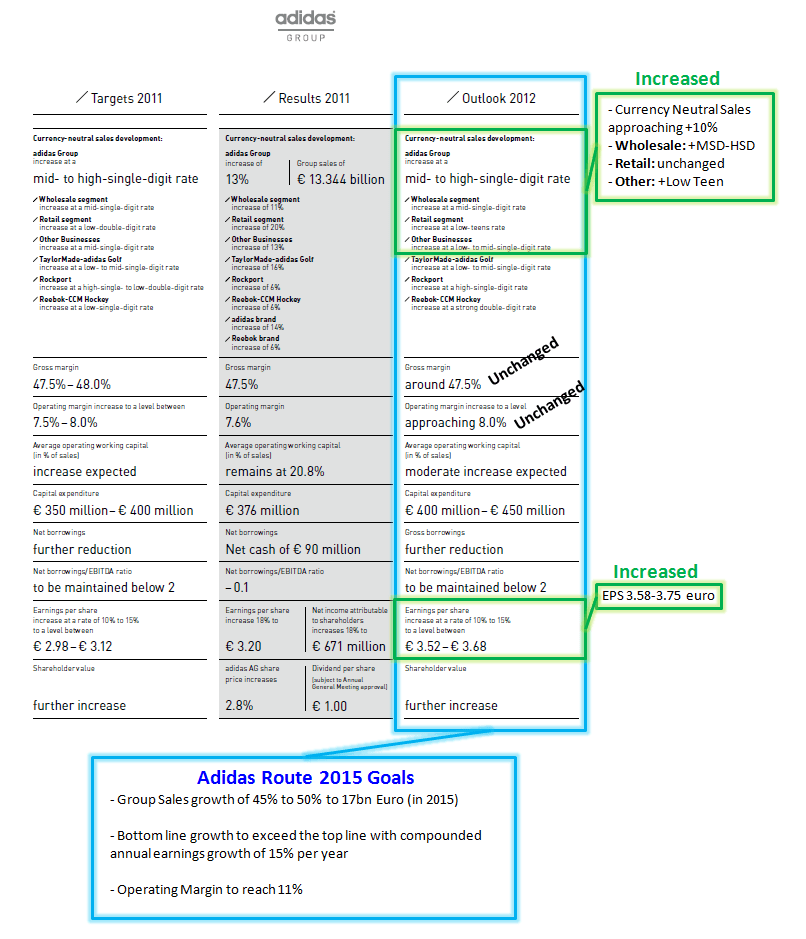

Adidas gives no quarterly guidance. Here is a table given at the end of last fiscal year, as well as changes that it’s already made to the outlook.

Highlights from the Call:

Revenues: +17% (+14% currency neutral)

5th consecutive quarter of double digit top line growth

- Wholesale: +10% cc Driven by all regions except North America; Other Asia+29%, China +27%

- Same Store Sales: +9% cc, North America +17%, Latin America +14%

- Other: +32% cc

Geographic Callouts:

Greater China: +26% currency neutral

No Doubt Adidas is gaining share in the market

- Disciplined business rebuild since 2009

- Maintained sharp focus on distribution quality & store optimization

- Refined product offering, brand marketing & merchandising to cater to a more mature/sophisticated Chinese consumer

- Feedback from partners indicate Adidas has the greatest momentum, traffic remains high

Western Europe: +7%

Continue to secure and build on strong market share gains

- Focusing on consumer analytics and channel right product placement

- Examples: UK & Poland +19% & 35% respectively (sporting events this summer)

North America:

Adidas: +10% currency neutral

- Footwear market share now at DD, sales +22% in Q1

TaylorMade-Adidas golf: +33% currency neutral

Reebok (ex licenses/Toning): +5% currency neutral

Brand & Category Callouts:

Adidas: +16% currency neutral

8th consecutive quarter of DD top line growth with DD growth in all regions

- Football: +23% in Q1

- Current strength still ahead of Summer events

- Running: +16%

- Clima franchise up over 80%

- Basketball: +23%

Reebok: -7% currency neutral

Excluding NHL sales shift to CCM, the end of NFL license and ex toning, sales +10% cc

- Continue to see good progress in Western Europe despite economic uncertainty

- North America +5% ex tonight and profitability improving due to better price mix/product offering

- Starting to see traction with global classic sales +7% cc

- India- no additional color, taking the opportunity to improve underperforming area of the business

- Estimating 1 time charges from idea to be a maximum of 70mm euro

TaylorMade-Adidas Golf: Sales +DD in all product categories

- Apparel: +28%

- Footwear: +64%

- EBIT Doubled

- Expecting Adam's golf deal to cost 53mm euro and close later this year

Margin Improvements:

Gross Margins: -74bps

- Higher sourcing costs ate 4.7 points of margins alone

- offset much of sourcing impact through retail penetration, favorable product/regional sales mix

EBIT Margins: +113bps

- Leveraged operating expenses for the 5th consecutive quarter down -160bps as % of sales

- Retail OM +110bps (marketing 11.1% of sales and should be similar to 2011 levels for the full year at 12.7%)

Retail Footprint at Quarter End:

2422 stores, +21 stores or 1% vs. LY

- Opened 110 new stores, closed 89, 30 remodels

Inventories:

+13% cc (17% in Euro Terms)- believe to be best positioned in the industry

Debt:

Net Debt 640mm euro at Quarter end

- Down 274mm or 30% YoY

Equity Ratio +2.9 points to 48.1%

Guidance Increased (See attached Table):

Sales Growth to approach 10% (vs prior MSD-HSD)

- Increased expectations in wholesale and other business

Continue to expect OM to approach 8% with net income growing 12%-17%

EPS projected to be 3.58-3.75 euro vs original guidance of 3.52-3.68

Q&A:

Market Share:

- North America still a lot of potential, concentrating on building the business on a sustainable product platform will pillars in basketball, football, running and training

- Same plan for Europe, though there are some economic challenged but growth should continue with championships coming down the pike

India:

- Do not publish the size of the business but India is not within the 3 biggest countries in Asia

- Believe in 3 months on second quarter call there will be more details on India

Style:

- Very successful in driving the style business primarily through originals

Reebok GM:

- Has been helped by the shift from Hockey into CCM

- Retail segment carrying in higher margin

Japan:

- Market leader in Japan

- Strong business will continue into the next quarter and full year

Input costs:

- Believe the costs have peaked in Q1

Reebok Marketing plans:

- Launched the sport of fitness campaign a few weeks ago

- Marketing concepts seem to be working

- Compares are difficult over easy tones last year but the business is growing

- Expecting new merchandise in the Spring of 2013

Royalty Income Growth:

- Largely due to increase in Adidas products

E-Commerce:

- Grew considerably up 60%

- Do not publish figures for the e-commerce business

Reebok:

- +10% ex license changes & toning, only accounting for NHL/NFL shift, down 5%

China Performance:

- Much more sustainable and healthy business model

- New IT systems that allow for quick response time

- Inventory is cleaner and can be monitored closer

- Will continue to see strong growth moving forward in China

SG&A:

- Getting more leverage from operating expenses which is expected to continue throughout the year

Inventories:

- Want to be in a position to service the consumer fast while managing working capital

- Quality is inventory should be as clean as possible

- No 1 offs in 1Q contributing to inventory position improvement

Retail NEO

- Opened 8-10 stores in Germany with 2 to follow in the coming weeks

- Early indications are quite exciting

Reebok US:

- Difficult comparisons from easy tone in the first 6 months but business is headed in the right direction

ASP:

- Improving but no additional color given on the call

Latin America joint venture:

- Business grew in Q1, working closely with joint venture partner

- Have seen some hurdles with terrorists and import duties

Marketing Spend:

- Will remain around 13%

- Will not necessarily cross the boundary in event years

Toning:

- Don’t see toning as completely over

- Feel they can rebuild the business