TODAY’S S&P 500 SET-UP – May 3, 2012

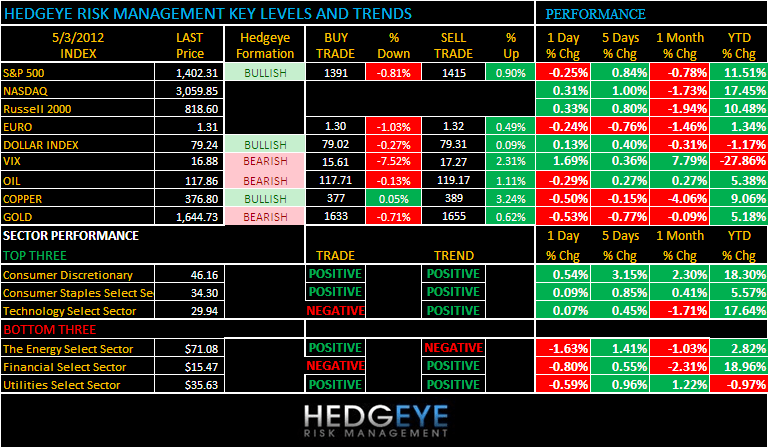

As we look at today’s set up for the S&P 500, the range is 24 points or -0.81% downside to 1391 and 0.90% upside to 1415.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/02 NYSE -377

- Down from the prior day’s trading of 908

- VOLUME: on 5/02 NYSE 780.19

- Increase versus prior day’s trading of 1.13%

- VIX: as of 5/02 was at 16.88

- Increase versus most recent day’s trading of 1.69%

- Year-to-date decrease of -27.86%

- SPX PUT/CALL RATIO: as of 05/02 closed at 2.69

- Up from the day prior at 1.74

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 39

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.93

- Unchanged from prior day’s trading

- YIELD CURVE: as of this morning 1.67

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: Challenger Job Cuts (Y/y), Apr.

- 7:45am: ECB rate decision

- 8:30am: Nonfarm Productivity, 1Q P, est. -0.6% (prior 0.9%)

- 8:30am: Unit Labor Costs, 1Q P, est. 2.8% (prior 2.8%)

- 8:30am: Jobless Claims, week of Apr. 28, est. 379k (prior 388k)

- 9:45am: Bloomberg Consumer Comfort, week of Apr. 29

- 10:00am: ISM Non-Manf., Apr., est. 55.3 (prior 56)

- 11:00am: Fed’s Williams speaks on economy in Santa Barbara, CA

- 1:00pm: Fed’s Lockhart speaks on economy in Santa Barbara, CA * 1:30pm: Fed’s Plosser speaks on economy in Santa Barbara, CA

GOVERNMENT:

- U.S. Treasury Secretary Tim Geithner, Secretary of State Hillary Clinton attend opening session U.S.-China Strategic and Economic Dialogue in Beijing

- President Obama hosts Cinco de Mayo reception

- House, Senate not in session

- Quinnipiac University officials discuss latest poll of “swing state” voters in Florida, Ohio and Pennsylvania, 10am

WHAT TO WATCH:

- April retail sales expected to gain 1.5%: Retail Metrics

- European Central Bank may leave benchmark interest rate at record low 1%, economists est. Rate decision at 7:45am, press conference 45 minutes later

- JPMorgan to take stake of almost 30% in France’s Technicolor, in move supported by Technicolor management: Les Echos

- U.K.’s Sage said to be in talks on putting its accounting software for small businesses on Microsoft’s Azure cloud platform: FT

- ISM’s index of non-manufacturing industries probably cooled to 4-month low of 55.3 from 56 in March, economists est.

- Nexon said to be in talks to distribute Electronics Arts’s next “FIFA Online” title in Asia rather than buy the company

- Carlyle sold 30.5m shrs at $22 each, less than $23-$25 range

- Temasek selling $2.4b in BOC, China Construction Bank

- CME raises margins for non-hedged accounts to meet CFTC rule

- BP wins tentative approval for $7.8 billion oil-spill pact

- Billionaire James Packer may sell his investment in Foxtel, held through his control of Consolidated Media Holdings, to help fund bid for Echo Entertainment: Daily Telegraph

- Philip N. Duff, founder of FrontPoint Partners, said to be struggling to attract assets for his latest money-management venture

- Lockheed Martin won’t lead a team to compete against Hewlett-Packard for $4.5b Navy network deal; may increase chances HP will hold onto its biggest U.S. govt. contract

- One of Edvard Munch’s four versions of “The Scream” set record for work of art at auction when it sold at Sotheby’s last night for $119.9m

EARNINGS:

- Lamar Advertising (LAMR) 6am, $(0.14)

- Cimarex Energy (XEC) 6am, $1.27

- Cigna (CI) 6:30am, $1.30

- Fortress Investment Group (FIG) 6:30am, $0.10

- Gildan Activewear (GIL CN) 6:33am, C$0.21

- NRG Energy (NRG) 6:45am, $(0.08)

- Teradata (TDC) 6:55am, $0.56

- American Tower (AMT) 7am, $0.74

- Alpha Natural Resources (ANR) 7am, $(0.06)

- BCE (BCE CN) 7am, C$0.73

- Cardinal Health (CAH) 7am, $0.88; Preview

- Apartment Investment & Management (AIV) 7am, $0.37

- HCA Holdings (HCA) 7am, $0.98

- Lear (LEA) 7am, $1.20

- GE Energy (OGE) 7am, $0.33

- Jean Coutu Group PJC (PJC/A CN) 7am, C$0.24

- Plains Exploration & Production (PXP) 7am, $0.62

- Elizabeth Arden (RDEN) 7am, $0.04

- Viacom (VIAB) 7am, $0.89

- Xylem (XYL) 7am, $0.36

- Beam (BEAM) 7:01am, $0.47

- ANSYS (ANSS) 7:03am, $0.66

- WPX Energy (WPX) 7:15am, $(0.02)

- SCANA (SCG) 7:22am, $1.03

- El Paso (EP) 7:29am, $0.28

- Airgas (ARG) 7:30am, $1.07

- General Motors (GM) 7:30am, $0.85; Preview

- Hyatt Hotels (H) 7:30am, $0.09

- Progress Energy (PGN) 7:30am, $0.65

- Sealed Air (SEE) 7:30am, $0.21

- Scripps Networks Interactive (SNI) 7:30am, $0.60

- Sara Lee (SLE) 7:30am, $0.25; Preview

- El Paso Pipeline Partners (EPB) 7:44am, $0.61

- Apache (APA) 8am, $3.07

- Level 3 Communications (LVLT) 8am, $(0.52)

- Pinnacle West Capital (PNW) 8am, $(0.07)

- Valeant Pharmaceuticals International (VRX CN) 8am, $0.97

- CenterPoint Energy (CNP) 8:15am, $0.33

- Cablevision Systems (CVC) 8:15am, $0.18

- Manulife Financial (MFC CN) 8:22am, C$0.37

- Denbury Resources (DNR) 8:30am, $0.38

- MGM Resorts International (MGM) 8:30am, $(0.16)

- Sempra Energy (SRE) 9am, $0.98

- SNC-Lavalin Group (SNC CN) 9:05am, C$0.52

- Great-West Lifeco (GWO CN) 12:38pm, C$0.52

- CareFusion (CFN) 4pm, $0.45

- Mohawk Industries (MHK) 4:01pm, $0.55

- LinkedIn (LNKD) 4:02pm, $0.09

- First Solar (FSLR) 4:04pm, $0.48

- Fluor (FLR) 4:05pm, $0.87

- Kraft Foods (KFT) 4:05pm, $0.56

- SandRidge Energy (SD) 4:05pm, $0.02

- American International Group (AIG) 4:15pm, $1.13

- Northeast Utilities (NU) 4:15pm, $0.67

- CF Industries Holdings (CF) 4:18pm, $4.95

- Southwestern Energy (SWN) 5pm, $0.32

- Public Storage (PSA) 5:03pm, $1.42

- Eldorado Gold (ELD CN) 5:41pm, C$0.17

- Pembina Pipeline (PPL CN) 6:12pm, C$0.25

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

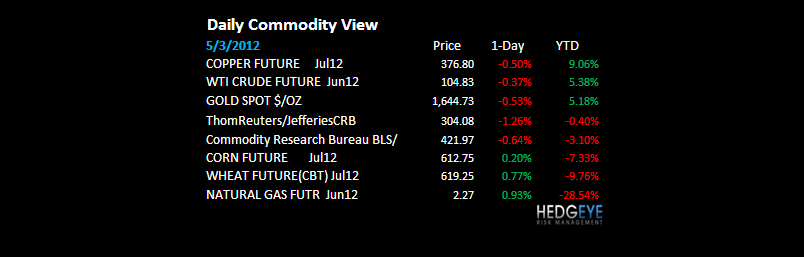

OIL – most important Global Macro move of the week right now is Brent Oil snapping my intermediate-term TREND support line of $119.17; Oil has been the big holdout of the major commodities deflating; if this holds, its bullish on the margin for Consumers (and Consumption Equities). The Divergence their yesterday (XLE -1.6% vs XLY up agrees).

- Crude Oil Extends Biggest Decline in Two Weeks on Jobs, Supplies

- Iran Embargo Impossible to Meet as Ships Depend on Blended Fuel

- Chesapeake Alone on Wall Street in Gas-Rally Bailout: Energy

- Barrick Gold Spending Faster Than Earnings Rise: Commodities

- CME Raises Margins for Non-Hedged Accounts to Meet CFTC Rule

- Gold Declines on Concern Slowing European Growth to Boost Dollar

- Copper Falls for Second Day as Slowing Economies May Curb Demand

- World Food Prices Fell in April as Cost of Dairy, Grain Declined

- Corn Set to Gain on Speculation China May Boost U.S. Purchases

- Shanghai Exchange to Start Silver Futures Trading From May 10

- Palm Oil Slumps to Six-Week Low as Weather May Aid U.S. Soybeans

- Real Yields Topping Asia as Rains to Cool Prices: India Credit

- New Europe Ports Seen Unprofitable With Slump Deepening: Freight

- Indonesia Ban on Unprocessed-Metal Exports to Proceed as Planned

- Sugar Falls to 19-Month Low on India’s Exports; Coffee Declines

- Proposed Rule Would Weaken Mad Cow Protections, Ranch Groups Say

CURRENCIES

US DOLLAR – Strong Dollar = Stronger Consumption, globally; that’s the only way out of this mess and it doesn’t take much. Yesterday’s +0.35% move in the USD Index was more of an arrest of its decline (down -6 of the last 7 wks) than a rip higher. If you see a sustainable breakout > $80 USD Index, Oil is going to come down a lot faster.

EUROPEAN MARKETS

SPAIN – we learn a lot more about bear markets on the bounces than on the declines; the 2012 crash/decline in Spain’s IBEX is trivial to consider in the rear-view mirror (down -23% from YTD peak yesterday, making a fresh crisis low which matters vs 2011); the bounce would have to get > 7498 for us to change our view from bearish to bullish.

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team