This note was originally published April 05, 2012 at 10:49 in Restaurants

When we consider that GMCR has now declined for 10 days in a row and insiders are exiting the stock, it is easy to concoct a bearish story. The question is: how bearish is bearish enough? We think the stock could go to $25.

Green Mountain Coffee Roasters’ stock is one we have been wary of for some time. Howard Schilit, renowned forensic accountant, mentioned the company in a highly insightful interview with Barron’s last weekend about accounting shenanigans. Also over last weekend, we also got our hands on an amended Class Action Complaint filed against the company in the US District Court in Vermont. It makes for fascinating reading and cites 14 confidential witnesses from many different tiers and roles within GMCR.

We can imagine a time when the senior management team at Green Mountain Coffee Roasters looked at each other across a table and said, “Starbucks is going to buy us one day”. While that eventuality may materialize one day, our estimation is that it is more likely to occur in a bankruptcy context than any other.

The first rumblings about GMCR’s accounting issues began in late 2010. The company had acknowledged an overstatement of pretax income in September of 2010 and the SEC had notified the company of an investigation into its revenue recognition practices. In 2011, when it became clear that Starbucks wanted to take a slice of the single-serve market, we were convinced that the Seattle-based titan would go it alone. We were wrong then but, as time passes, our confidence is growing that our thinking was not a million miles off target.

With a current market capitalization of $7 billion and sales of $4.2 billion, weighing the current fundamental risks leads us to believe that this company’s stock could go to $25 or even lower in short order. We believe that there is a risk of inventory write-downs and other one-time but long overdue charges. The overstatement of pre-tax income acknowledged in 2010, as we discuss in more detail later in this post, bore no relation to the company’s relationship with M. Block & Sons, GMCR’s single order fulfillment entity. According to its website, M. Block is a leading provider of end-to-end supply chain solutions. Our view is that some costs could arise from alleged improprieties outlined in an Amended Class Action Complaint filed against Green Mountain last week. While our legal expertise is limited at best, the numbers corroborate with much of the detail in that complaint. If even 10% of the allegations in the complaint are founded in truth, investors may begin to exit the stock en masse.

Before we begin this note in earnest, it is worth stating clearly that many of the points discussed in this post is merely alleged to be true, coming from the Amended Class Action Complaint filed against Green Mountain Coffee Roaster’s Inc., et al., at the United States District Court in Vermont and also various other sources where the information provided constitutes opinion.

NOTHING TO BE ALARMED ABOUT

On September 28th, 2010, GMCR filed a form 8-K with the SEC announcing management’s discovery of an “immaterial” overstatement of pretax income related to an immaterial accounting error relating to “the margin percentage it had been using to eliminate the inter-company markup in its K-Cup inventory balance residing at its Keurig business unit”. Having determined that the error arose in 2007, the company calculated the impact from that point through June 2010 as being $7.6 million in pre-tax income or, net of tax, $0.03 in EPS.

Within the same filing, the company reveals that on September 20th, 2010, “the staff of the SEC’s Division of Enforcement informed the Company that it was conducting an inquiry and made a request for a voluntary production of documents and information. Based on the request, the Company believes the focus of the inquiry concerns certain revenue recognition practices and the Company’s relationship with one of its fulfillment vendors. The Company, at the direction of the audit committee of the Company’s board of directors, is cooperating fully with the SEC staff’s inquiry”.

The lead plaintiffs allege that the company knew about the SEC’s investigation for months. A confidential witness, “CW1”, cited in the case, states that the company’s revenue recognition methods were being investigated by the SEC. CW1 was a former GMCR distribution planning manager, according to the Complaint. Said witness recalled that in November and December 2009, internal discussions regarding the company’s revenue recognition practices were held at company meetings attended by many senior GMCR executives including CFO Frances Rathke and CEO Larry Blanford.

Our contention is that the inventory control and revenue recognition issues are one and the same largely due to the influence GMCR had over its supply chain “partner” MBlock (more on this later). The confidential witness, referred to above, claims to have confronted two superiors, VP of Operations Jonathan Wettstein and Director of Operations, Don Holly about the company’s inventory processing practices on numerous prior occasions, dating back as far as October 2009. His views were expressed to no avail; the inventory processing practices remained the same, as we discuss later.

While it is not appropriate or possible for us to take a stance on whether or not management knowingly and willingly manipulated inventory and sales numbers, it is surprising to us that management would have assumed such a bullish stance during the 7/28/10 conference call, if indeed SEC investigators were already meeting with company representatives regarding accounting practices at the company. The following statement from management during that conference call was highlighted by the Complaint as being particularly misleading given that future sales growth was being guided down at the same time:

“And at the same time we'll be building our retailer inventories as we get into the fall season, with the expectation that we are going to continue to exceed our own expectations on brewer sales.”

Is it possible to have the expectation that one’s expectations are going to be exceeded?

THE HIDE & SEEK INVENTORY METHOD

The “Class Period”, which is the stretch of time that the Action alleges that investors purchased GMCR’s common stock at inflated prices due to materially false and misleading statements, spans from 7/28/10-9/28/10. At the center of the Action is the allegation that inventory was purposely accumulated with little or no regard for real demand for the product.

The confidential witness that claims to have approached management about the company’s inventory processing practices, CW1, outlined that management preferred a “standard deviation plus 3 [days’ inventory]” method versus the “ABC” method favored by the industry which categorized inventory as fast, medium, and slow moving items. The witness stated to Wettstein that this method was “skewed” and would result in production of expired and expensive products to be produced solely to “carry-over” the inventory from one period to the next. CW1’s input did not result in any change in policy, according to the Complaint.

Two other anecdotes, both of which – if true – are astounding, detail further improprieties that were carried out by GMCR, according to confidential witnesses cited in the Complaint. CW1, stated, according to the Complaint, that “senior management stressed”, at weekly and bi-weekly meetings, “the need to continue to produce product regardless of whether or not the product could be sold.” The resulting inventory problem was allegedly masked in two ways. First, according to CW1, to “get rid of inventory” during audits, dated or expired coffee was loaded onto trucks and parked a few blocks away until after the auditors left the warehouse. CW7, a lower-level employee in GMCR’s shipping department in Knoxville, Tennessee, corroborated CW1’s claims, adding that inventory was shipped to other company warehouses only to be returned untouched days later. Additionally, CW1’s claims that expired coffee product was offered to pig farmers for inclusion in silage were strengthened by CW7 who said that he/she had witnessed vast amounts of product being dumped in land-fills near the Knoxville production plants.

Why would employees, higher- and lower-level, have gone along with this strategy? Why would M. Block have been so complicit in the alleged shenanigans?

FOLLOW THE MONEY

Money is the ultimate truth serum and, we believe, following the money helps to tie a lot of this story together. Details within the Complaint as well as actual insider transactions by officers of the company seem to rhyme with the narrative of shenanigans that has been touted by Green Mountain detractors for the last eighteen months or more.

Firstly, it is worth starting with M. Block, a company that was Keurig’s single order fulfillment entity. In addition to taking orders for GMCR, M. Block also had as much as 500,000 square feet of warehouse space, storing both brewers and coffee. Green Mountain was an extremely important client for M. Block; the Complaint states that prior to mid-2009, GMCR represented 20% of the company’s business. After a nationwide contract was agreed in July ’09, however, that share 4quickly grew to 75%. According to the Complaint, confidential witness six, or “CW6”, a former VP of Operations at one of the company’s roasters and a CPA, stated that the SEC was questioning the existence of an arms-length relationship between GMCR and M. Block and whether or not the transactions between the two companies could be recorded as sales. David Einhorn’s recent presentation, the research behind which included interviews with current and former employees of GMCR and its partners, alleges that GMCR exploited the relationship with M. Block to engage in a “variety of shenanigans that appear designed to mislead investors and to inflate financial results.”

Given the importance of GMCR to M. Block from a revenue perspective, it is clear that the incentive existed for the smaller, dependent company to comply with the practices of its client upon which it relied so heavily.

Lower-level employees, both within GMCR and M. Block (although Einhorn cites employees of M. Block as feeling like they worked for GMCR) were incentivized to follow senior management’s plan of attack, according to the Complaint. CW1 states in the document that all employee bonuses were awarded annually and based upon the amount of product produced, not on the amount of product sold.

Furthermore, the Executive Compensation section of the fiscal 2011 10-K contains a definition (that was also in a proxy detailing the policy for FY10) of the “Annual Bonus Opportunity or Annual Cash Bonus” as “cash reward paid to executives on an annual basis; currently based on two financial metrics: net sales and non-GAAP operating income.” If the company was able to manage revenue figures by simply ordering K-Cups from licensed third-party roasters and warehousing the inventory at M. Block’s facilities, as the Complaint alleges, it seems that the calculus behind executive level bonuses may have provided some incentive for senior officers to follow that strategy.

MANAGEMENT IN THE KNOW?

From the outside, it is impossible for anyone to know what management was thinking during the Class Period. Looking at the insider transaction of Scott McCreary and Michelle Stacy definitely doesn’t instill much confidence. In the table below, we provide a timeline of events interwoven with color provided in the Class Action Complaint by witnesses.

When we consider that GMCR has now declined for 10 days in a row and insiders are exiting the stock, it is easy to concoct a bearish story. The question is: how bearish is bearish enough? We think the stock could go to $25.

FUTURE RISKS

The primary concerns from us arising from this Complaint are as follows:

- There is a risk that management may have been derelict in their duty to provide investors with forthright guidance on business trends that is supportive by reasonable basis.

- It appears that there is a significant risk that the relationship with M. Block was not “arms length”. Since transactions between the companies are being booked as sales, the relationship should be “arms length”. The SEC is investigating. A change in revenue recognition more reflective of reality could be just as bad for net sales growth as it has been good.

- No restatement has yet been made pertaining to GMCR’s relationship with M. Block, per the company’s 2010 10-K. We believe that there is a high likelihood that the inventory number of ~$600mm will need to be written down. The question is, by how much? David Einhorn thinks that as much as 33% of the inventory in M. Block’s warehouse could be expired.

- Uncertainty risk is extremely high. How much inventory does the company have? Will it need to revise its entire storage and supply chain system under scrutiny and the looming probability of further class action law suits (if media reports are anything to go by)?

FINANCIALS – THE BIG UNKNOWN

One of the worst case scenarios for GMCR shareholders would be if management has been understating inventory which has resulted in margins being overstated. The company is burning a tremendous amount of cash and taking on leverage to do it. Taking it bit by bit, we can see that the return profile for this stock is not encouraging. We see few reasons to own this stock beyond the size of the market and even that positive is greatly overshadowed by the plethora of negative risks facing the company.

INVENTORY

You can see in the chart below that inventories are extremely high. Despite management’s bullish commentary on its “demand model” – that was based on what were likely inflated sales data – the sales-inventory spread has contracted for six of the last seven quarters. There are far more questions than answers when it comes to GMCR’s inventory. Did managers overshoot the mark when sales did not keep pace? Is there a write-down coming? We think there has to be.

As we mentioned earlier, Greenlight Capital thinks as much as a third of the inventory in M. Block’s facilities could be expired. Our take is that there is a strong chance neither M. Block nor GMCR itself knows exactly what its inventory is worth. Not to single out Pricewaterhouse Coopers, but none of the major auditing firms have been strangers to financial scandals over the past ten years. Many have been blamed for not holding clients to a high enough standard of scrutiny during audits. Yet PWC was compelled to make the following statement in a report that was included in GMCR’s 2010 10-K:

“We do not express an opinion or offer any other form of assurance on management’s statement referring to the Company’s plan for remediation of the material weaknesses in internal control over financial reporting.”

RETURN ON EQUITY

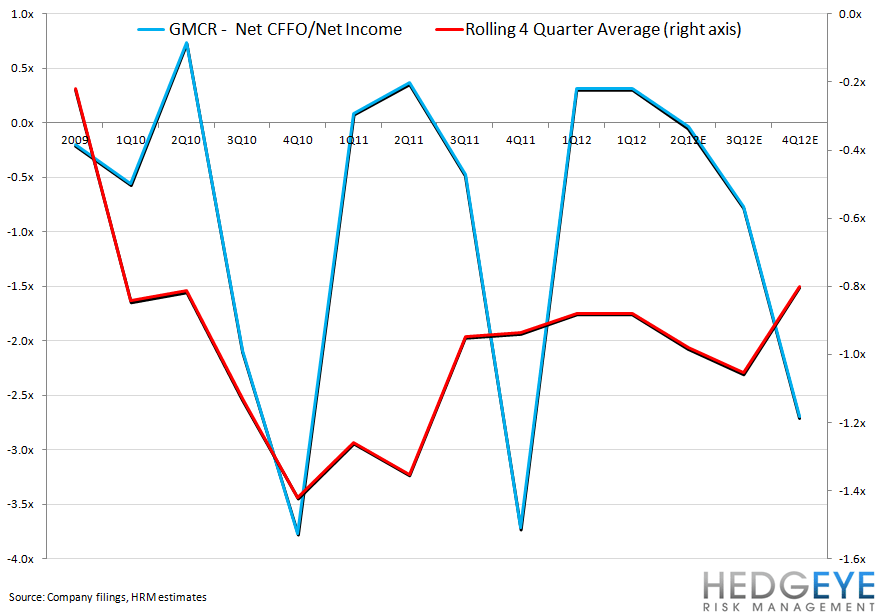

Between 2008 to 2010 return on common equity declined from 18.6% to 15.2%. At the same time, EBIT margins surged from 12.1% to 18.2%. Despite higher margins, the declining returns are due to asset turnover decreases for both accounts receivable and inventory. In fact, inventory turnover has dropped from 5.2x in 2008 to an all time low of 3.7x in 2011. Equally troubling is the company’s inability to convert reported net earnings into operating cash flows from 2008 to 2011.

POOR ASSET BASE & LOW QUALITY BRANDS

The company growth by acquisition is only temporary and the assets the company bought (overpaid for) are of low quality relative to competing brands in the coffee space.

The first acquisition was in November 2009, when they acquired Timothy’s Coffees of the World Inc. The acquisition gave them the right to the little known Timothy’s World Coffee brand and wholesale business as well as licensed brands Kahlua and Emeril’s. The acquisition also opened the Canadian market to GMCR. Five month later, in May 2010, they bought Diedrich Coffee in a bidding war Peet’s Coffee. This acquisition enabled the company to penetrate the Southern California market. Included in this acquisition was Diedrich Coffee, Coffee People brands, and a perpetual royalty-free license in the U.S. for the Gloria Jean’s coffee brand, for use in K-Cup portion packs. Peet’s was also sniffing around this acquisition so a big premium was paid. In December of 2010, GMCR acquired LJVH Holdings, owner of Van Houtte and other brands, based in Montreal.

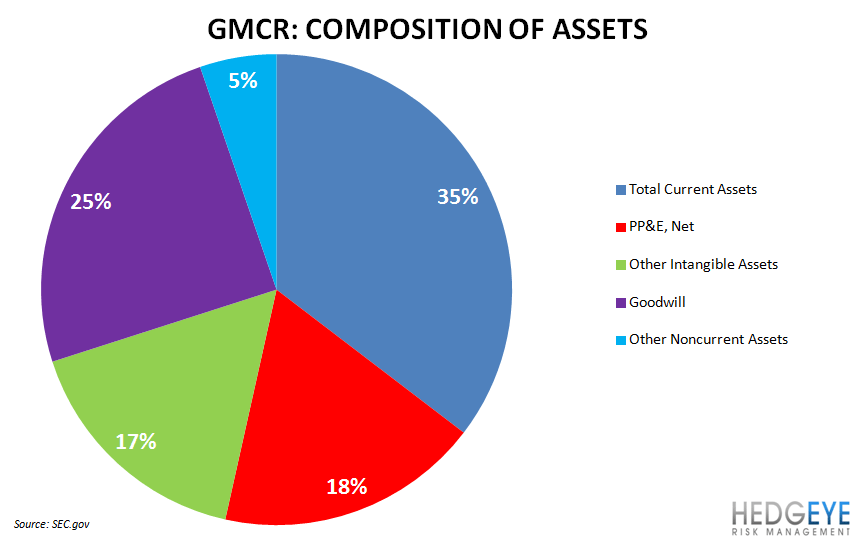

We can make a lot of qualitative comments on these brands, and we do not believe that they were great acquisitions by any means, but looking at GMCR’s asset base at the moment is not encouraging. Over 41% of the company’s assets are intangibles and goodwill. Consistent with a company that has, in our view, been more concerned with superficial improvements than making substantial strides in the underlying business, GMCR is depreciating these assets over a period of 10-15 years when a much shorter period would be more appropriate.

The Current Assets don’t look much better. At the end of FY1Q12, 48% of Current Assets is comprised of inventory, which is up 125% year-over-year. As we have stated several times in this note, we think this inventory number needs to be written down. Accounts receivable is up 73% year-over-year also.

CASH BURN GIVING BULLS HEARTBURN

The confluence of all of these factors – the excessive inventories, poor assets, and sub-par returns – is that the company burns cash. We see the faulty yardstick – inflated demand – that management has used to run its business as being at the root of this problem. The “demand model” has led the company to announce a staggering 135% increase in capital spending for FY12 versus FY11. We have the company burning $935mm during the two year period FY11 and FY12. If the capital markets decide to tighten the company’s access to capital it could be catastrophic. How many companies in history have grown earnings over the long run while burning cash?

The cash conversion cycle cuts through the noise and offers a clear gauge of how effectively the company is managing inventory, accounts receivable, and accounts payable.

Looking at the chart below, we can see that the proportion of earnings yielding cash is not a positive sign for the company. Having a cash burn rate that is within the limits of available resources is not necessarily a negative but we feel that GMCR is going to test the goodwill of the capital markets if its cash flow generation does not improve. With capex set to go through the roof in FY12, we don’t see that improvement coming about any time soon.

CONCLUSION

We are not legal experts but think that the looming possibility of further Class Action law suits coming down the pike do not bode well for GMCR. Just this past Monday, for instance, Faruqi & Faruqi, LLP, a national law firm, announced that it is investigating potential wrongdoings at Green Mountain Coffee Roasters. The financial outlook, irrespective of any legal struggles in the future, is also dire. Favorable debt and equity markets have allowed this company to live on borrowed time – and live well. With competition increasing and the high probability that capital-raising is set to become more difficult as time goes on, we believe that GMCR’s party is over.

Howard Penney

Managing Director

646.455.0992

Rory Green

Analyst

646.455.0992