TODAY’S S&P 500 SET-UP – May 2, 2012

As we look at today’s set up for the S&P 500, the range is 24 points or -1.05% downside to 1391 and 0.65% upside to 1415.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/01 NYSE 908

- Up from the prior day’s trading of -665

- VOLUME: on 5/01 NYSE 771.45

- Decrease versus prior day’s trading of -9.45%

- VIX: as of 45/01 was at 16.60

- Decrease versus most recent day’s trading of -3.21%

- Year-to-date decrease of -29.06%

- SPX PUT/CALL RATIO: as of 05/01 closed at 1.74

- Down from the day prior at 1.92

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.93

- Decrease from prior day’s trading of 1.94

- YIELD CURVE: as of this morning 1.68

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications (prior -3.8%)

- 8am: Fed’s Tarullo to speak in New York at the CFR

- 8:15am: ADP Employment Change, April, est. 170k (prior 209k)

- 9:45am: ISM New York, April (prior 67.4)

- 10am: Factory Orders, March, est. -1.7% (prior 1.3%)

- 10am: U.S. Treasury makes quarterly refunding announcement

- 10:30am: DOE inventories

- 12:30pm: Fed’s Lacker speaks on economy in Norfolk, Virginia

- 6:30pm: Fed’s Evans speaks in Chicago

GOVERNMENT:

- NRC meets to discuss post-Fukushima recommendations on fires, flooding at power plants caused by earthquakes, 1pm

- FCC Chairman Julius Genachowski discusses broadband adoption, job creation at National Cable & Telecommunications Assoc, 3pm

- President Obama scheduled to return to the U.S. after a surprise visit to Afghanistan

- House, Senate not in session

- Commerce Dept. advisory panel meets to vote on recommendations to improve U.S. competitiveness in exporting renewable energy, energy efficiency products and services, 10am

- China, U.S. Strategic and Economic Dialogue in Beijing

WHAT TO WATCH:

- Carlyle consults buyout playbook to price IPO at 62% discount; IPO expected to price this evening

- Facebook said to begin marketing share sale as soon as next wk

- Chinese manufacturing index rose in April to 49.3 vs prelim. 49.1 reported April 23, signaling rebound

- ADP report may show U.S. added 170k jobs in April after 209k in March

- U.S. Deputy Treasury Secretary Neal Wolin said opponents of the Dodd-Frank Act will fail in efforts to roll back part of the regulatory overhaul

- Genworth Financial’s CEO resigned after an 80% stock plunge since the end of 2006

- Goldman Sachs said a proposed Fed rule seeking to limit links between banks could cut U.S. economic growth by as much as 0.4 percentage point

- News Corp.’s Rupert Murdoch may be prompted to lower or sell his 39% stake in BSkyB

- BP Gulf of Mexico spill trial shouldn’t be delayed until after a proposed hearing on a settlement of most private- party claims, U.S. tells judge

- Euro-region manufacturing shrank for a 9th month in April

- Twitter said to have considered buying mobile-photo app Camera+

EARNINGS:

- AMERIGROUP (AGP) 6am, $0.56

- Enterprise Products Partners LP (EPD) 6am, $0.57

- Macerich (MAC) 6am, $0.69

- CVS Caremark (CVS) 6:45am, $0.63. Preview

- Barrick Gold (ABX CN) 6:55am, $1.09; Preview

- Comcast (CMCSA) 7am, $0.43; Preview

- El Paso Electric (EE) 7am, $0.12

- Energizer Holdings (ENR) 7am, $1.08

- Time Warner (TWX) 7am, $0.64; Preview

- AllianceBernstein Holding (AB) 7:09am, $0.24

- Devon Energy (DVN) 7:30am, $1.43

- IAC/InterActive (IACI) 7:30am, $0.46

- IntercontinentalExchange (ICE) 7:30am, $2.02

- Och-Ziff Capital Management Group (OZM) 7:30am, $0.13

- Public Service Enterprise Group (PEG) 7:30am, $0.67

- Cooper Industries (CBE) 8am, $1.00

- Loblaw (L CN) 8am, $0.49

- Mastercard (MA) 8am, $5.30

- Magellan Midstream Partners (MMP) 8am, $0.96

- Rowan (RDC) 8:15am, $0.34

- Allete (ALE) 8:30am, $0.77

- Franklin Resources (BEN) 8:30am, $2.22

- Clorox (CLX) 8:30am, $1.03; Preview

- Marathon Oil (MRO) 8:30am, $0.87

- Allergan (AGN) 9am, $0.87; Preview

- Expeditors International of Washington (EXPD) 9am, $0.39

- PG&E (PCG) 9:04am, $0.72

- Edison International (EIX) 4pm, $0.51

- Green Mountain Coffee Roasters Inc (GMCR) 4pm, $0.64

- DreamWorks Animation SKG Inc (DWA) 4:01pm, $0.09

- Kim Realty (KIM) 4:01pm, $0.30

- Sunoco (SUN) 4:01pm, $ (0.08)

- Whole Foods Market (WFM) 4:03pm, $0.59

- Allstate (ALL) 4:05pm, $1.12

- JDS Uniphase (JDSU) 4:05pm, $0.11

- Symantec (SYMC) 4:05pm, $0.38

- Visa (V) 4:05pm, $1.51

- ValueClick (VCLK) 4:05pm, $0.34

- ON Semiconductor (ONNN) 4:05pm, $0.09

- Prudential Financial (PRU) 4:07pm, $1.72

- Lincoln National (LNC) 4:10pm, $0.98

- Boston Beer (SAM) 4:10pm, $0.41

- Continental Resources (CLR) 4:15pm, $0.85

- Concho Resources (CXO) 4:15pm, $1.13

- Hartford Financial Services Group (HIG) 4:15pm, $0.91

- Transocean (RIG) 4:15pm; Preview

- Onyx Pharmaceuticals (ONXX) 4:15pm, $ (0.78)

- RenaissanceRe Holdings (RNR) 4:22pm, $2.42

- Charles River Laboratories International (CRL) 4:30pm, $0.65

- Pioneer Natural Resources (PXD) 4:30pm, $1.20

- Hertz Global Holdings (HTZ) 4:30pm, $0.00

- First Quantum Minerals (FM CN) 5pm, $0.24

- Murphy Oil (MUR) 5pm, $1.52

- Tesoro (TSO) 5pm, $0.27

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

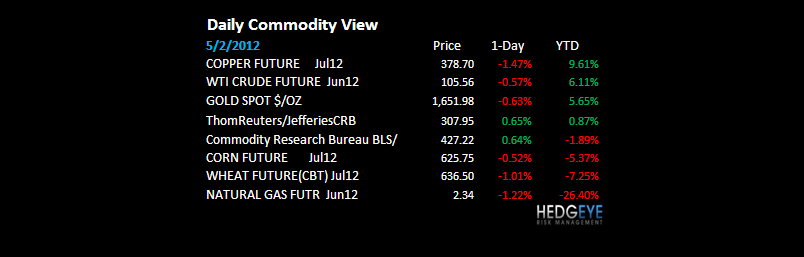

- Trafigura Follows Raffles Into Heart of Asian Trade: Commodities

- Philippines Cuts Rice Imports as Harvest Swells, Alcala Says

- Investors Dump Commodities in Longest Slide Since November

- Trafigura Hires Bankers for Commodity Trade Finance Business

- Oil Drops From Five-Week High on U.S. Supply, European Economy

- Gold Declines a Second Day on Speculation Stimulus Not Needed

- Corn Declines a Second Day as Rainfall Boosts U.S. Crop Outlook

- Cocoa Reaches Five-Week High on Supply Speculation; Sugar Falls

- Copper Falls as Euro-Area Manufacturing Shrinks for Ninth Month

- Exxon Pact Spurs Rosneft Bonds in $5 Billion Plan: Russia Credit

- YPF Bondholders Lose Faith in Takeover Clause: Argentina Credit

- Freedom From Gazprom Tempts Ukraine as Exxon Hunts Shale: Energy

- Brazil Steelmaker CSN Shares Plummet on Disruptive Rail: Freight

- Gold Rally Stalling at $1,700 Before Drop: Technical Analysis

- Congo Fighting Thwarts Plans to Export Conflict-Free Minerals

- Wien Bearish on Oil First Time as Output Swells: Energy Markets

- BHP Copper Mine Threatened by Mooted Tax Change, Citigroup Says

CURRENCIES

US DOLLAR – the Bernanke Bailout beggers can only hold this USD ball under water for so long before the Europeans and/or the Japanese start to burn their currencies at the stake – its all relative in the Currency War, so get used to it. Dollar having its 1st up day in weeks and Commodities go really red on that (immediate-term correlation USD/CRB back at 0.8).

EUROPEAN MARKETS

EUROPE – apparently the European economy was not allowed to cease to exist this morning and for all the ISM fans out there, some of these European ISM’s are train wrecks (Germany 46.9, Italy 43.9, Spain 43.5!). New orders for Italy had a 3 handle at 39 and change. Ouchy

BUNDS – hot cross German Bunds; we like those as they push to new highs here this morning - #GrowthSlowing still matters and that’s why you buy Bunds and UST Bonds. We bought TLT yesterday on the associated no-volume rally in US stocks.

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team