TODAY’S S&P 500 SET-UP – May 1, 2012

As we look at today’s set up for the S&P 500, the range is 19 points or -0.49% downside to 1391 and 0.86% upside to 1410.

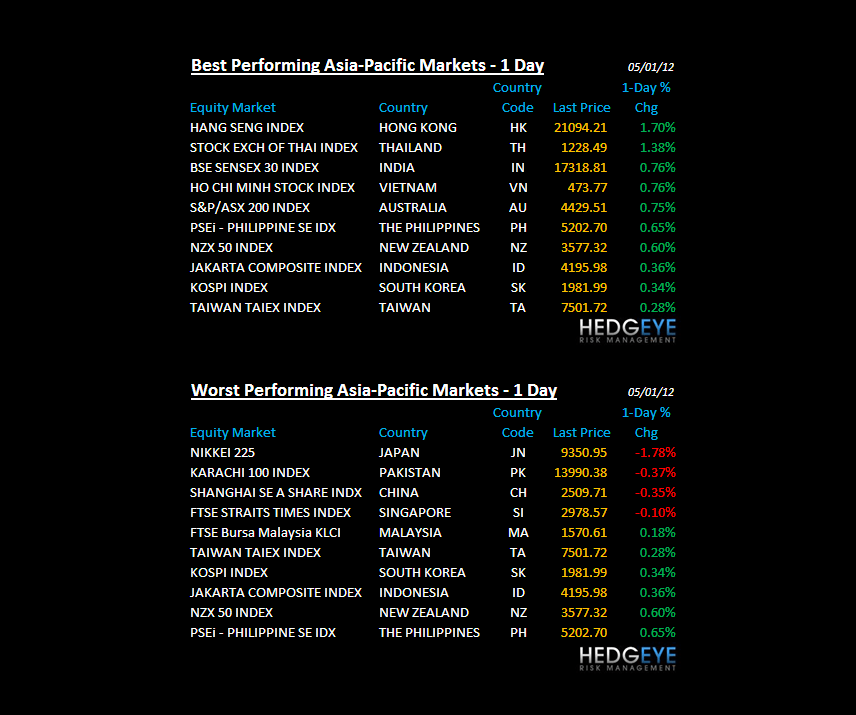

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 4/30 NYSE -665

- Down from the prior day’s trading of 1005

- VOLUME: on 4/30 NYSE 851.91

- Increase versus prior day’s trading of 8.14%

- VIX: as of 4/30 was at 17.15

- Increase versus most recent day’s trading of 5.09%

- Year-to-date decrease of -26.71%

- SPX PUT/CALL RATIO: as of 04/30 closed at 1.92

- Down from the day prior at 2.21

CREDIT/ECONOMIC MARKET LOOK:

APRIL – you can only put lipstick on a pig for so long, then lower-highs start to concern the bulls; particularly as the Macro data confirms that price momentum. Perma-Bulls have had to learn this lesson the hard way in 3 of the last 4yrs (ie sell in Q1, buyem back in Q3 a lot lower) and I don’t think Pavlov’s bells are going to keep them in it on “valuation” this time either.

10YR TREASURIES – bond yields continue to tell you all you need to know about Growth Slowing in the USA. At 1.92% this morning, yields are testing 6 week lows and have gone straight down since mid-March when the US growth slowdown picked up on the downside. Yesterday’s PMI print was -10% m/m and Jobless Claims are up +15% m/m – it matters.

- TED SPREAD: as of this morning 37

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.91

- Unchanged from prior day’s trading

- YIELD CURVE: as of this morning 1.66

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 9:30am: Fed’s Kocherlakota speaks to tribal leaders in Washington

- 10am: Construction Spending, Mar., est. 0.5% (prior -1.1%)

- 10am: ISM Manufacturing, Apr., est. 53.0 (prior 53.4)

- 10am: ISM Prices Paid, Apr., est. 59.0 (prior 61.0)

- 11am: Fed’s Williams speaks on economy in Beverly Hills, CA

- 11:30am: U.S. to sell $30b 4-wk, $26b 52-wk bills

- 12:30pm: Fed’s Evans & Lockhart speak on monetary policy in Beverly Hills

- 3pm: Fed’s Plosser gives economic outlook in San Diego

- 4:30pm: API inventories

GOVERNMENT:

- Secret Service Director Mark Sullivan to provide panel with details on agents’ involvement with prostitutes in Colombia

- U.S. travel industry kicks off $12.3m marketing campaign, with ads rolling out in U.K., Canada, Japan

- SEC, CFTC holds closed meetings on enforcement matters

- House, Senate, Supreme Court not in session

WHAT TO WATCH:

- Fed said to have criticized how some of the 19 largest U.S. banks calculated potential losses, planned dividends in this year’s stress tests

- Group that includes Wolverine World Wide, Golden Gate Capital said to be near agreement, may announce deal as soon as today to buy Collective Brands for $21-$22 per share

- Mitsubishi, Mitsui agreed to buy 14.7% stake in Woodside Petroleum’s proposed Brose LNG project in Australia for $2b

- ISM’s factory index probably eased to 53 last month from 53.4 in March, economists’ est. ahead of today’s report

- Chesapeake Energy says IRS reviewing executive-incentive program that allowed CEO Aubrey McClendon to buy stakes in thousands of co.’s oil and natgas wells, in filing yesterday

- April U.S. auto sales rate may be 14.3m, up from 13.2m year- ago, decelerating from 1Q rate 14.6m

- Bank of America may cut 2,000 banking jobs on top of plan announced last year to eliminate 30k jobs in 3 years: WSJ

- House Financial Services Cmte Chairman Spencer Bachus said he’s been cleared by congressional ethics office of allegations he improperly traded securities during 2008 financial crisis

- NYC’s pension funds will vote against the five Wal-Mart directors standing for re-election at next month’s shareholder meeting: NYT

- Isuzu Motors said it’s considering forming business alliances with companies including General Motors; Nikkei reported April 29 GM may buy 10% stake in Isuzu

- American Hospital Association says Obama administration’s $14.6b program to encourage doctors to adopt electronic medial records too ambitious, goals may not be met, in letter to HHS

- May Day holiday, some overseas markets closed, Occupy Wall Street stages protests

- No U.S. IPOs expected to price: Bloomberg data

EARNINGS:

- Corn Products International (CPO) 5:30am, $1.22

- Becton Dickinson and Co (BDX) 6am, $1.38

- Huntsman (HUN) 6am, $0.39

- Emerson Electric Co (EMR) 6:30am, $0.80

- Harris (HRS) 6:30am, $1.34

- NiSource (NI) 6:30am, $0.71

- Foster Wheeler (FWLT) 6:45am, $0.39

- Archer-Daniels-Midland Co (ADM) 7am, $0.60

- Avon Products (AVP) 7am, $0.28

- Biogen Idec (BIIB) 7am, $1.48

- Cobalt International Energy (CIE) 7am, $(0.11)

- Marsh & McLennan Cos (MMC) 7am, $0.61

- Marathon Petroleum (MPC) 7am, $1.31

- Pfizer (PFE) 7am, $0.56

- Sirius XM Radio (SIRI) 7am, $0.02

- Techne (TECH) 7am, $0.85

- Thomson Reuters (TRI CN) 7am, $0.41

- TRW Automotive Holdings (TRW) 7am, $1.61

- Wisconsin Energy (WEC) 7am, $0.73

- DENTSPLY International (XRAY) 7am, $0.52

- Legg Mason (LM) 7am, $0.47

- Automatic Data Processing (ADP) 7:30am, $0.91

- Cummins (CMI) 7:30am, $2.22

- Hospira (HSP) 7:30am, $0.48

- Arch Coal (ACI) 7:45am, $0.19

- HCP (HCP) 7:45am, $0.66

- Valero Energy (VLO) 7:45am, $0.28

- AGCO (AGCO) 8am, $0.86

- Arrow Electronics (ARW) 8am, $1.09

- Cameco (CCO CN) 8am, C$0.25

- Prologis (PLD) 8am, $0.40

- Martin Marietta Materials (MLM) 8:05am, $(0.24)

- Ecolab (ECL) 8:25am, $0.48

- FirstEnergy (FE) 8:30am, $0.80

- CBOE Holdings (CBOE) 4pm, $0.36

- Motorola Mobility Holdings (MMI) 4pm, $0.01

- Unum Group (UNM) 4pm, $0.76

- WebMD Health (WBMD) 4pm, $(0.18)

- CBS (CBS) 4:01pm, $0.44

- Chesapeake Energy (CHK) 4:01pm, $0.28

- DaVita (DVA) 4:01pm, $1.45

- Fiserv (FISV) 4:01pm, $1.14

- TripAdvisor (TRIP) 4:01pm, $0.34

- Broadcom (BRCM) 4:05pm, $0.55

- ONEOK (OKE) 4:05pm, $1.31

- OpenTable (OPEN) 4:05pm, $0.34

- Genworth Financial (GNW) 4:07pm, $0.13

- Arthur J Gallagher & Co (AJG) 4:11pm, $0.26

- TECO Energy (TE) 4:15pm, $0.24

- Yamana Gold (YRI CN) 4:28pm, $0.24

- Boston Properties (BXP) Post-Mkt, $1.13

- General Growth Properties (GGP) Post-Mkt, $0.21

- Intact Financial (IFC CN) Post-Mkt, C$1.26

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Fat Pigs Means Pork Bust as Record Herd Ends Rally: Commodities

- Jeremy Charles Will Retire as HSBC’s Head of Precious Metals

- Corn Declines as U.S. Planting Progress May Boost Global Supply

- Oil Near Two-Day Low After China PMI Expands Less Than Forecast

- Sugar Falls as Delivery Seen Bigger Than Forecast; Coffee Drops

- Copper Swings Between Gains, Drops Amid Doubt About China Easing

- Gold Is Seen Falling on Concern Physical Purchases Are Slowing

- U.S. Lags in Cattle ID Seen as More Effective Than Mad Cow Tests

- Aluminum Set to Strengthen in Next 10 Days: Technical Analysis

- Rubber Gains for Fourth Day as China’s Manufacturing Expands

- Wind’s $168 Billion North Sea Boom Lures Oil Industry: Energy

- Utility Puts Hit Record in Bet Against Defensive Rally: Options

- Batista Considers Industrial Partner to Tap $1.5 Trillion Assets

- Pork Surplus May End Four-Year Price Rally

- Kansas Draws Record 100 to Measure Wheat in World’s Top Exporter

- Oil Supplies Surge to 21-Year High in Survey: Energy Markets

- Record Fuel Output Returning Exmar’s Tankers to Profit: Freight

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

JAPAN – while we were lugging around our 100 slide deck presentation on Japan in March, the most common question was “what’s the catalyst to make Japanese stocks go down?” A: economic gravity. Just when consensus thought Japan couldn’t go down it’s down for 15 of the last 19 trading days (down hard, -1.8% overnight).

MIDDLE EAST

The Hedgeye Macro Team