Very Bullish Senior Loan Officer Survey in All but One Category

The Fed released its second quarter Senior Loan Officer Survey yesterday afternoon. The survey covers lending standards and loan demand and was conducted between March 27th and April 10th.

Overall, the survey paints a very positive picture, though admittedly is somewhat backward looking given the survey period was 3-5 weeks ago. Across C&I and CRE loans, lending standards eased while loan demand improved. On the consumer side, residential mortgage demand rose significantly. That said, lending standards tightened modestly for both prime and nontraditional borrowers. Consumer non-mortgage loans saw lending standards ease again this quarter and demand strengthened considerably. Most notably, banks willingness to make auto loans increased substantially.

We saw relatively strong loan growth trends from a majority of the regional banks in 1Q12. This survey suggests that those trends should persist through 2Q12, barring any sharp loss of confidence intra-quarter.

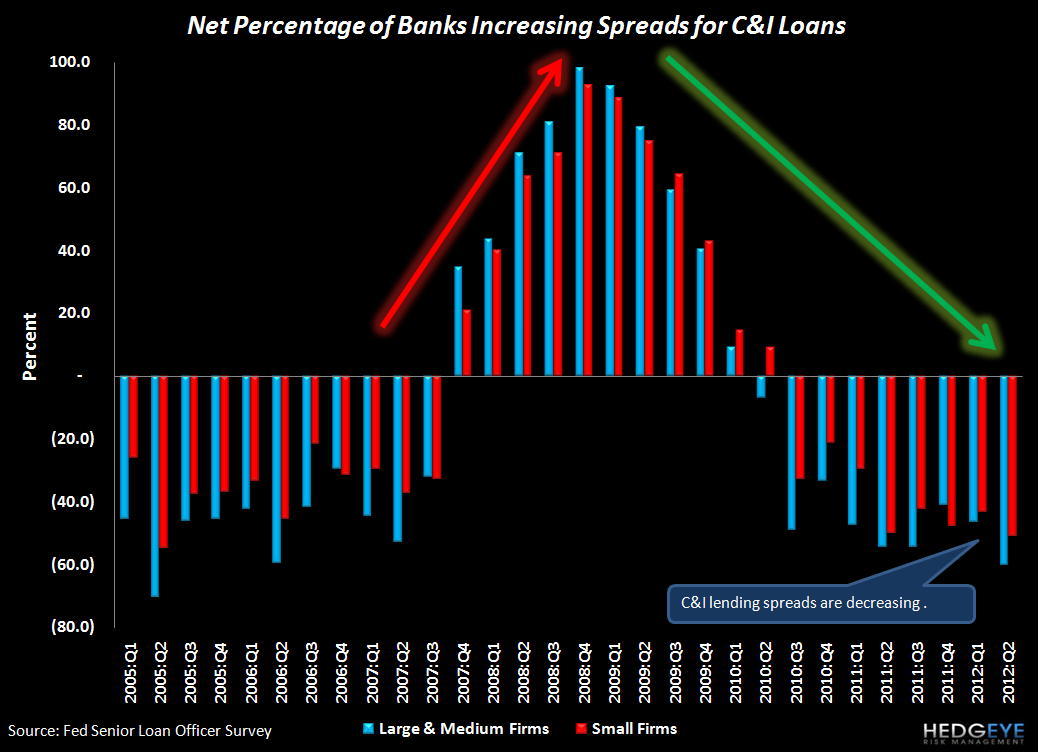

C&I Loan Demand Rises Sharply

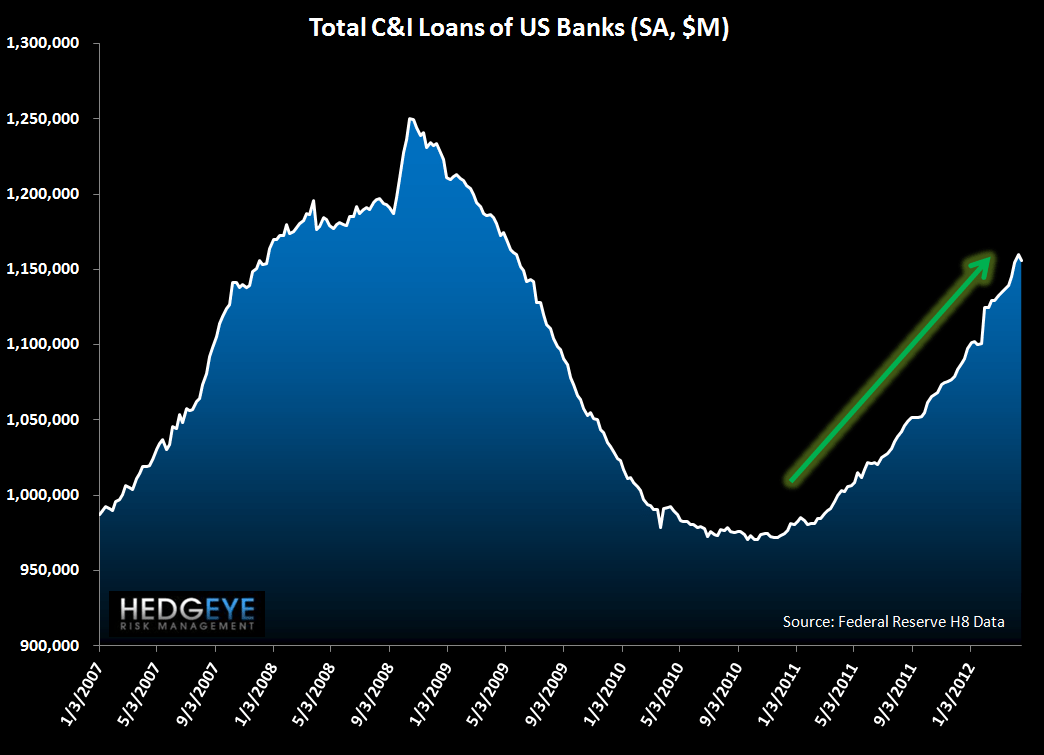

Demand for C&I loans continued to rise in the 2Q survey, spreads tightened, and standards continued to ease. The Loan growth in C&I remains the strongest out of any loan category, according to the Fed's H.8 data.

Notably, a net 60% of banks reported not tightening spreads for large and mid-size firms, while a net 31% of banks reported stronger demand for C&I loans among large and mid-size borrowers.

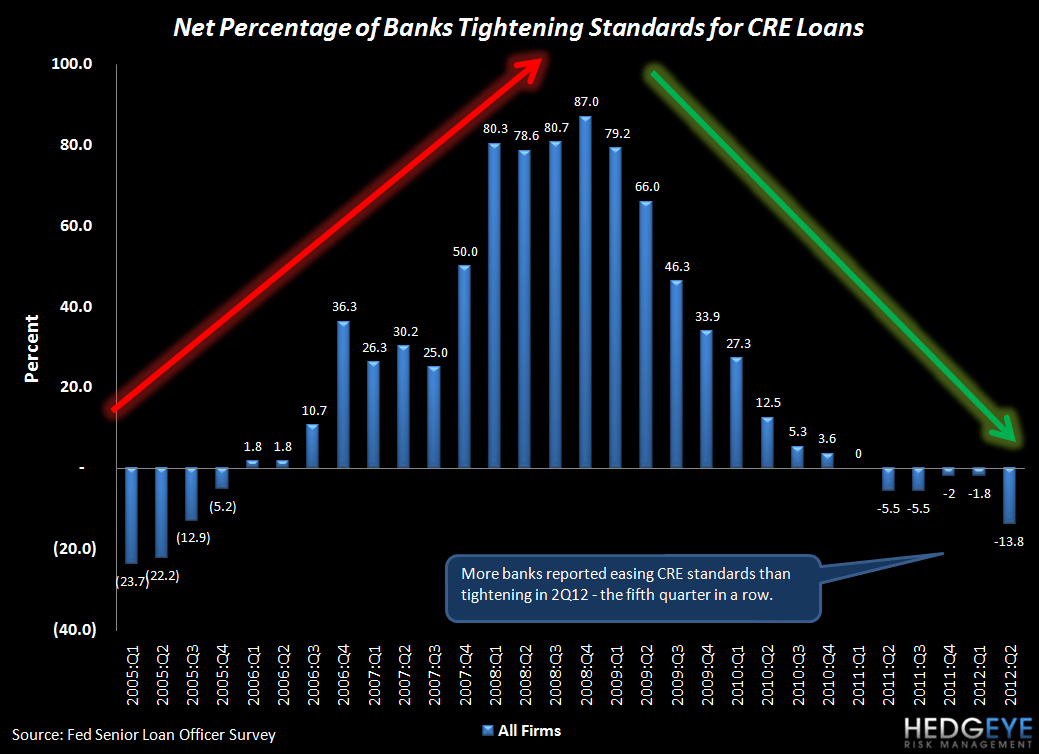

CRE Loan Demand Rises Further While Standards Continue to Ease

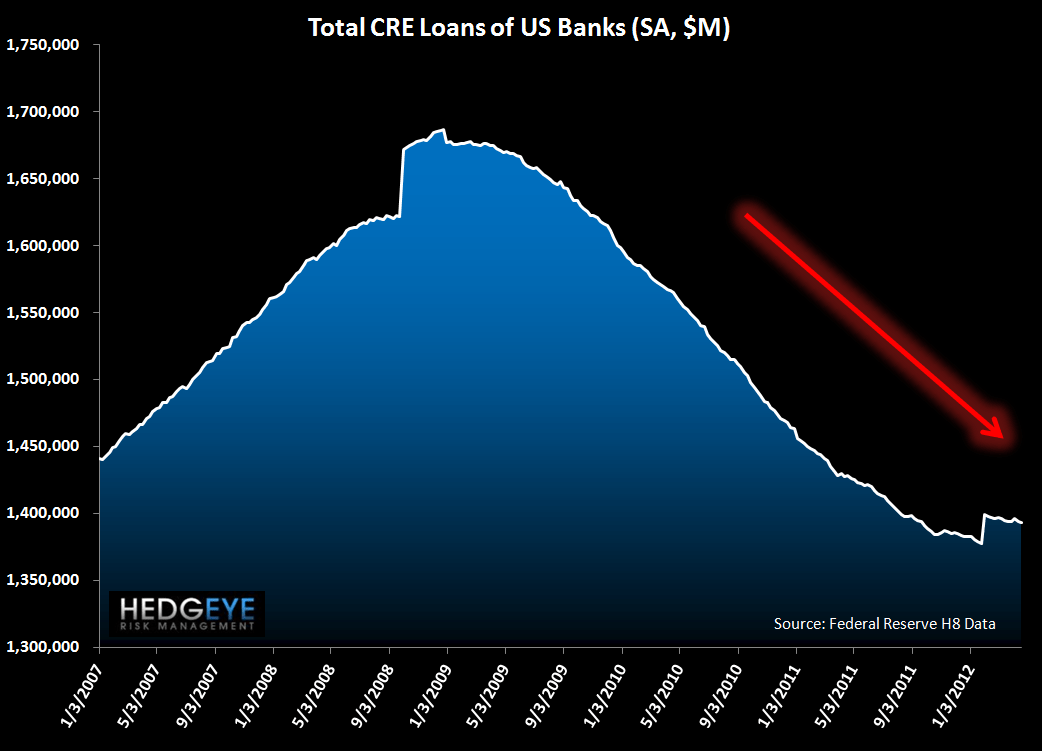

Commercial real estate loan demand improved in the quarter with a net 39.7% of banks reporting stronger demand for CRE loans. Meanwhile, a net 13.8% of banks reported easing CRE loan standards 2Q12 - the highest percentage recorded since the downturn began. In spite of the turn in this data, H8 data shows that CRE loans, overall, remain in decline.

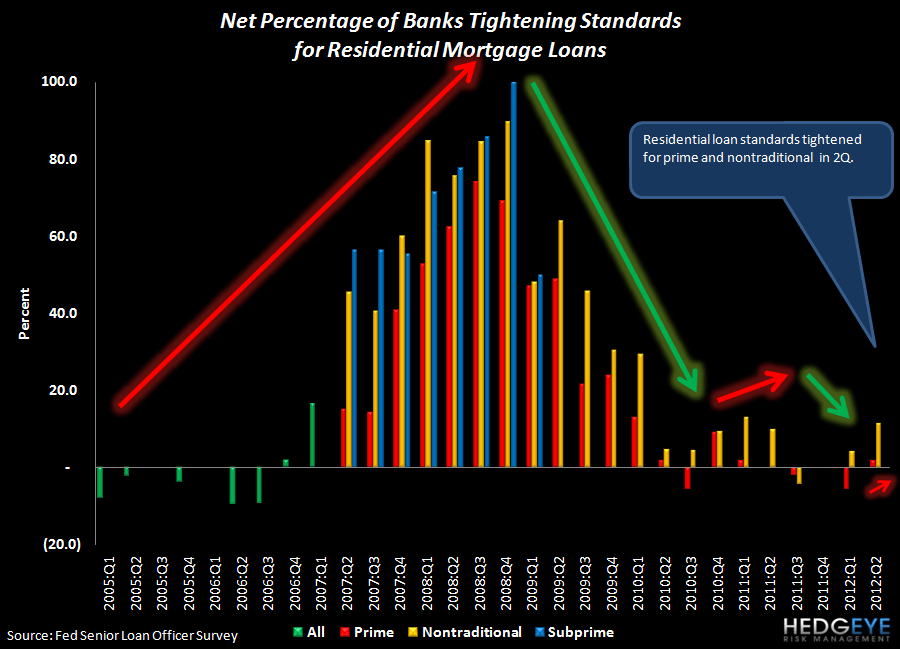

Residential Real Estate - A Mixed Picture

Residential mortgage loan standards were tighter in 2Q for both prime and nontraditional borrowers. A net 1.9% of banks reported tightening standards on prime borrowers, while a net 11.5% of banks reported further tightening on nontraditional borrowers.

The demand side, however, saw the sharpest uptick in demand since the housing downturn began. Demand was reported as stronger for prime residential loans by a net 30.2% of banks, while a net 23.1% of banks reported stronger nontraditional loan demand.

Consumer Loans - Cards, Cars & Installment

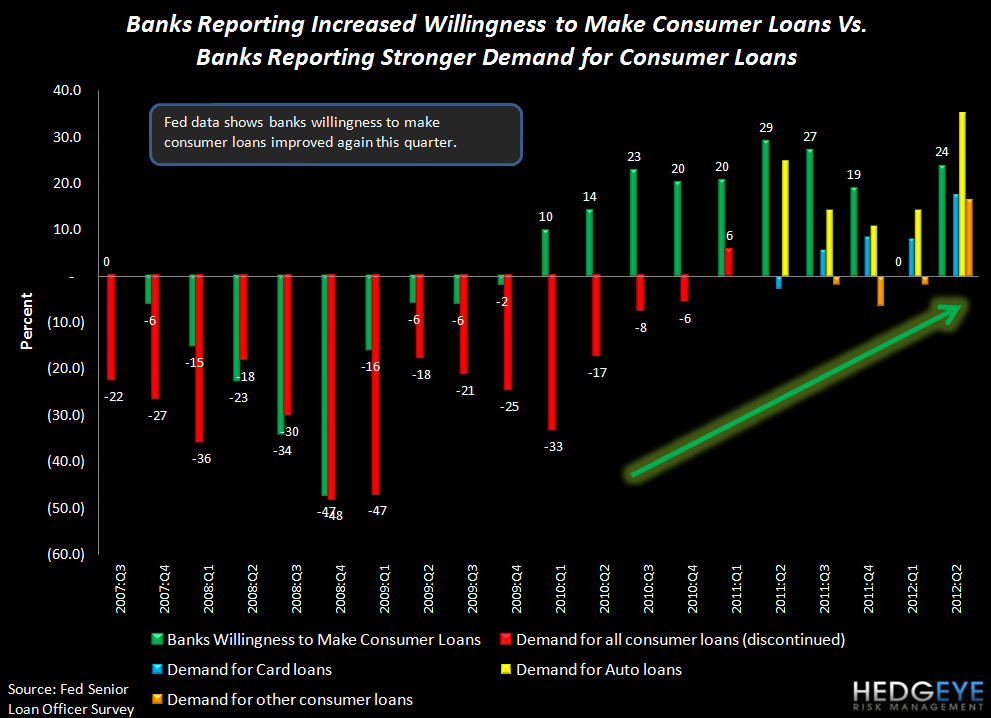

Banks reported a net easing of standards for credit cards, auto loans and installment credit. This survey was roughly in-line with that of recent surveys. On the demand front, demand picked up sharply. Demand for credit card loans rose to a net 17.5% of banks from 8.1% in the prior quarter. Demand for auto loans rose to a net 35.3% from 14.3% in the prior quarter and installment loan demand picked up to a net 16.4% from negative 1.9%. These are very positive readings on the demand front. Finally, This quarter also saw a net 23.6% of banks report an increased willingness to make consumer loans. This is roughly consistent with the readings from the last several quarters.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link below to view in your browser.