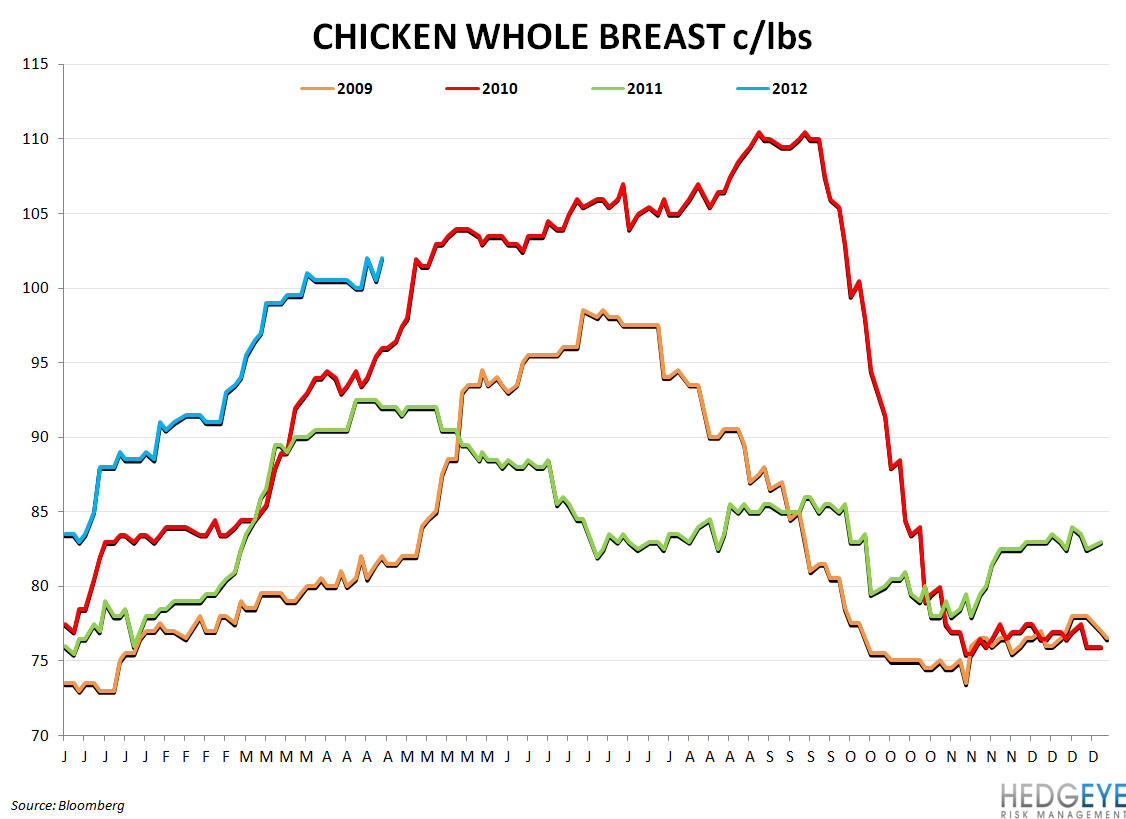

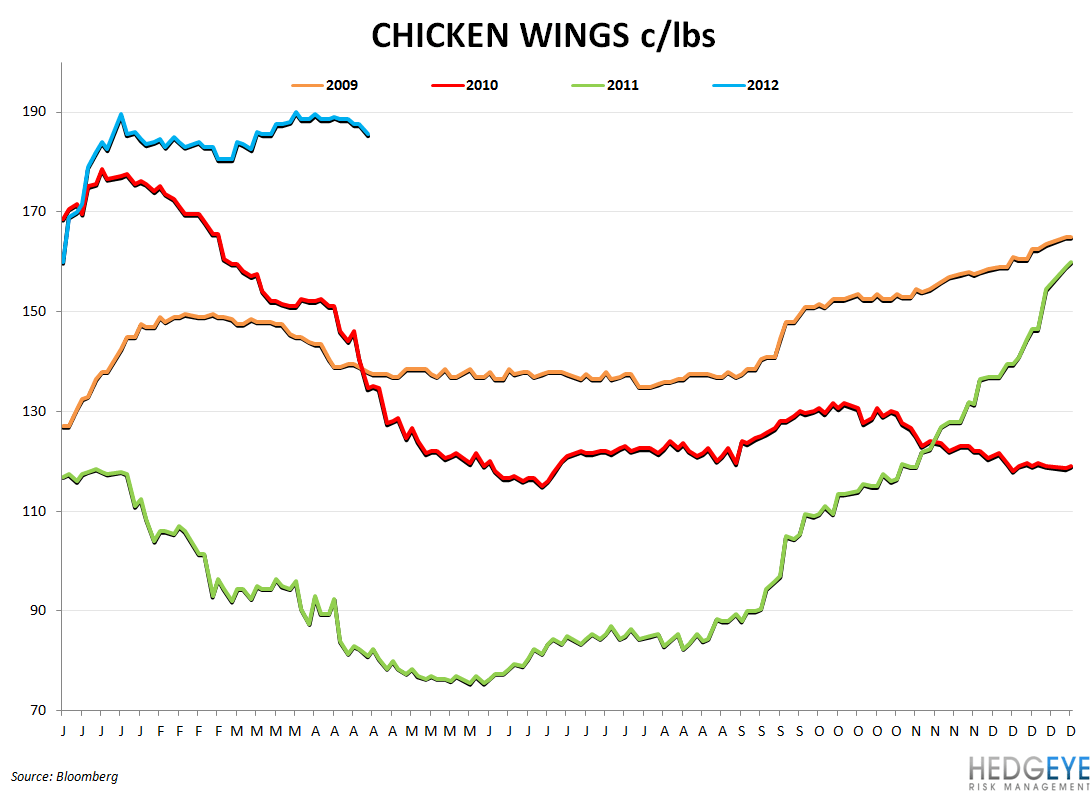

Today’s upgrade of BWLD (by an analyst that made a superb call downgrading the company right at the top) centered on the conversation about chicken wing prices turning from “higher prices” to “lower prices” and the impact that would have. In the same paragraph, in highlighting the sensitivity between the year-over-year change in wing prices and EPS, the report reminded us of the truth: cents per pound do not matter as much as year-over-year inflation for BWLD earnings.

Another notion supported by the upgrade was that egg sets and chick placements are lapping last year’s decline and, therefore, are likely to be supportive of moderating wing prices. That may be true but, pertaining to BWLD; the question is whether or not it will come soon enough to save 2Q. For two reasons, we do not think it will.

- Egg sets will likely not increase, year-over-year, until the last week of the second quarter even under aggressive assumptions.

- Even if we are wrong on #1, the actual supply of chicken does not influence the market for two months. Egg sets being placed today reflect chickens that will hit the market in the last days of 2Q. Demand in the summer months is also expected to be strong, according to SAFM.

Conversation about chicken wing prices moving lower will not change the likelihood that BWLD misses 2Q as costs increase as a percentage of sales and comps decelerate sequentially. As the chart below illustrates, as of 4/20, the leading indicator of supply – egg sets – is declining ~5% year-over-year. We expect that line to remain negative through June.

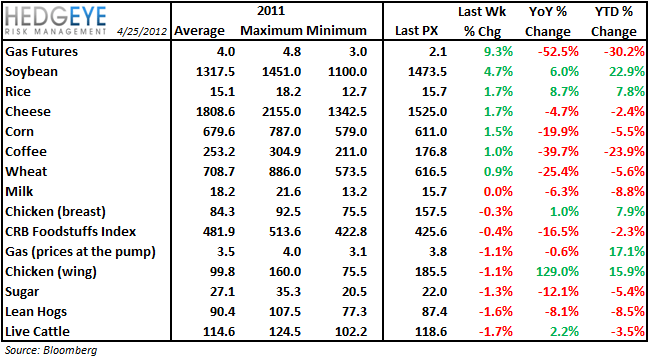

COMMODITY TABLE

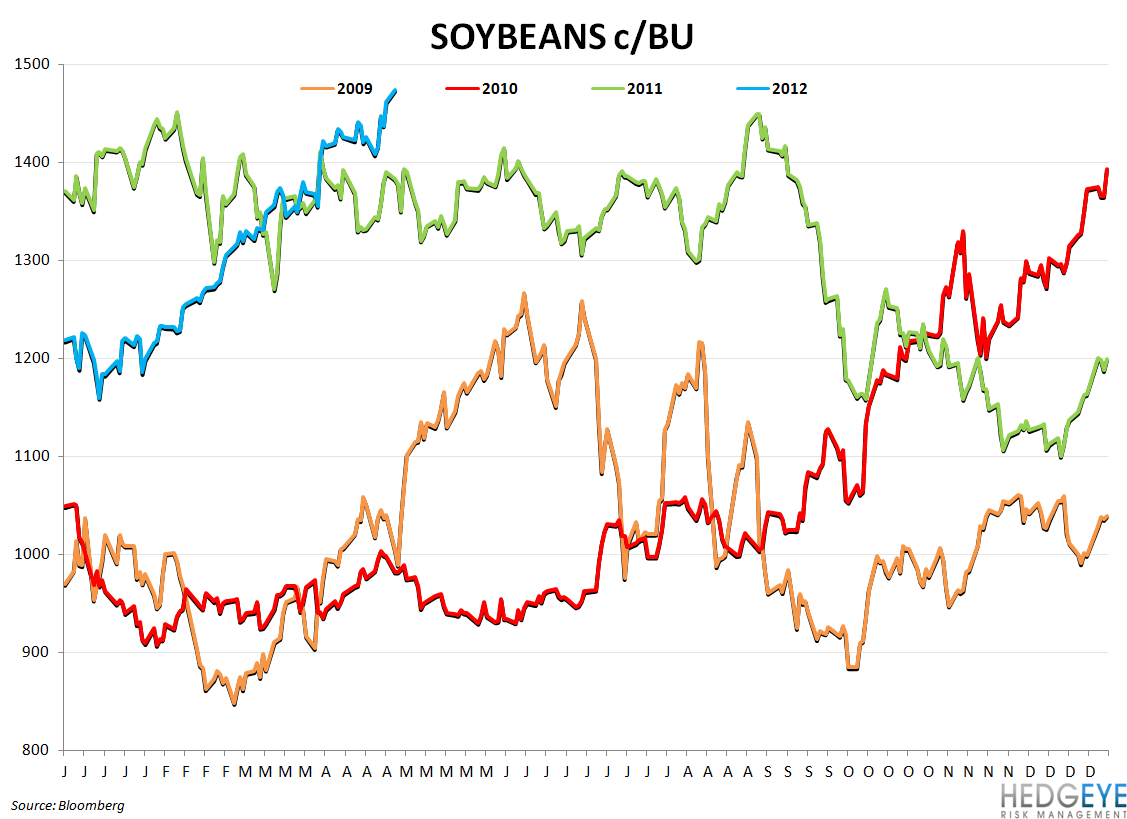

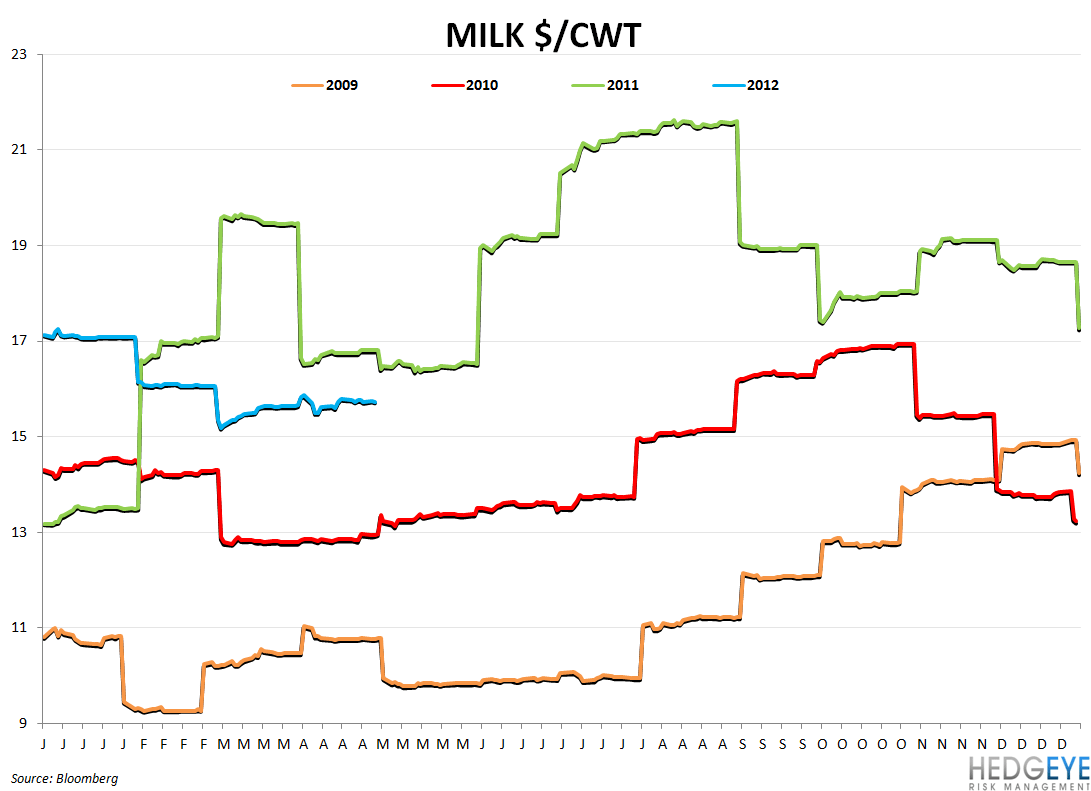

Overall, proteins moved lower last week while grains, dairy, and coffee moved higher. Beef prices were hit by the BSE news but it seems that the livestock disease “firewall” in the U.S. food system was effective. Larry Hollis, beef veterinarian at K-State, commented on CattleNetwork that the particular strain of BSE that was detected in the animal in question is unlikely to involve any transmission to another animal or consumers. The condition did not, apparently, arise from any feed but rather was naturally occurring and the “firewall” procedures in place worked well to identify this one instance.

Coinciding with the concern around “pink slime” or Lean Finely Textured Beef, the news was certainly not positive for beef prices. The market today seemed to reflect a degree of stability in beef prices. Japan, Canada, and the European Union today said that they’ll continue to import American beef.

CORRELATION TABLE

CHARTS

Howard Penney

Managing Director

Rory Green

Analyst