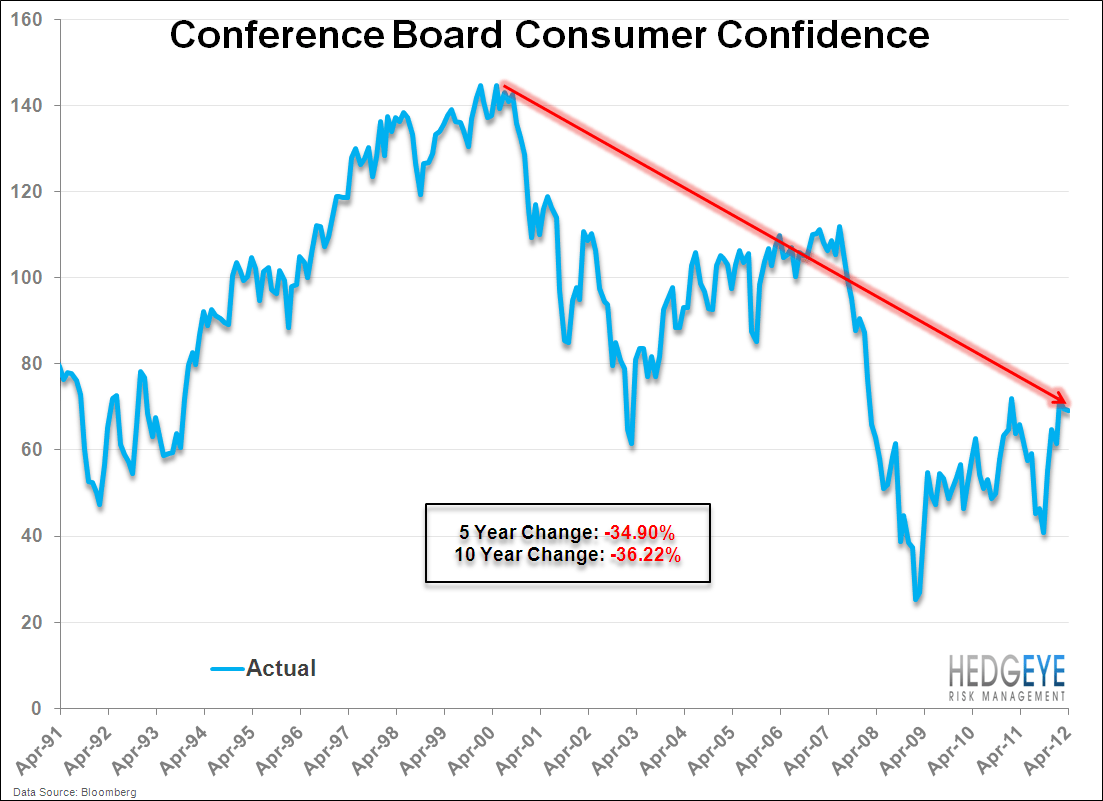

Conclusion: Consumer confidence declined sequentially with a meaningful drop off related to the auto and major appliance sector.

Last week, we used a quote from Charles Dickens’ A Tale of Two Cities that started, “It was the best of times, It was the worst of times”. Today’s consumer confidence seems to further exemplify the confused nature of the U.S. economy. At 69.2, consumer confidence for April decreased 0.43% MoM, more significantly it was down -1.43% from March’s unrevised number of 70.2. The indicator has increased 4.8% YoY, yet it is still far from signaling a healthy economy, which would require a reading of at least 90. Consumers’ confidence have not reflected a strong economy since December 2007, at a level of 90.6. The average confidence reading for 2010, 2011, and 2012 YTD is 54.49, 58.13, and 67.95 respectively. April’s statistic is the second consecutive decline since a level of 71.6 in February (which was the highest data point since February 2011).

Although there were some segments within the index that experienced positive movements, largely the outlook does not appear favorable. The measure of those who believe business conditions are “good” increased from 14.3% to 15.3%, yet those who view the business conditions as “bad” also increased from 33.2% to 33.5%. Those expecting the business conditions to worsen rose from 13.7% to 14.2% and the measure of consumers anticipating the business conditions to improve dropped from 19.3% to 18.8%. Consumers viewing jobs as “hard to get” declined from 40.7% to 37.5%, however those stating jobs are “plentiful” contracted from 9.0% to 8.4%. The outlook that there will be fewer jobs in the months ahead fell from 18.5% to 18.0% as did the opinion that there would be more jobs, which decreased from 17.4% to 16.9%. The fraction of people anticipating a raise from their current employers decreased from 15.5% to 14.0%.

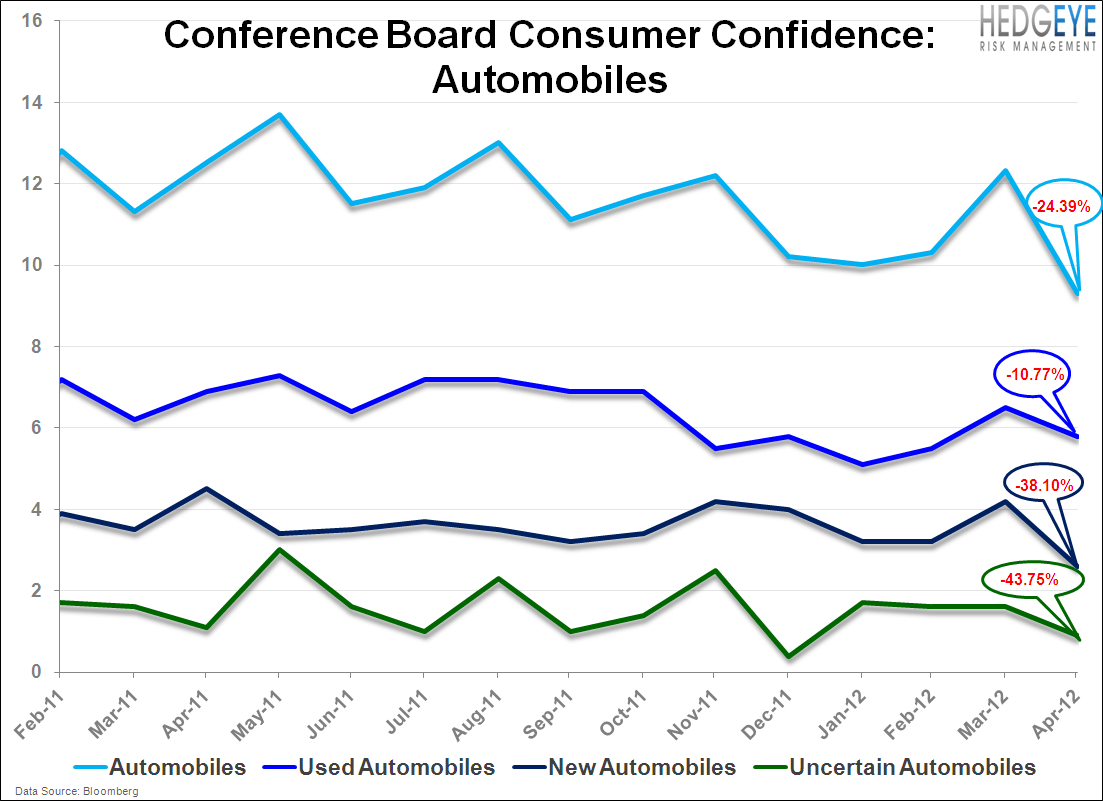

The proportion of consumers expecting business conditions to improve over the next six months declined from 19.3% to 18.8% and consumers who believe business conditions will worsen increased from 13.7% to 14.2%. Consumer confidence in major appliances decreased 14.05% MoM and 15.01% YoY, and consumer outlook in the automobile industry was also decisively negative. Some of the readings contradict each other, swinging from slightly positive to slightly negative, yet it is evident that the slow paced “recovery” is definitely not increasing its pace based on the latest consumer confidence measure.

Daryl G. Jones

Director of Research