McDonald’s continues to be the de facto safety trade of the restaurant space. Our opinion at this point is that there are some subtle changes taking place as the new Chief Executive Office takes over that are worth noting.

On Friday we took the opportunity to ask Don Thompson what he thinks his legacy will be when he finds himself – hopefully long from now – closing in on retirement as Jim Skinner currently is. His response was, in our view, interesting in that he mentioned the “Plan to Win” but also spoke of the importance of growing organically and building new restaurants coincidentally. Specifically, Thompson stated that “we are much smarter now” and that McDonald’s “can walk and chew gum at the same time” [organic unit growth]. We do not view this as a negative for the company but it does represent a lower return growth profile for the company than we have seen over the past five years.

Thompson’s three “global priorities” are:

- Optimizing the menu [transitioning from dollar menu]

- Modernizing the customer experience [remodel/reimage program]

- Broadening accessibility to Brand McDonald’s [unit growth]

Unfortunately, the McDonald’s conference call was littered with headwinds facing the company that are, on a relative basis, greater than those facing competitors such as Yum Brands. McDonald’s highlighted three major hurdles facing the company in 2012. Firstly, the economic climate remains challenging, particularly in Europe. Secondly, consumer confidence remains varied across markets. Finally, the company highlighted “economic pressures and inflationary costs”. Beef has been a key driver of these cost pressures.

Simply comparing McDonald’s to Yum Brands under the specter of these three factors paints McDonald’s in an unfavorable light relative to its rival. Yum has shrugged off concerns related to China’s rate of growth but McDonald’s’ exposure to Europe seems to be causing some concern among management personnel and investors alike.

WHAT WAS NOT SAID

Changes on the margin are all-important and we see the decrease in emphasis on beverages as a strategy going forward as being important. While management said that “the U.S. also continues to strengthen its position as a as a beverage destination”, total beverage units were only up 6% versus up 20% in 4Q11, 16% in 3Q11, and 29% in 2Q11. In fact, the word “beverage” was only mentioned twice on the 1Q12 call. The 4Q11, 3Q11, and 2Q11 calls included 4, 8, and 18 mentions of the word “beverage”, respectively. The word “McCafé” was mentioned twice on the 1Q12 call. The 4Q11, 3Q11, and 2Q11 calls included zero, 7, and 11 mentions of the word “McCafé”, respectively.

The evidence suggests that beverages are increasingly becoming a less important part of the vocabulary from McDonald’s’ management team. With that in mind, foremost in our thoughts is what the company’s strategy will be to maintain top-line momentum over the next few months.

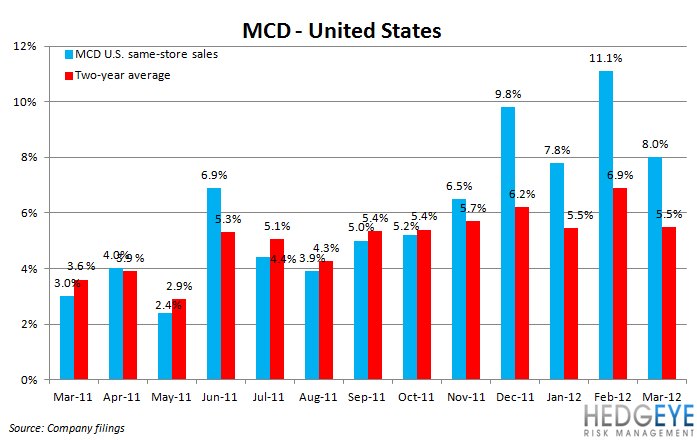

UNITED STATES

The beverage initiative last year clearly helped McDonald’s take share from competitors. Don Thompson did provide an interesting take on the industry when he said, “around the world we continue to gain market share in an industry with minimal-to-negative growth”. For a frame of reference, the Justice Holdings presentation touting the upcoming Burger King presentation cited an industry growth number of +6%!

For McDonald’s, one of the core initiatives in the U.S. this year is an attempt to evolve the company’s value proposition with the new Extra Value Menu and, in doing so, turn away from the existing dollar menu. Beginning in April, McDonald’s is focusing the menu on four tiers (excluding combo meals):

- Premium ($4.50-5.50)

- Core ($3.50-4.50)

- The new Extra Value Menu ($1.20-3.50)

- The Dollar Menu

Given that the company is guiding to 4.5-5.5% inflation in the U.S. in 2012, we believe that management is attempting to manage check and margin by forcing customers to trade up to the Extra Value Menu from the Dollar Menu. This belief is supported by the fact that one of the biggest changes that the company is undertaking is the addition of fresh baked cookies and ice cream cones to the Dollar Menu in place of small drinks and small fries.

Our view remains that this is a big risk for McDonald’s. If this change goes against consumer preference, there is a

possibility that satisfaction scores will be negatively impacted. When we spoke to the company in March when the menu changes were first announced, we learned that a “mini-combo meal” offering may bundle the fries, burger, and drink but a decision has not been made on that yet. Still, ordering the $1 items individually is no longer an option.

EUROPE

Turning to Europe, McDonald’s has been significantly impacted by the macroeconomic environment there, more so than any other multi-national restaurant company due to its relatively larger exposure to the region. Europe represents 40% of total revenues for McDonald’s and 39% of operating profit. As Don Thompson said, Europe is a region that “continues to experience unprecedented economic challenges from widespread austerity measures, concerns over the sovereign debt crisis and unemployment levels averaging about 10%”.

The company has long been focused on upgrading the customer experience; 80% of the system’s interiors have been refreshed as well as 50% of the exteriors. Roughly 150 McCafés will be added to the Europe system in 2012.

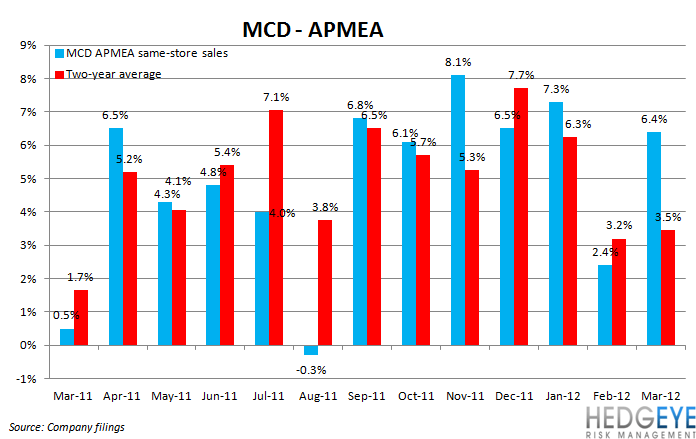

APMEA

In APMEA, McDonald’s called out the challenging economic conditions in China (8.5% same-store sales), ongoing “tightening” in Australia, and uneven results in Japan. Again, the company is looking to value as a strategy with the recent launch of the Loose Change Menu in Australia last month.

We think that APMEA is an important component of the long-term strategy for McDonald’s but, given that it only comprises 18% of EBIT, the near term story will be dictated far more by business in the US and Europe, which account for 43% and 38% of EBIT, respectively.

CONCLUSION

McDonald’s trends are not disastrous but going forward, we see plenty to be concerned about. Specifically, lapping the outsized performance of the U.S. business last summer, which was driven by impressive beverage sales, and maintaining momentum in Europe are two key issues. As we wrote earlier, beverage unit growth is sequentially slowing so we believe that catalyst is no longer a major factor.

Given the pending IPO of Burger King and our view that the brand is “too big to fix”, it struck a chord when McDonald’s management emphasized that it is “willing and able to invest for continued growth and to widen our competitive advantages”. In reimaging 2,400 restaurants globally (800 U.S., 900 Europe, and 475 APMEA) and rebuilding 200 U.S. locations, the company is clearly in a position of strength versus its closest rivals. The longer-term outlook for McDonald’s is positive, with competitors like Wendy’s and Burger King floundering, but growth in that segment of quick service pales in comparison to fast casual/specialty. We would look elsewhere for top long QSR ideas at this price. Jack in the Box is one company that we believe has upside potential from here.

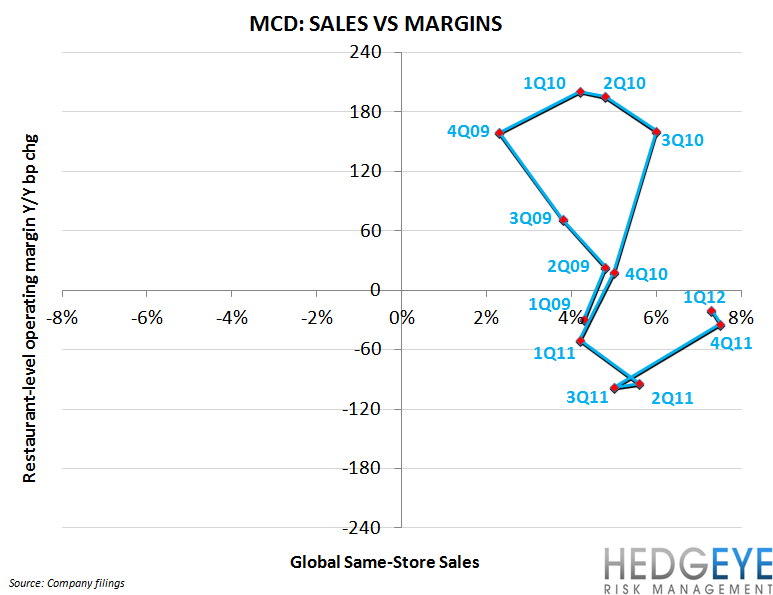

Globally, the price factor flowing through the company’s income statement is roughly 3%. With inflation pressuring margins, particularly in the U.S., sales trends will take on an increased importance. Given the difficult top-line compares and uncertainty around the transition from Dollar Menu to Extra Value Menu, our conviction on the top-line continuing to meet consensus is tenuous at best.

Howard Penney

Managing Director

Rory Green

Analyst