THE HEDGEYE BREAKFAST MONITOR

HEDGEYE VIRTUAL PORTFOLIO POSITIONS

LONGS: JACK, SBUX

SHORTS:

MACRO NOTES

Commentary from CEO Keith McCullough

I believe my competitor at ISI is calling it a “Growth Problem Alert” today – we’ve been calling it #GrowthSlowing since Feb:

- GROWTH SLOWING – when we say that, we mean it globally. The words USA “de-coupling” is an Old Wall St word that has not worked in the last 5yrs. The world is as globally interconnected as it’s ever been and what policy does to the world’s reserve currency has very consequential impact on the intermediate-term slopes of growth and inflation.

- EUROPE – Spanish stocks are crashing again (down -23% since Growth Slowing started, globally in Feb – Hong Kong and India stock markets stopped going up in Feb too). The French Services PMI print for April was awful (46.1 vs 50.1 MAR) and Italian consumer confidence just hit a record low. Central planning not working. DAX snapping TREND support (6689).

- COPPER – the Doctor is getting tagged this morning, down -1.7% and in a Bearish Formation (bearish TRADE, TREND, and TAIL in our model). Commodity prices (or Bernanke’s Bubbles) look a lot like US Treasury Yields again. 10yr yield getting smoked to a fresh 2mth #GrowthSlowing low of 1.93%.

Next SP500 support = 1356.

SUBSECTOR PERFORMANCE

QUICK SERVICE

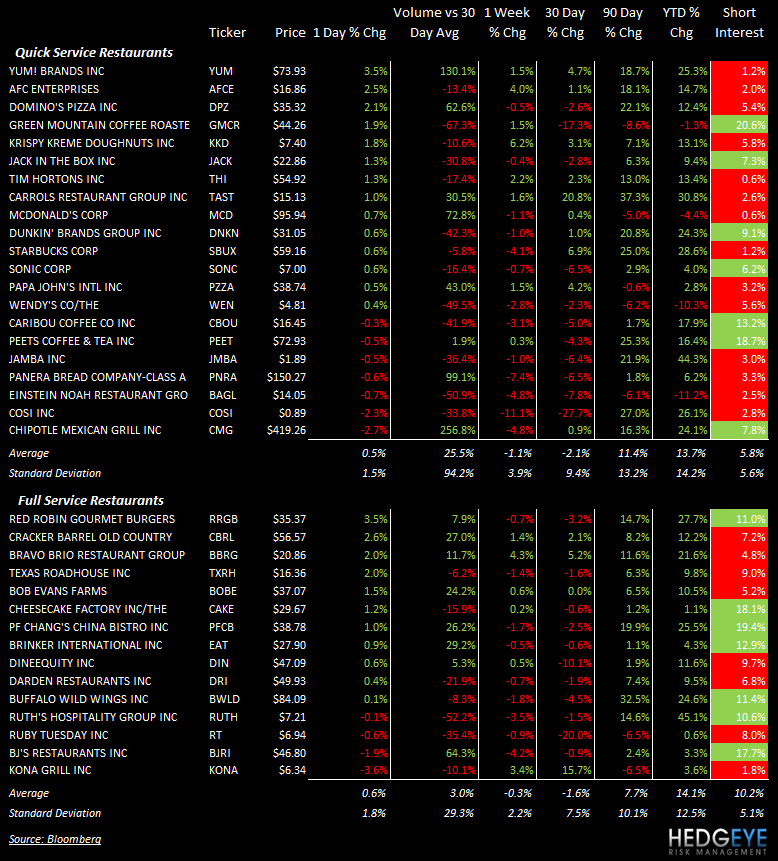

MCD: McDonald’s CEO Jim Skinner highlighted jobless claims during the conference call on Friday as being indicative of the soft macro environment.

DPZ: Domino’s holder Trian reported a passive stake of 4.4% down 7.2% in value at the end of 2011.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

YUM: Yum Brands traded up 3.5% on accelerating volume.

CMG: Chipotle traded down -2.7% on accelerating volume.

CASUAL DINING

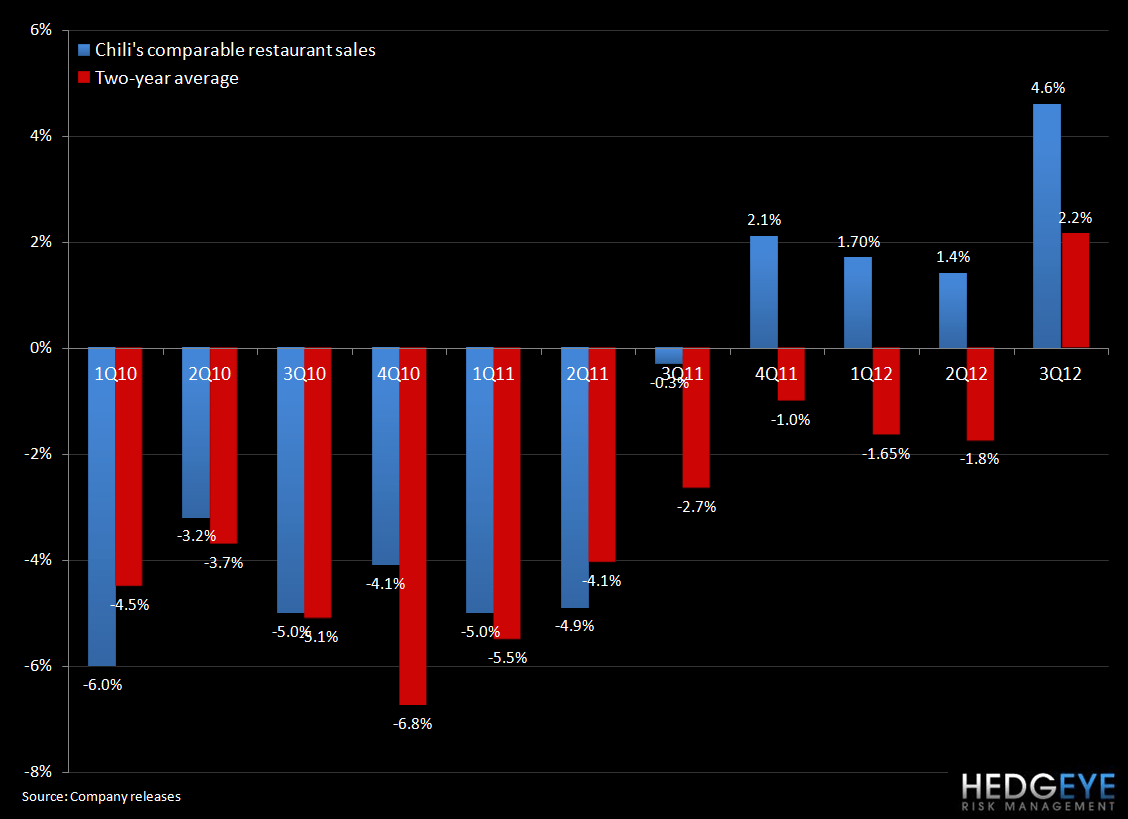

EAT: Impressive numbers out of Brinker today. 3QFY12 EPS came in at $0.60 versus $0.56 consensus and company-owned comparable restaurant sales at Chili’s came in at 4.6% versus 2.3% consensus. As the charts below illustrate, Chili’s made significant progress on the top line. Two-year average trends improved significantly on a sequential basis despite the more difficult compare and lapping of the introduction of the lunch promotion in January 2011. How much of that successful lapping was due to weather is the question of the day. Any forward looking commentary from management pertaining to April trends will likely have a significant impact on where the stock ends up at the close today. From what we know, it seems that traffic slowed over the duration of the quarter at Chili’s; traffic was up 1.8% for the quarter but March came in at +0.5%.

CAKE: Cheesecake Factory’s CEO, David Overton, was paid $4.1m for FY11, according to filings made with the SEC. In 2010, he received $3.7m total compensation.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

CBRL: Cracker Barrel bounced back after a soft day’s trading on Thursday. Shareholder Sardar Biglari is trying to shake things up at the company. Friday the stock closed above Thursday’s high.

BJRI: BJ’s Restaurants traded down on accelerating volume on Friday. The stock received an upgrade on April 12thbut has sold off since.

Howard Penney

Managing Director

Rory Green

Analyst