Last week, we expressed our concerns about the casual dining sector’s sales trends in March and early April. Almost any exposure to the category has returned handsome gains to shareholders over the past six months. We think taking a little money off the table is a wise move at this point. Below we run through our thoughts on several names including our (relative) favorite longs and which stocks we see as the best shorts at this time.

There has been a significant amount of volatility in the casual dining space over the past three and six months, in particular. We will begin by looking at the category’s recent price action together with sentiment, valuation, the macroeconomic outlook and – in the last section of this post – our current view on company-specific factors we see as important for several individual stocks.

Casual Dining

Our Casual Dining Index has appreciated greatly since the equity markets bottomed in October 2011. The chart below shows how tightly correlated (on an inverse basis) the Casual Dining Index is to Initial Jobless Claims. If Hedgeye’s call on growth slowing is correct, then a softer employment market could bring a sustained correction in casual dining stocks. Furthermore, the “Ghost of Lehman” effect on jobless claims that has been boosting headline numbers because of a distortion in the seasonal adjustment factor for much of this year-to-date has dissipated and is set to reverse in a few months. We wrote about this topic in early March after the Financials team, led by Josh Steiner, first published on it in great detail.

In terms of the near-term sales outlook, we would highlight the recently released Blackbox Intelligence data that shows 1Q12 casual dining same-store sales increased +1.7% including a -1.2% move in traffic. The March numbers were particularly disappointing, coming in at -0.2% and -3.4% for same-store sales and traffic, respectively.

Price

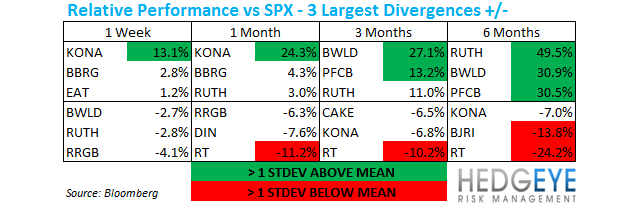

Looking at the divergences shown in the table below, we can see that several stocks have seen substantial outperformance versus the broader equity market over the last six months and, given Hedgeye’s view on growth slowing, along with the fact that the industry outlook is deteriorating, it is worth refreshing our thoughts both on casual dining and some individual stocks. We will focus on PFCB, BWLD, and EAT in our company commentary at the end of the note.

Valuation

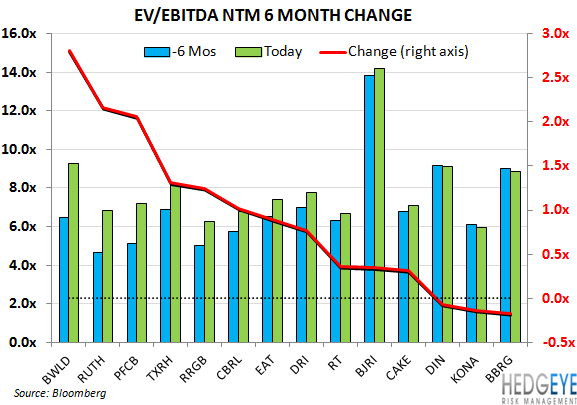

In terms of valuation, we can see that with the exception of KONA, DIN, and BBRG, consensus has valued the casual dining space significantly higher over the past six months. BWLD is the standout from the chart below with its EV/EBITDA NTM multiple increasing by almost three turns over the past six months. PFCB has also seen a large appreciation in its multiple along with RUTH and TXRH. The contraction of DineEquity’s multiple is notable; a heavily-franchised industry leader should not have traded as poorly as this stock has over the past six months, particularly when a competitor – EAT – has traded so well.

Sentiment

Sell-side analysts have been cautious on casual dining for some time, remaining so despite the generally strong price action. Buy-side investors, too, have preferred QSR and Fast Casual as a means to gain exposure to restaurants and this shows in our Casual Dining Sentiment Scorecard, below. With so much upside apparent, it seems that there could be some risk to adopting an overtly bearish stance at this point; it is possible that the macroeconomic fears currently weighing on sentiment could be dismissed or postponed if employment growth continues to be positive and gas prices fail to impact the American summer driving season as much as many seem to be anticipating. In that scenario, investors that have been looking to QSR rather than Casual Dining may change course and boost the group higher. We are not anticipating that as we see restaurant industry data corroborate our macro team’s view that growth is slowing as inflation accelerates, but we believe it is worth highlighting the risks to our current stance. Being selective on the short side, however, we see several attractive opportunities that we will discuss below.

PFCB and EAT are still the undesirables of the casual dining space and we view that as a positive for the longer-term TAIL story of both of these stocks. DRI remains the bellwether for the space with investors generally remaining neutral-to-positive on the stock.

P.F. Chang’s

P.F. Chang’s has been a favorite name of ours since February 6th. In that note, “PFCB – TURNING THE QUEEN MARY”, we wrote: “We’re confident that the current consensuses of $1.61 for 2012 is not reliable in that there are several estimates included in that number of $1.80 where, our guess would be, the analyst responsible has not updated his/her model for a while.” That turned out to be correct, and the FY12 EPS estimate is now at a much more realistic $1.56. In that same note, we also said that we would be buyers of PFCB on down days for the ensuing three months.

While we expected the three month period starting February 6thto be positive for PFCB, it is fair to say at this point that the ~14% gain since then has been above our expectations at the time. At this point, we remain positive on the longer-term TAIL but would not be buyers here.

From a price perspective, as we mentioned, the 14% gain since we turned positive on February 6thhas exceeded our expectations. Relative to the S&P 500, the stock has outperformed by ~1100 bps.

Our style does not anchor heavily on valuation but back in late 2011 when we began considering this name as a possible long, it traded as low as 5.5x EV/EBITDA NTM (consensus). At that point, we were seeing a business that was clearly in disarray but also a management team that was no longer skirting around the issues. With a sum of the parts analysis indicating at that point that downside was limited and management’s change in tone, improving macro trends led us to turn positive on the stock in February. Now, the situation has changed. The stock is valued a turn higher and while steps are clearly in place to fix the business, there is now some downside risk and less likelihood, in our view, of incremental positive news over the next three months or so.

For P.F. Chang’s, like most casual dining concepts, employment growth is an important driver of its business. Excluding the impact of self-inflicted wounds, the realization of which led investors to exit the stock en masse for the first nine months of 2011, this stock has largely followed inverted rolling claims, as the chart below shows. The correlation over the duration of the chart below is weak but, as the investment community gained clarity on the company’s plan going forward, the stock traded more in line with the space. From October to present, the correlation between the two data sets shown in the chart below is -0.87 (the scale on the left axis is inverted) and has been getting progressively tighter.

In short, we believe that the dislocation that existed between P.F. Chang’s and the rest of the casual dining space has largely been corrected. From a sentiment perspective, there is more fuel in the tank; the sell-side remains bearish on the name and short interest, although has varied between 36% and 19% over the last three years, is currently at the low end of that range.

Going forward, how the stock trades from here is largely dependent on the impact of the new lunch initiative at the Bistro together with the overall macro environment (typified by initial claims). P.F. Chang’s reminds us in many ways of Brinker in mid-2010. Obviously Brinker’s subsequent resurgence depended on market conditions, several other well-executed initiatives, and other company-specific factors. We will continue to frame our view of P.F. Chang’s in the same way.

Buffalo Wild Wings

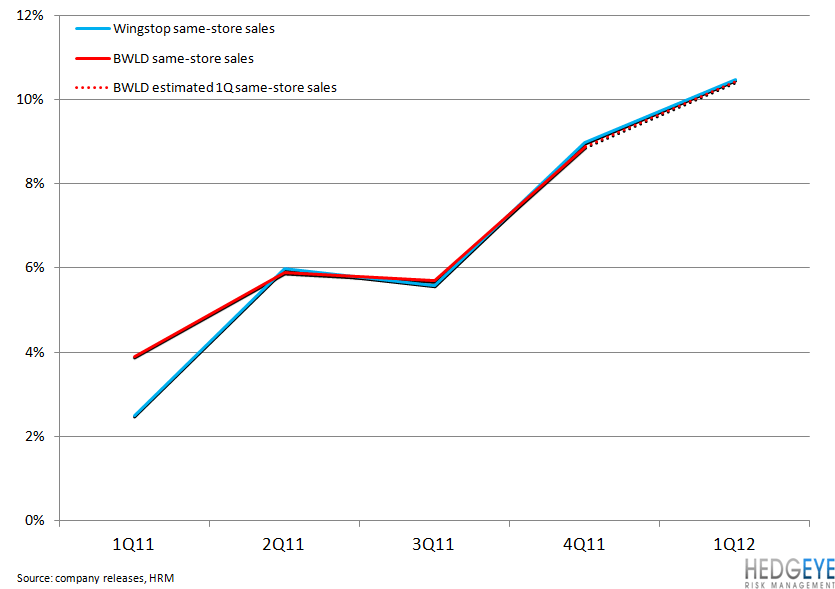

Buffalo Wild Wings is our favorite short in the casual dining space. The top line is what hurt us, and other investors and analysts with a bearish stance on the stock, when the company announced 4Q results earlier this year. The first six weeks of the year were strong for the company; same-restaurant sales came in at 12.9% and this data point overshadowed the fact that the fourth quarter of 2011 saw operating margins contract despite much higher than expected sales growth and benign commodity inflation.

At this point, investors know that the top line numbers for 1Q will be strong for Buffalo Wild Wings. Wingstop, a company that we believe offers a good proxy for Buffalo Wild Wings’ from a same-restaurant sales perspective, reported 1Q12 comps of 10.5%. If BWLD’s comps come in where we expect them to, also at 10.5%, that would imply a sequential slowing of comps through 1Q.

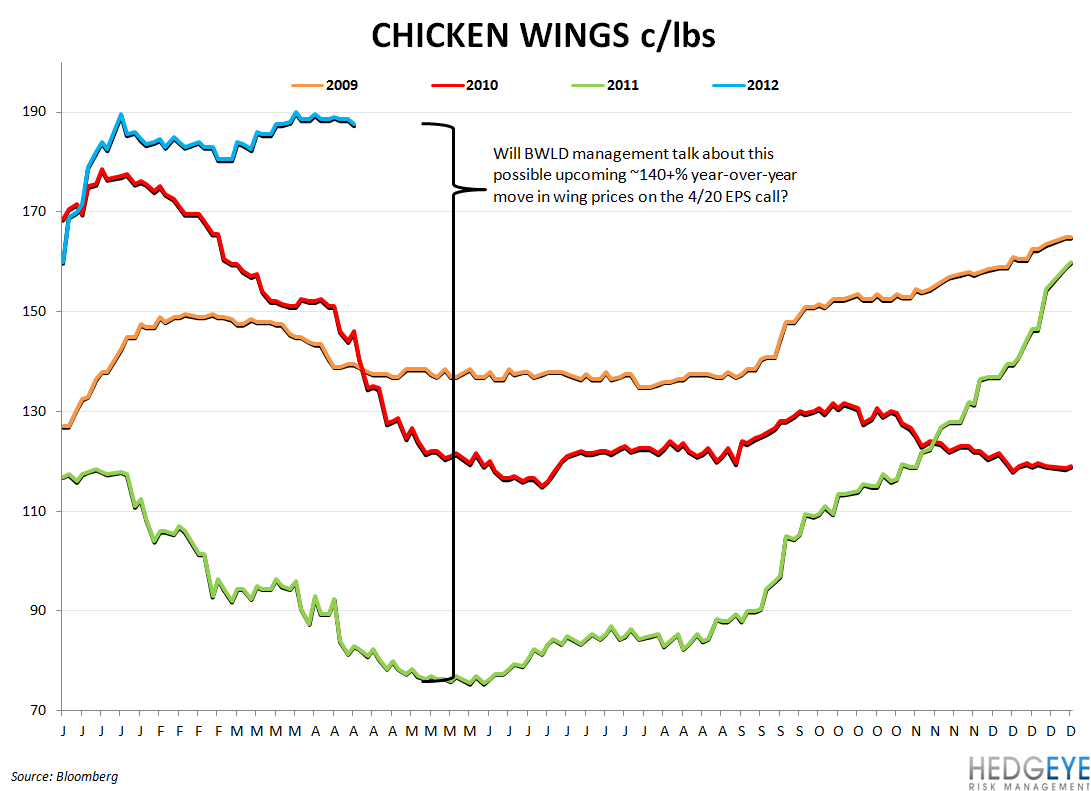

What will really move the stock, however, will be the forward-looking commentary that management provides. How much weather was in the 1Q comps? How much will traditional wing price inflation impact 2Q, 3Q, and FY12 EPS versus prior guidance? From the second chart, below, it seems that constrained chicken supplies could persist for some time. This risk-reward is highly skewed to the downside, here, in our view. From a price perspective, BWLD has outperformed the S&P 500 by almost 30% over the last three months. Additionally, the EV/EBITDA multiple that consensus is awarding the stock has increased by two turns. With the headwinds facing the industry and BWLD specifically, we believe that this stock could fall to $75 or lower.

Brinker

Brinker has been one of our favorite names in casual dining for the last eighteen months. As the chart below indicates, the employment picture is extremely important for the company. As we wrote earlier, our view on P.F. Chang’s is similar to that which we had on Brinker back in 2010. Now that the stock has ran up this high, the obvious question becomes whether or not it is time to take some money off the table. Depending on duration, we think it could be the right move.

Over the longer term TAIL, three years or less, we believe that this company is doing the right things to take share. The primary competitor of Chili’s is Applebees and that is a company that we believe is facing some top line headwinds over the next year in addition to any that may be facing the industry. Chili’s should continue to take share and reap the rewards of its upgraded kitchen and asset base.

Over the Trade and Trend durations, which are three weeks or less and three months or more, respectively, we have reservations about buying the stock at this price. Coming into the quarter, we are concerned that traffic may not be strong enough to indicate that the company is on track to meet FY12 comparable restaurant sales guidance. Following the company reporting 2QFY12 earnings, the stock sold off on concerns that top-line trends were suggesting that the company may not hit comparable restaurant sales targets for the full year. While the stock has more than recovered from those concerns, we believe that the recent industry trends are likely to revive investor anxiety as the next catalyst, 3QFY12 EPS on 4/27.

In terms of the Trend duration, there are two factors giving us pause. Firstly, the macroeconomic outlook has been softening. The improvement in initial claims data has reversed: claims are now rising. Secondly, we need to find evidence that Chili’s is seeing positive traffic as it laps the impact of the lunch combo introduced on January 10th, 2011. Weather may distort that picture, but we expect the Street to press management for comments on the 4QFY12 trends-to-date.

Macro has been a significant factor for Brinker’s strong performance. The correlation between claims and EAT has been 0.95 since the equity markets bottomed in October. Given our outlook on the macro environment, industry trends, and hesitance on the company’s traffic being positive at this point, we have change with the facts.

Howard Penney

Managing Director

Rory Green

Analyst