Conclusion: This should be one of the less eventful earnings seasons for the retail supply chain in quite some time. Expectations are in check, and management teams continue to have high hopes for a 2H margin ramp. They won’t back off of that pitch…until they have to later this year. The group is getting winded, with a 17x p/e on 23% consensus growth expectations, which is simply mind numbing. In this context, we like stories that have asymmetric factors that will allow them to work in any climate, such as LIZ, URBN, FINL, DECK, ANF, DKS NKE and RL. We don’t like names that will get stuck in the middle of the margin madness, such as KSS, JCP, HBI, GIL, CRI, M, TGT, SHLD and JNY.

Earnings Season for the Retail Supply Chain kicks off in earnest later this week with both Hanesbrands and UnderArmour showing their wares. We think that the broader take-away from this earnings season will be one of opacity and complacency – though it might not be fully apparent at the time. Companies have a great excuse in unfavorable winter weather, and little visibility into what the real underlying sales trends are in April due to the rather severe impact that the change in the holiday calendar is having on the top line. Specifically, Easter was on April 24thlast year, while this year it fell on the 8th. Given what we think is about a 3-week ramp of sales into the Easter holiday, the event definitely pulled sales forward into the month of March. As a result, companies who operate on a January – December fiscal calendar will recognize Easter spending in Q1 vs Q2 last year. We can argue anywhere from a 1% to 5% impact on sales results for March/April. The reality is that the companies are largely unaware of the actual magnitude of the shift either. But any kind of soft comps in April will probably be given a free pass by the market. In fact, we’d argue that it already has.

On top of the holiday calendar shift, the industry is at the tail end of a meaningful ramp in commodity costs that has the Street modeling a significant ramp in earnings growth in 2H12. That’s where we get concerned. People tend to forget that Gross Margins are not all about costs; there’s also a revenue/pricing component. Most retailers and suppliers are planning to keep lower commodity costs in 2H. But no few are banking on any peers breaking rank. JC Penney’s EDLP strategy will absolutely put Kohl’s on defense. That’s 12% of the apparel industry right there. What about Target, Sears, Amazon, Gap/Old Navy… The numbers start adding up. Margins are a zero sum game in this business. If prices come down, someone has to pay for it – either the brand, the manufacturer in Asia, the retailer, or the consumer. The only safe bet for us is that it probably won’t be the consumer.

To put some numbers behind the madness, consider the following…

a) The current consensus earnings growth forecast for the next 12-months is 23%. We have not seen this kind of growth since we came off of recessionary earnings numbers in 2010.

b) The market is giving this earnings growth a 17x p/e. We’ve only seen that kind of multiple five times in 3-years, but always at times when the group was still clearly under-earning. Who are we to say that it is NOT under-earning today? But to make this case, we need to see a considerable upshift in consumer spending alongside another decline in raw materials costs to push margins to new peaks. We don’t like that call.

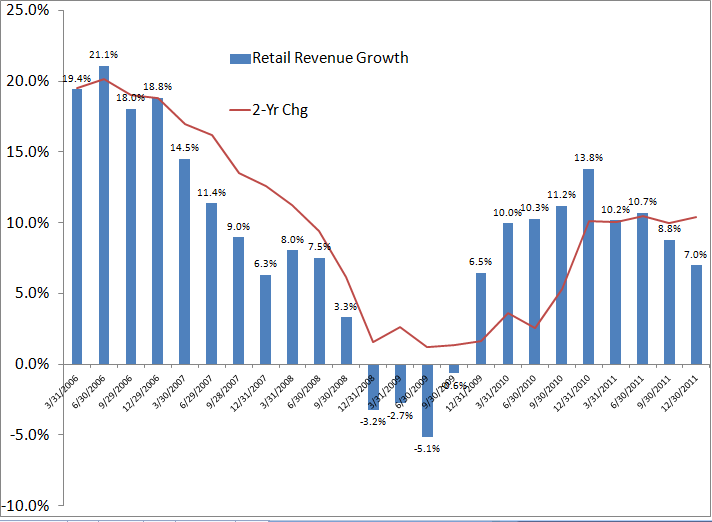

c) Revenue: 4Q was the first time in 3-years where revenue growth in retail was below 7%. Granted, it was on a tough comp vs the prior year, but the 2-year run rate has been stuck squarely at 10% for the past five quarters.

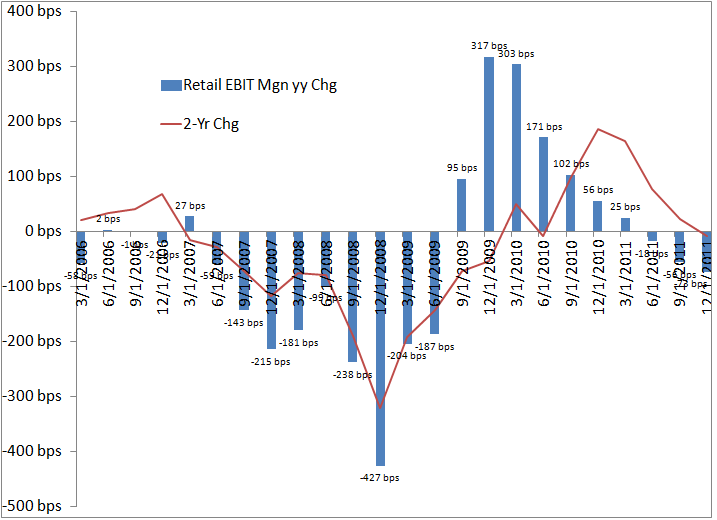

d) EBIT Margins have been down for the past three quarters by an average of about 50bps. The consensus is banking on a reversal in EBIT margins in 2H and in 2013. Such a sharp reversal would be the first time we’ve seen a non-recessionary rebound to that degree in well over five years.

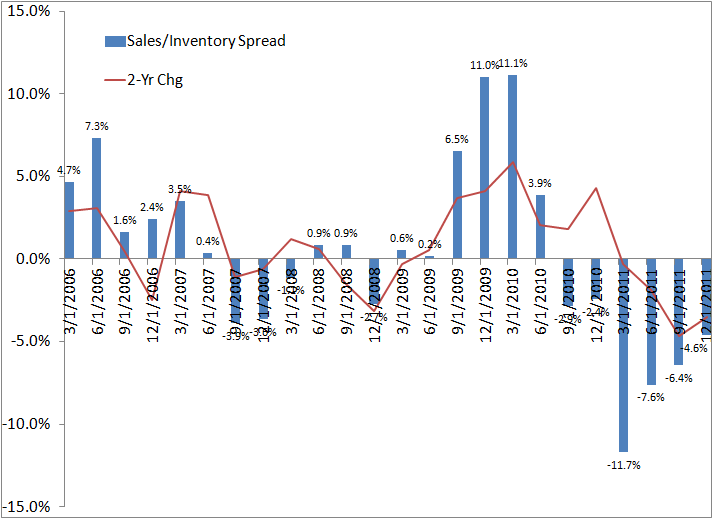

e) We’re going on six consecutive quarters where inventories are growing faster than sales. Maybe this supports the case for a sustained top line, but certainly not at the margin levels people are expecting in 2H.

f) Without question, capex is on the rise. That’s not bad by any means, so long as the returns are ultimately there. But the point is that the current run-rate of 3.4% of sales is likely to continue to creep closer to the 4% level – which crimps cash flow. Out of all these factors, this one concerns us least, as the space is largely sitting on too much cash anyway. That said, we think we’ll see an increasing bifurcation as to who can get a return on their investment and who can not.

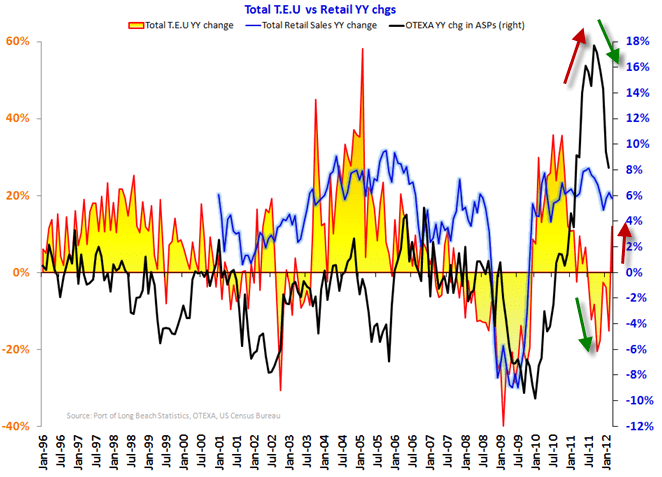

g) Here’s a notable callout. We all know that cost pressure is easing in 2H. But does everyone realize that we just saw container traffic pick up again after 10 months of being negative? Virtually 90% of the items we put on our bodies arrives into the US in a container. When costs are high, the industry pulled back order levels to keep margins in check. Now with costs planned to come down in 2H, we’re seeing retailers and suppliers get more aggressive with importing product. This plays into our concern about 2H Gross Margin risk.