We revisited the pricing disparity within HBI’s core basics category across 3 of its largest customers (WMT, KSS, JCP) which was prevalent in February. The pricing gap on like-for-like product remains what we’d call severe.

In our 2/13 note "HBI: Pricing Disparity = Uncertainty" we addressed the gap in Hanes’ basics pricing across various mid tier department stores and mass retailers. Additionally, we outlined our expectations for competition on price to heat up in 2H and as a result, while costs ease, pricing will buckle for HBI and offset the improvements on the cost side. In February, there was a prominent bifurcation in price points for like goods at KSS, WMT, AMZN & JCP. This gap is still in place today – down to the penny. Perhaps this is a positive for HBI that its customers are able to maintain such opacity. But we question how long the balloon can be held underwater.

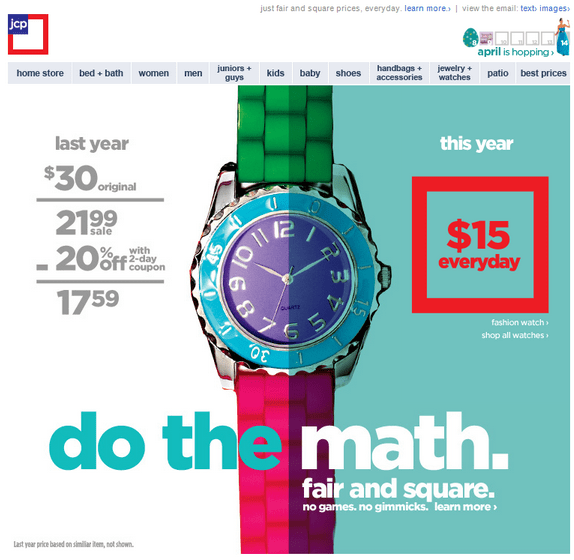

Our expectations for price competition to headline the back half of 2012 stem from industry dynamics, primarily JC Penny’s radical shift in pricing which will stir defensive responses from KSS, SHLD (if it still exists), M, TGT and Amazon. As of today, we have little transparency into what kind of traction JC Penney’s “Fair and Square” pricing strategy has gained on the consumer however we can say that from where we sit, Ron Johnson and team have started doing a better job conveying the strategy’s message. Previous ads have been replaced with the actual math (see below) – a watch that cost $30 last year, cost $21.99 when on sale (last year) and then $17.59 with an additional 20% off now costs $15…. everyday – clear as clear can be. Compare messaging from KSS vs. JCP. It’s like night and day.

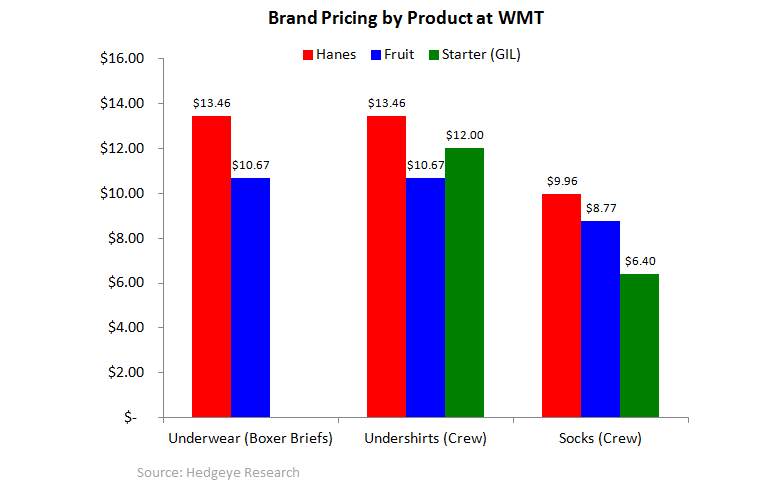

Right now (and unchanged from February’s check), for the same commodity Hanes 5 pack of crew T-Shirts, KSS pricing is 36% above JCP. Likewise, for an identical 4 pack of boxer briefs, KSS pricing is 44% above JCP. After adjusting for online BOGO and volume incentives, KSS remains 42% and 50% above JCP for the same two items respectively. The pricing disparity here doesn’t address Wal-Mart who actually has the best price for Hanes’ basics in undershirts, boxer briefs & socks (see chart 2 below). Interestingly though, at WMT, across the 3 basics categories, Hanes’ pricing is at a premium to Fruit of the Loom & Starter (GIL) for the items we analyzed (chart 1).

Near term, we expect the results tomorrow after the close to be in line with consensus (-$0.33), if not slightly better. The company has been on the road constantly over the past two months and has been extremely bullish about its prospects. It has all the visibility it needs this quarter. But as for visibility into 2H, the lock on revenue evaporates. Looking out to the intermediate term however and considering the implications a price battle could have for the commodity retailers like HBI, we’re shaking out at $1.54 vs $2.50E for F12. For additional takeaways following the 2/15 call, see our note "HBI: Fail".