“To succeed, you must study the end game before everything else.”

- José Raúl Capablanca (Chess Grandmaster)

José Raúl Capablanca was one of the world’s first great Chess champions. In fact, statistical ranking systems rank him the fifth greatest player of all time. He was a Cuban national and was world champion from 1921 – 1927. His nickname was the “Human Chess Machine” which characterized the simple nature of his style combined with his total mastery over the board. To him, understanding the end game was the preeminent focus for any player.

For those of you that aren’t Chess grandmasters, the end game is the point in the game when there are a relatively limited number of pieces on the board. Many chess analysts disagree as to when exactly the end game begins, but they all agree that when the end game begins strategy is much different than the middle game. In fact, over time the world’s best chess players have always excelled at the end game and utilized a consistent strategy.

Yesterday was one of those stock market days that certainly made a few investors wonder whether the global economic growth end game is actually here yet, or close. The snap back in U.S. equities didn’t necessarily surprise us but obviously characterized the almost bi-polar sentiment that currently exists in global equities. One day bad news matters, the next day good news matters more. The global economic growth slowing end game is here, then it isn’t.

Meanwhile in Spain over night we did get more evidence of the debt end game. The nation that will continue to be the pressure point in European sovereign debt issues this year, reported that non-performing bank loans accelerated from December and now total €143.82B, which is a 18-year high. This compares to a 1% level before the correction of the real estate market that began in 2008. As we’ve noted, the key risk is that this level of non-performing loans accelerates dramatically as property prices continue to revert to the mean.

The key issue with Spain accelerating to the downside from a debt perspective is that Germany is basically on record saying that Spain is too big to save. And so is Italy. Not being able to save either Italy or Spain is certainly a European sovereign debt end game that is increasingly concerning. To be fair, though, Spanish 10-year yields have come in again over night and are now solidly below the 6% line at 5.78%, which is a positive, but the IBEX this morning is down -3.2%. Tomorrow we get the longer term Spanish bond auctions and they, too, will likely be as successful as any artificially controlled market.

The major political catalyst this week in Europe is the French elections with the first round this weekend. Since a major candidate has to garner 50% to win, it is likely there is a second round given there are major candidates competing. Currently, the most recent polls from CSA have Hollande leading Sarkozy 29% to 24% in Round 1. This is an improvement from being tied a few days ago. The polls then show Hollande mercy crushing Sarkozy in Round 2, by a margin of 58% to 42%.

The French election is critical because: A) Hollande is a Socialist, B) Hollande is a Socialist, and C) Hollande has stated that if elected he will renegotiate the EU budget compact and that he will not accept austerity as rule for countries. Things are about to get a lot more challenging politically in the great monetary union that is the Eurozone.

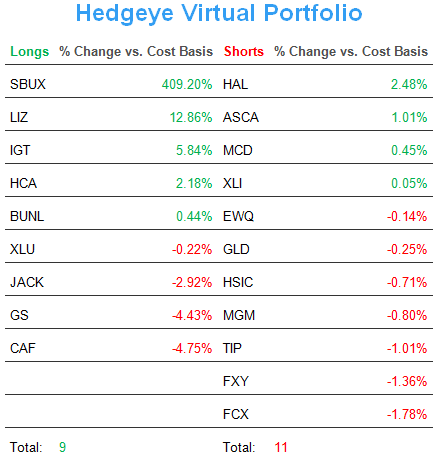

In the U.S. we are fully in the midst of earnings season. As part of earnings season, we our having our Sector Heads participate in our morning calls for clients ( ping sales@hedgeye.com if you don’t have access ) and also write a brief summary of their thoughts on earnings in their sectors. Our Financials Sector Head wrote this yesterday as it related to financials:

“Roughly one third of financial companies have reported earnings so far. 7 of the 8 large or mid cap companies have beaten estimates on the bottom line. Revenue trends have been more mixed, with just over 1/3 beating estimates, 1/3 in-line and just under 1/3 missing. However, this is a bit misleading because of Debt Value Adjustment. With DVA, the big banks’ revenue lines are adversely affected by an accounting convention that requires them to recognize negative revenues when their credit default swaps tighten. First quarter saw sizeable CDS tightening, so the headwind was significant for all the large-cap capital markets sensitive names: C, JPM, BAC, GS, MS.”

The remainder of his note can be found at www.hedgeye.com in unlocked content and we will be updating these summaries over the course of the next week. But if there was one take away from Josh, it is that so far his companies are beating estimates, which is a positive driver for stock prices in the financial sector in the short term.

Related to U.S. growth, we have a number of negative catalysts that will come more and more into focus in the coming months. Namely, as of January 1st, 2013, the Bush tax cuts, the temporary payroll tax cut, and the long-term unemployment benefits all expire. Then on January 15th, 2013 the automotive government spending cuts, driven by the failure of the Joint Select Committee on Deficit Reduction, go into effect. Will it be check mate for U.S. economic growth? Probably not, but Q1 2013 is certainly an end game to start contemplating.

The immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, Japanese Yen (vs USD), Euro/USD, and the SP500 are now $1, $117.69-120.93, $79.26-79.64, $79.96-82.30, $1.30-1.32, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research