This note was originally published at 8am on April 04, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Early triumph can promote future failure.”

-Nassir Ghaemi

Last week I wrote a pointed Early Look note titled Bernanke’s War. When my Global Macro Process sees Growth Slowing like this (like it did in Q1 of 2008, Q1 of 2010, and Q1 of 2011), I am not shy making a call that’s counter to consensus. We have fought the Fed before, and won.

Fighting The Fed’s conflicted and compromised 0% Policy To Inflate means that, at some point, the man runs out of either political room or the ability to ban Global Macro-economic gravity. If either or both happen, I think I can win.

Bernanke’s Bubbles are vast. That’s why I have a 0% allocation in the Hedgeye Asset Allocation Model to both Commodities and Fixed Income right now. If these bubbles are in the process of popping, why stay in them?

Back to the Global Macro Grind…

Dollar up = Correlation Risk On, eh. All it took yesterday was the US Dollar Index arresting its most recent 4 consecutive-week debauchery for US stocks to stop going up. At one point in the day, the SP500 was down almost 1%. That’s only happened 1 other time in 2012 (no, that’s not normal).

Another way to say what happened yesterday, and what’s happening across asset classes in Global Macro this morning for that matter, is what we have coined Deflating The Inflation. Functionally, whether Romney or Obama figures this out or not is left to be seen, but popping Bernanke’s Bubbles at the pump would be most easily achieved by raising interest rates.

What other long-term bubbles are popping this morning?

1. GOLD (we’re short GLD): down another -2.4% this morning to $1632/oz and finally snapping my long-term TAIL support line of $1652. Over the longest of long terms, no matter what your religion on the subject matter of Gold, it does not act well when Treasury Yields are rising. People look at “risk free” rates of return relative to absolutes; particularly when 0% was the absolute comparison.

2. US TREASURIES (we’re short TIP): Treasuries are down with 10yr bond yields rising to 2.25%, taking the rip in 10yr yields to +22% from 1.84% (immediately after Bernanke tried his best to ban economic gravity during his January 25th speech, pushing easy money to 2014, sort of).

3. JAPANESE YEN (we’re short FXY): yes, during a Currency War where the Americans, Europeans, and Japanese are in a race to the bottom to de-value their respective fiat currencies, the US and European Keynesian Policy Makers perpetuated a bubble in the Japanese Yen up until February of 2012. Then kaboom – Yen down -9% in a straight line as the Euro and USD stopped going down.

The popping is a process, not a point. Unless you think that there is political inertia, from here (i.e. throughout the US Election), that allows Bernanke to keep this 0% Policy To Inflate ball under water, you won’t have to take my word for it on hearing the popping.

“Pop, pop, bang!”

Remember that line from Cinderella Man’s Jimmy Braddock (played by Russell Crowe in 2005)? That was one of the many metaphors I used when Fighting The Fed during Q1 of 2008. Braddock was an Irish-American boxer from New Jersey. I am a Canadian-American Fed fighter from Connecticut. And, Mr. Bernanke, I am not going away.

Back to the ring. I have a 73% position in Cash and am in no hurry to add to my 9% asset allocation to US Equities this morning. Why? Well, because US Equities are bubbly too. Not as bubbled up as Bonds and Gold were, but they’re certainly worthy of wearing a bobble head.

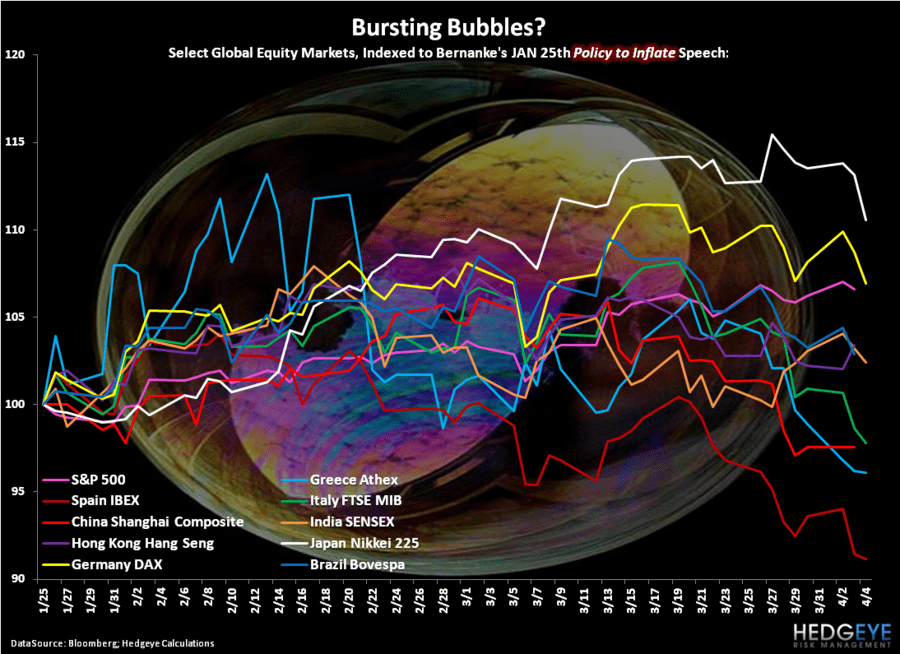

The most interesting thing about Equities, globally, is that with the exception of the USA and Venezuela (ran by 2 serial currency debauchers in Chief who think stock market inflations reflect economic prosperity), equity markets around the world stopped going up a month ago. Check out the corrections in markets that have stopped making higher YTD highs:

- Greece = down -15.2%

- Spain = down -12.4%

- Italy = down -9.5%

- China = down -8.0%

- Brazil = down -6.0%

- India = down -5.1%

- Japan = down -4.2%

- Germany = down -4.1%

- Hong Kong = down -4.1%

- USA = down -0.4%

The most obvious point here is that the SP500 is only down -0.4% from its YTD peak. It has only had 1 down-day greater than 0.7% in 2012, and is now subject to the only risk management strategy that has held true for the last 40 years – mean reversion.

It’s a good thing we have Apple. Or is it?

Maybe that’s a bubble too. Who knows until it starts popping. But the storytelling about this stock is hilarious. Next to a story that “Home Prices Seen Dropping 10%”, the 2ndMost Read story on Bloomberg is titled “Apple Fever, $1 Trillion Valuation.” Nice.

The thing about bubbles (centrally planned ones and all others) is that they need a darn good story. Apple’s is fantabulous at this point, and so was that of The Ben Bernank.

That said, don’t forget where I started this morning – if that quote from Nassir Ghaemi’s “A First-Rate Madness” comes home to roost, the “early triumphs” of Keynesian Economics could very well lead to Bernanke losing this war.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, Japanese Yen, and the SP500 are now $1632-1666, $121.98-126.12, $79.19-79.64, 81.91-83.78, and 1388-1419, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer