“I am not well qualified to criticize the theory of rational expectations and the efficient market hypothesis because as a market participant I considered them so unrealistic that I never bothered to study them.”

-George Soros

Just as Keith has his pile of reading, I also have mine. The quote above from George Soros was in a speech he gave to the Institute for New Economic Thinking Annual Plenary Conference. The quote itself was buried somewhat deep in Soros’ comments, but it jumped off the page at me. To me it is somewhat akin, and I hate to use another hockey analogy, to Wayne Gretzky being told he couldn’t score 90+ goals in a NHL season (which is more than one goal per game) after he did it.

Soros, of course, is in a similar situation in the realm of investing. He has absolutely crushed it in terms of outperforming the market over long periods of time. His performance has been so staggering, in fact, that his net worth today is estimated north of $22 billion. Now I haven’t always admired Soros’ political positions, but it is very difficult not to admire his investment track record.

More importantly, I’ve always admired his desire and interest in attempting to explain his investment process. Much of what Soros has written about his investment process revolves around reflexivity. He loosely based this way of interpreting the markets on a theory by philosopher Karl Popper that suggests that the individual’s interpretation of reality never quite correspond with reality itself.

According to Soros, in financial markets this is taken one step further in that individuals with a flawed sense of reality actually take action based on this flawed interpretation of the future. In turn, these collective actions often influence future events, or more likely, as Soros said, create a “divergence between the participants’ view of reality and the actual state of affairs and a divergence between the participants’ expectations and the actual outcome.”

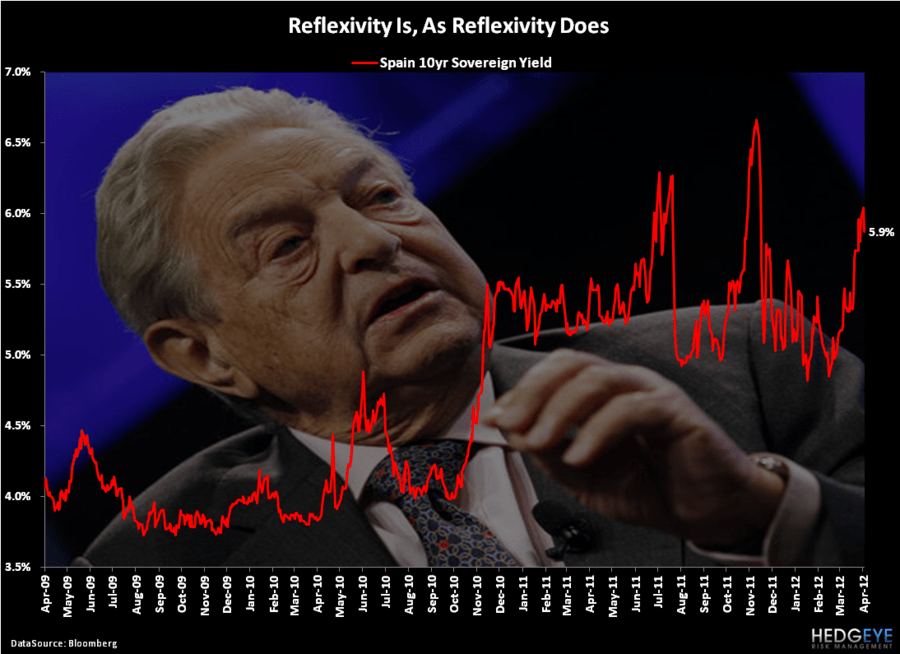

From my seat, the pin action in Europe over the past 18-months highlights Soros’ idea that collectively market participants really have no idea what the ultimate outcome in Europe will be to resolve the intrinsic issues associate with the Maastricht Treaty. Specifically, I’m referring to the issue that a European monetary union cannot exist sustainably without a strong political union or fiscal solidarity.

This morning the first of two key Spanish debt auctions occurred for the week. The reflexive response from the equity markets is that the auction was a success, as European equities are up across the board with beleaguered French banks leading the way. According to reports we are receiving from some of our contacts on the ground in Europe, the Spaniards sold 3.2 billion euros of 12 – 18 month bills versus a maximum target of 3.0 billion euros at a total bid-to-cover of 3.19. On the negative side, the bills sold yielded 2.6% on the 12-year versus 1.4% prior and 3.1% on the 18-year versus 1.7% prior. So, yes the auction was “successful”, albeit at usury type rates.

It’s quite possible that the Spanish debt auction this Thursday is just as “successful”. Although as always, I would recommend watching not necessarily what the government officials say, but what they actually do. In that vein, this week European officials are headed to Washington, DC with hat in hand to ask for more money from the International Monetary Fund. The IMF meetings occur from April 20 – 22nd. Interestingly, the Europeans may meet at least one surprising fiscal hawk in the way of U.S. Treasury Secretary who has already ruled out additional contributions to the IMF based on the belief that the IMF already has “substantial financial resources.”

Meanwhile as the loose monetary policies in Europe appear likely to be extended in perpetuity, inflation readings came in stickier, even if marginally, across the board this morning. Eurozone March CPI came in at +1.3% month-over-month and +2.7% on year-over-year basis, both ahead of expectations. The acceleration in U.K. inflation was even more noteworthy coming in at +3.5% versus estimates of +3.4%.

The scary thing with inflation is that, just like George Soros’ returns, it also compounds. So, at this rate of inflation, in 10 years someone in the U.K. who makes $50,000 now will have to make $70,000 to have the same purchasing power. Thus we have the hidden tax of inflation.

Switching gears briefly, I wanted to touch on U.S. politics. Yesterday the Senate blocked the so-called Buffett Tax, which would have implemented a mandatory tax of 30% on anyone earning over $1 million in income. The legislation was blocked basically on party lines. In terms of true tax reform, the Buffett tax is basically meaningless and is clearly not much more than a political stunt, although perhaps an adroit one by the Obama camp as according to a recent Gallup poll 6 in 10 eligible voters supported passage of the bill.

The Democrats are only going to continue to focus on this class warfare type issue heading into the Presidential elections this fall. In fact, yesterday I received a blast email from Stephanie Cutter, the Deputy Campaign Manager for Obama which invited me to compare my tax rate to Romney’s. Ultimately, this “war on the rich” is and will continue to backfire on Obama in one key way: political donations. So far, corporate executives across almost every industry have been giving less money to Obama and the Democrats this election cycle. (We will have a note on this up today.)

For those looking for some interesting and enlightening reading this morning, the IMF releases the world economic outlook and fiscal monitor at 9am and ECB President Draghi is delivering an intro speech at the 6thECB Statistics conference. Thinking about an annual ECB statistics conference reminds of Mark Twain’s famous quote (who he purportedly borrowed from former U.K. Prime Minister Benjamin Disraeli):

"There are three kinds of lies: lies, damned lies, and statistics."

Indeed.

The immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, Japanese Yen (vs USD), Euro/USD, and the SP500 are now $1, $117.67-121.61, $79.27-79.67, $80.03-82.34, $1.30-1.32, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research