TODAY’S S&P 500 SET-UP – April 17, 2012

As we look at today’s set up for the S&P 500, the range is 34 points or -1.50% downside to 1349 and 0.98% upside to 1383.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 4/16 NYSE 411

- Up from the prior day’s trading of -1577

- VOLUME: on 4/16 NYSE 735.51

- Decrease versus prior day’s trading of -4.60%

- VIX: as of 4/16 was at 19.55

- Unchanged versus most recent day’s trading

- Year-to-date decrease of -16.45%

- SPX PUT/CALL RATIO: as of 04/16 closed at 2.15

- Increase from the day prior at 1.98

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 39

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 2.01

- Up from prior day’s trading of 1.98

- YIELD CURVE: as of this morning 1.73

- Increase from prior day’s trading at 1.71

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: ECB President Mario Draghi delivers introductory speech at the Sixth ECB Statistics Conference

- 8:30am: Housing Starts, March, est. up 1% M/m to 705k (prior 698k)

- 8:30am: Building Permits, March, est. 710k (prior revised 715k)

- 9am: Bank of Canada interest rates

- 9:15am: Industrial Production, March, est. 0.3% (prior 0.0%)

- 9:15am: Capacity Util., March, est. 78.5% (prior revised 78.4%)

- 11:30am: Treasury selling $30b 4-week bills

GOVERNMENT:

- IMF, World Bank holds first day of annual spring meetings

- IMF releases World Economic Outlook and Fiscal Monitor, 9am

- CFTC Dodd-Frank rules for swap dealers take effect

- Deadline for EPA to release rules for air pollution from oil, gas drilling, primarily affecting fracking

- Secretary of State Hillary Clinton attends U.S.-Brazil Global Partnership dialogue in Brasilia

- Arizona primary for Gabrielle Giffords’s Congressional seat

- House, Senate in session:

- House Transportation subcommittee holds hearing on GSA waste of taxpayers’ money, 8:30am

- Senate Banking Committee holds hearing on Export-Import Bank reauthorization, 10am

- House Ways and Means Committee holds hearing on tax incentives for retirement accounts, 10am

- House Energy subcommittee marks up Gasoline Regulation Act and Strategic Energy Production Act

- House Oversight subcommittee holds hearing on the Securities and Exchange Commission and cost-benefit analysis, 10am

- Senate Homeland Security Committee subcommittee holds hearing on Contingency Contracting Reform Act of 2012, 10:30am

WHAT TO WATCH:

- Goldman Sachs releases 1Q results; watch trading, investing rev.

- Spain pledged to take “decisive” action against Argentina within days, after Argentinian President seized YPF, the oil company majority-owned by Repsol

- Home starts may have increased 1.0% to a 705k annual rate in March, economists est., as housing demand stabilized

- RIM said to be in talks to hire financial adviser to help weigh strategic options

- Toshiba agrees to buy IBM’s point-of-sale terminal business for $850m

- Japan said it will provide $60b to IMF’s effort to expand its resources

- Audi said poised to purchase motorcycle-maker Ducati for $1.1b

- Citigroup hosts annual meeting

- Zynga plans to step up pace of acquisitions in search for new ‘FarmVille’

- Rio Tinto 1Q mined copper output misses analyst ests.

- Fiat, Renault and Peugeot Citroen lead European car sales to 14-year low as economy stalls

- Zayo/AboveNet go-shop ends today

EARNINGS:

- Comerica (CMA) 6:40 a.m., $0.56

- US Bancorp (USB) 6:45 a.m., $0.64

- Omnicom Group (OMC) 7 a.m., $0.69

- State Street (STT) 7:06 a.m., $0.87

- Northern Trust (NTRS) 7:14 a.m., $0.65

- TD Ameritrade Holding (AMTD) 7:30 a.m., $0.26

- Coca-Cola (KO) 7:30 a.m., $0.87

- Johnson & Johnson (JNJ) 7:45 a.m., $1.36

- Forest Laboratories (FRX) 8 a.m., $0.70

- Goldman Sachs (GS) 8 a.m., $3.55

- WW Grainger (GWW) 8 a.m., $2.52

- McMoRan Exploration Co (MMR) 8 a.m., $(0.12)

- USG (USG) 8:29 a.m., $(0.42)

- Cree (CREE) 4 p.m., $0.21

- Stryker (SYK) 4 p.m., $0.99

- CSX (CSX) 4:01 p.m., $0.38

- Seagate Technology (STX) 4:01 p.m., $2.12

- International Business Machines (IBM) 4:03 p.m., $2.66

- Intel (INTC) 4:05 p.m., $0.51

- Intuitive Surgical (ISRG) 4:05 p.m., $3.12

- Yahoo! (YHOO) 4:05 p.m., $0.18

- United Rentals (URI) 4:15 p.m., $0.05

- Webster Financial (WBS) 4:15 p.m., $0.40

- Cathay General Bancorp (CATY) 4:30 p.m., $0.30

- Fulton Financial (FULT) 4:30 p.m., $0.19

- East West Bancorp (EWBC) 4:45 p.m., $0.43

- Linear Technology (LLTC) 5 p.m., $0.42

- Packaging of America (PKG) 5 p.m., $0.40

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – we continue to see Bernanke’s Bubbles in commodities popping. On the commodities bounce this morning, Copper is down again and remains in a bearish formation alongside 10yr UST yields < 2.03% at 1.99% last.

- Drought Draining Stocks of Oils Amid Record Demand: Commodities

- Oil Rises to Two-Day High on Spain Debt Auction, Retail Sales

- March Gold Sales Drop as Stability Returns, Perth Mint Says

- China May Become Top Corn Importer by 2014, Displacing Japan

- Soybeans Rise on Signs of Increasing Chinese Demand; Wheat Gains

- Gold May Gain in London as Euro-Area Debt Crisis Spurs Demand

- Copper Pares Declines in London, Gains 0.3% to $8,004 a Ton

- Shanghai Futures Exchange Announces Silver Contract Draft Plan

- Rubber in Tokyo Drops as Slower Growth in China Weakens Demand

- Rio Tinto First-Quarter Iron Ore Output Misses Estimates

- U.K. Reliance on Norwegian Gas Boosts Volatility: Energy Markets

- Ghana Signs $1 Billion Loan With China for Natural Gas Project

- Freeport Takeover Talk Intensifies With Low Valuation: Real M&A

- Drought Pushes Edible Oils Demand Higher

- Soybean Imports by China Seen Topping USDA Estimate on Crush

- LME Studying Including Chinese Yuan for Settlement, Clearing

- Palm Oil May Advance as Rainfall in Malaysia Disrupts Harvests

CURRENCIES

EUROPEAN MARKETS

SPAIN – you learn the most about bear markets on the bounces – this morning’s in Spanish Equities on no-volume tells you all you need to know as people keep focusing on last year’s game (bond auction yields); it’s now all about the economic gravity of the situation and the IBEX needs to close > 7585 to recapture its 1st line of support. France and Italy don’t look much better.

ASIAN MARKETS

JAPAN – the Nikkei was down for the 9th of the last 10 trading sessions last night, taking its correction from the March YTD top to -7.7%; Asian equities were generally weak with the exception of India who reverted to the broken playbook, cutting rates.

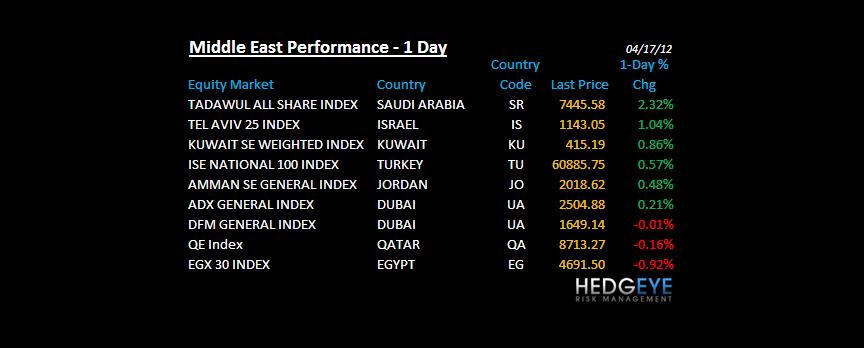

MIDDLE EAST

The Hedgeye Macro Team