Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

Key Takeaways:

* Spanish sovereign swaps continue to climb. At 502 bps this morning, they are up 102 bps from a month earlier and are up 38 bps vs. the prior week. Italian swaps stand at 435 bps, up 17 bps week over week and up 80 bps vs. a month earlier. For reference, Spanish swaps just hit an all time high as of this morning, narrowly eclipsing their highs of November last year (497 bps). Italian swaps are still a good bit below their prior highs.

* Both American and European Bank CDS were wider WoW. Bank swaps are reflecting the deterioration in creditworthiness in Spain, an economy roughly 5x as large as that of Greece. Get ready for 2011 all over again as we watch Spanish swaps climb and climb and concerns surrounding that rise escalate.

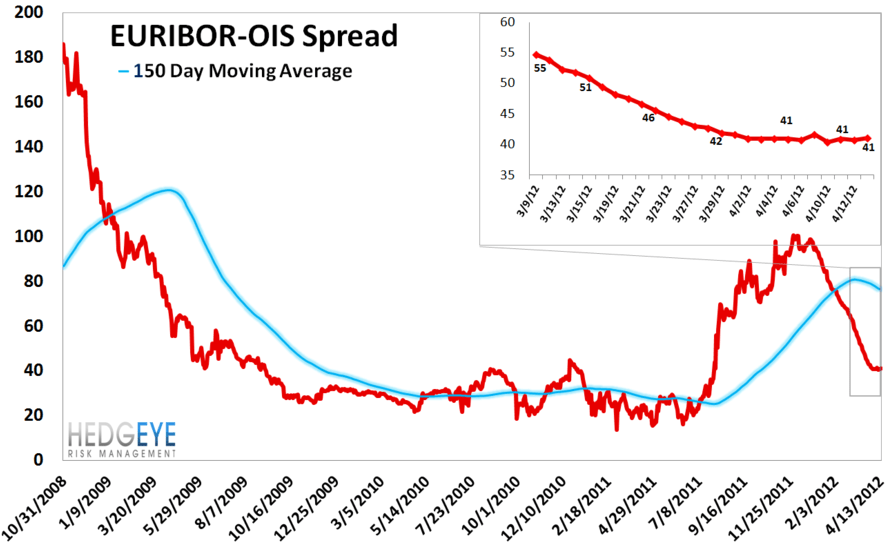

* Euribor-OIS has ceased tightening. After steadily falling since the start of the year, the risk measure has essentially flattened out at the 40-41 bps level. This had been a key measure we were using to gauge the perceived risk in the counterparty system.

* High yield rates rose 4 bps last week underscoring increasing risk in the market.

-------------

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was flat ending the week at 41 bps.

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis. Banks deposited €742.8 billion in the latest reading.

European Financials CDS Monitor – Bank swaps were wider in Europe last week for 37 of the 40 reference entities. The average widening was 5.6% and the median widening was 4.8%.

Security Market Program – For a fifth straight week the ECB's secondary sovereign bond purchasing program, the Securities Market Program (SMP), purchased no sovereign paper for the latest week ended 4/13, to take the total program to €214 Billion.

February-to-date the Bank has purchased a mere €210 Million versus €2.2 BILLION in the week ended 1/20 and €3.8 BILLION in the week 1/12.

The standstill comes as market risk returns. While there are other channels to suck up sovereign bond issuance, including through funding from the two 36-month LTRO programs, the SMP’s lack of buying may send a negative signal to market participants that are already weary of the sovereign and bank risks bubbling in Spain.

Matthew Hedrick

Senior Analyst