“My mother said to me, 'If you are a soldier, you will become a general. If you are a monk, you will become the Pope.' Instead, I was a painter, and became Picasso.”

-Pablo Picasso

The Spanish painter Pablo Picasso had no shortage of belief in his intrinsic talent as a painter. His point in the quote above was to basically say that if you are going to do something well, you should endeavor to do it better than anyone. Something his nation is not currently doing well, let alone better than any other nation, is managing their sovereign debt load.

As we wake up this morning to another week of managing risk in the global macro markets, Spain, as we highlighted in a detailed note last week, is once again front and center. The leading indicator of an acceleration of sovereign debt woes in Europe is the Euro, which has dropped just below $1.30 versus the U.S. dollar for the first time in two months.

The Euro is moving in anticipation that there are a series of Spanish debt auctions this week that may not go quite as planned. Specifically, tomorrow Spain will sell 12 and 18-month notes. This will be followed on Thursday by longer term debt due in October 2014 and January 2022. Watching these auctions will be critical in determining whether the European Union has the wherewithal to contain the once again accelerating crisis in confidence in the European sovereign debt markets.

To that point, if the debt and CDS markets for Spain are any indication, the Spanish sovereign debt issues are far from contained. Spanish 10-year yields are now at 6.16% and at levels not seen since December 2010. Meanwhile, Spanish credit default swaps are, literally, at all-time highs.

As we’ve previously written, Spain is a bigger concern than Greece for many reasons, but most specifically because its economy is almost 5x that of its Hellenic neighbor and is the 12th largest economy in the world. Clearly, Spain is not an insignificant player on the world stage.

To be fair, Spain’s sovereign debt load is not elevated to a level that would suggest as much stress as we are currently seeing in its debt markets. In fact, according to Euro Stat, Spain’s federal debt balance as a percentage of GDP was only 69% at the end of 2011. Many sovereign analysts believe the number is a bit of a misnomer though and when regional debts are included, which are in effect a recourse to the federal government, the total amount of debt is closer to 90%.

Regardless, the more pertinent issue in Spain is the acceleration of debt. By Spain’s own projections, the nation will add more than 10% to its debt-to-GDP ratio this year, taking that ratio closer to 80% on Euro Stat’s numbers. This will lead the industrialized world in growth in debt-to-GDP.

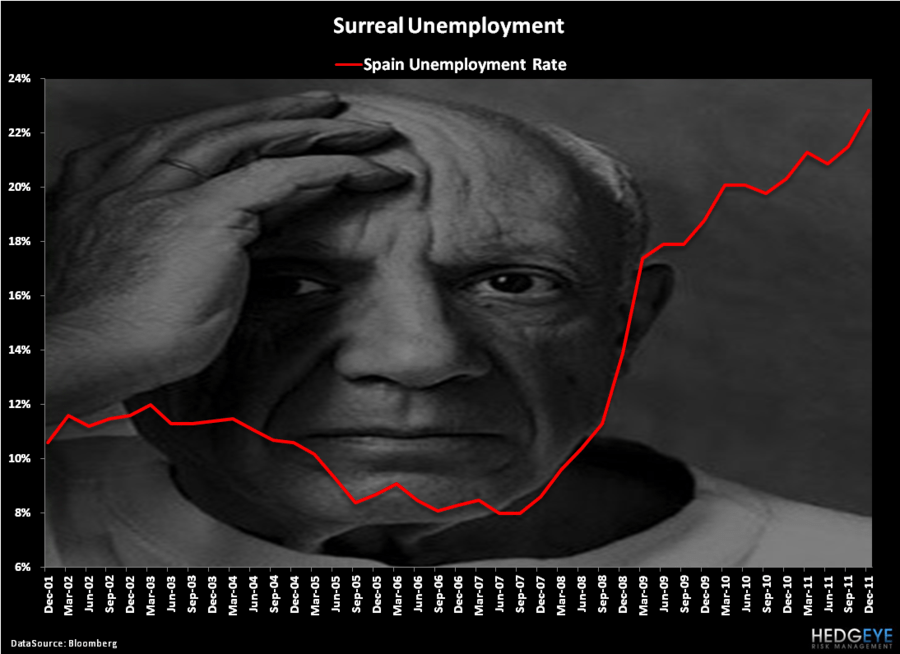

Spanish unemployment hit 23.6% at the end of February and the unemployment rate for the youngest demographic in Spain is literally at 50%. Given the structural unemployment issue, Spain is literally unable to grow out of its debt issues. This lack of growth potential is clearly what the markets are starting to bake in to Spanish yields. That is, if there is a way out, it is not going to be easy and certainly won’t occur before the nation becomes substantially more indebted.

This weekend Paul Krugman of the New York Times, in typical fashion, suggested adding more Keynesian stimulus to the mix. Or, at the very least, Krugman suggests dispensing with the “insane” austerity. If the United States is any case study, accelerating government spending does not appear to be the path to sustained economic prosperity.

Krugman may actually get his way in France, where Socialist Francoise Hollande is extending his lead over Nicolas Sarkozy. Currently, Hollande is expecting to win both the first round (April 22nd) and the second round (May 6th) of French elections. Sadly, we actually know how Socialism ends as well.

The other rumor out of Europe this morning is that Spain may re-instate a short selling ban. That is a little counter intuitive to us. Even if the markets are not giving you much in the way of confidence votes, changing the rules mid game is not going to increase confidence.

In other global macro news this morning, we are also seeing increased evidence of growth slowing and inflation accelerating. On the growth front, Sweden cut its 2012 growth outlook from +1.3% to +0.4% and the Bank of Korea cut its 2012 growth forecast from +3.7% to +3.5%. Meanwhile, inflationary data from India continued to come in hot as wholesale prices “beat” consensus estimates coming in at +6.9% versus the +6.7% estimate.

Switching gears, and while we wouldn’t normally flag Barron’s as a leading indicator for tail risk, the weekly publication did do a nice job this weekend discussing the next impending debt disaster in the United States, student loans. In terms of scale, the almost $1 trillion in outstanding student debt is larger than both the auto loan market and credit card market. The most interesting statistic quoted in the article is that college tuition is up 300% since 1990, which far outstrips the increase in more traditional measures of inflation by a factor of 4x.

At the end of the day, though, the vast majority of the student debt is guaranteed by the federal government, so on some level it has much more security than the typical sub-prime mortgage. Just make sure you add the $1 trillion asterisk when calculating the debt-to-GDP of the United States. Fiscal Picassos, we are not.

The immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, Japanese Yen (vs USD), Euro/USD, and the SP500 are now $1, $118.63-122.36, $79.64-80.27, $80.12-82.34, $1.29-1.31, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research