European Positions Update: Short France (EWQ); Long German Bunds (BUNL); Sold Germany (EWG) on 4/12

Asset Class Performance:

- Equities: The STOXX Europe 600 finished down -2.2% week-over-week vs -1.6% last week. Bottom performers: Italy -5.8%; Spain -5.4%; Finland -4.9%; Hungary -4.6%; France -3.8%; Denmark -3.0%. Top performers: Cyprus +2.8%; Greece +0.8%; Russia (MICEX) +0.6%.

- FX: The EUR/USD is down -0.18% week-over-week. W/W Divergences: PLN/EUR -0.54%, SEK/EUR -0.39%, HUF/EUR -0.28%

- Fixed Income: Greek 10YR bond yields fell -107bps week-over-week, versus a gain of similar magnitude last week. Most other countries were relatively flat week-over-week. Portugal led the charge +32bps to 12.55%, followed by Spain (+8bps) to 5.88%. Italy fell -7bps to 5.42%.

Portfolio: Short France (EWQ); Long German Bunds (BUNL)

Keith shorted France (EWQ) and bought German Bunds (BUNL) in the Hedgeye Virtual Portfolio yesterday (4/12). The moves are a continuation of our thinking about Europe: there’s a relative advantage to playing the capital markets of the stronger countries on the long side and weaker countries on the short side, at a price. We’re highly sensitive to price and well aware that there’s no simple equation to pair or hedge risk in Europe: political headline risk, even from the tiniest of countries in Europe, can roll country equity indices and influence yields across the continent. And we don’t expect this trend to change. Namely, we expect Eurocrats to continue to behave in a reactive manner, with the next call likely being the re-engagement of the SMP, which has been dormant for the last four weeks. This program may help to reduce the recent spike in sovereign yields and rise in CDS, yet does little to address the larger box the Eurozone is trapped in. That said, we’ve yet to see a disruption in the tight trading band of the EUR/USD of $1.30 - $1.34. We recommend trading the range, until further notice.

The timing of our short France position also plays into Sunday’s first of two French presidential election votes and increased fear around the sovereign and banking risk of Spain. The incumbent Nicolas Sarkozy is favored to win the first vote versus Socialist candidate Francois Hollande; however Hollande is expected to win the deciding second vote 53% to 47% according to an Ifop-Fiducial poll published on April 6th. What’s broadly clear is that both candidates plan to increase taxes and impose fees on financial transactions. Both have declared to reduce the country’s deficit to 0% (as a % of GDP), Hollande by 2017 and Sarkozy by 2016. Both guide to reduce the deficit to 3% by 2013 versus 5.3% in 2011.

However, Hollande has signaled an even more socialist agenda, which we think should result in the inability of the state to meet its deficit and debt reduction targets. Hollande wants to increase spending by €20 MM over five years (by repealing €29 MM of tax breaks and generating revenue by separating retail and investment bank operations and raising the income tax on earners over €1 MM to 75%) and reduce the retirement age to 60 from 62. With the country’s debt rising to the 90% level, we expect growth to be compressed, as proven by the work of Reinhart and Rogoff.

Simply put, the CAC has run well ahead of peer indices and has room to revert. The CAC is at 0.9% year-to-date, while the Spanish IBEX is down -15.4% YTD.

With respect to our position on German Bunds, we bought BUNL on a pullback, and continue to like Germany's employment and fiscal situation, which is much more tolerable than America’s right now and most of the Eurozone. Germany, across the capital markets, continues to signal a relatively safer bet.

Call Outs:

SMP - European Central Bank Executive Board member Benoit Coeure suggested that the bank could revive its bond-purchase program to reduce Spain’s borrowing costs: “We have an instrument, the securities markets program, which hasn’t been used recently but it still exists.”

Spain - borrowed €227.6B from the ECB in March, up €75B versus February, the same amount Italy borrowed in March.

Portugal - Dependence of the Portuguese banking system on the ECB rose to a record high in March, as banks took advantage of easier borrowing conditions: Bank of Portugal said domestic banks' use of the ECB's various credit facilities rose to €56.32 billion in March from €47.55 billion in February.

Switzerland - “The Swiss National Bank is enforcing the minimum exchange rate with all the means at its disposal,” SNB President Thomas Jordan told reporters at a press briefing today. “We are prepared to buy foreign currency in unlimited quantities for this purpose. In this respect, our policies are totally unchanged.”

Italy – Bond auction come in with higher yields. The bank sold €8.0B in 12-month bills with an average yield of 2.840% vs 2.392% prior; and €2.884 billion of 3YR bonds vs a €3 billion max target with a yield of 3.89% vs 2.76% previously.

EUR/USD - Most-accurate foreign-exchange forecasters say the euro will slide as austerity-driven spending cuts from Spain to Italy reignite debt turmoil and drag the region into recession

- Nick Bennenbroek, head of currency strategy at Wells Fargo & Co., expects the euro to drop more than 5% to $1.24 at the end of 2012.

- Westpac Banking Corp., which had the second-lowest margin of error, predicts $1.26.

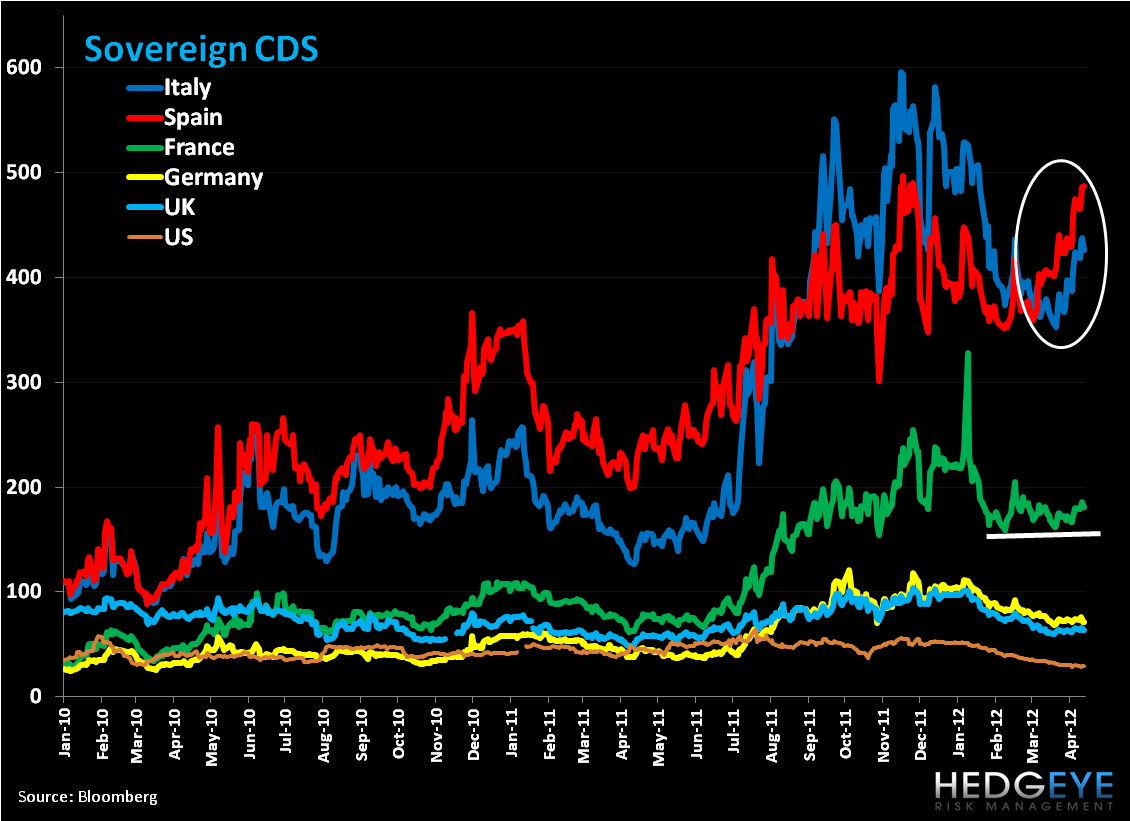

CDS Risk Monitor:

Week-over-week Spain saw the largest gains in CDS, +12bps to 487bps, while the other countries we follow were relatively flat. Ireland flashed an inflection, down -16bps to 589bps.

Data Dump:

Eurozone Industrial Production -1.8% FEB Y/Y vs -1.7% JAN

Eurozone Sentix Investor Confidence -14.7 APR (exp. -9.1) vs -8.2 MAR

Germany CPI 2.3% MAR Y/Y vs 2.5% FEB

Germany Exports 1.6% FEB M/M (exp. -1.2%) vs 3.4% JAN

Germany Imports 3.9% FEB M/M (exp. 1.3%) vs 2.4% JAN

Germany Wholesale Price Index 2.2% MAR Y/Y vs 2.6% FEB [0.9% MAR M/M vs 1% FEB]

UK PPI Input 1.9% MAR M/M (exp. 1.4%) vs 2.5% FEB [5.8% MAR Y/Y (exp. 4.8%) vs 7.8% FEB]

UK PPI Output 0.6% MAR M/M (exp. 0.5%) vs 0.6% FEB [3.6% MAR Y/Y (exp. 3.5%) vs 4.1% FEB]

France Bank France Business Sentiment 95 MAR vs 95 FEB

France Industrial Production -1.9% FEB Y/Y (exp. -1.2%) vs -1.9% JAN

France Manufacturing Production -3.7% FEB Y/Y (exp. -1.7%) vs -1.7% JAN

France CPI 2.6% MAR Y/Y vs 2.5% FEB

Italy Industrial Production -3.5% FEB Y/Y vs -1.7% JAN

Spain House Transactions -31.8% FEB Y/Y vs -26.3% JAN

Spain Industrial Output -3% FEB Y/Y vs -2.5% JAN

Spain CPI 1.8% MAR Y/Y vs 1.9% FEB

Sweden Industrial Production -7.1% FEB Y/Y vs 1.7% JAN

Sweden CPI 1.5% MAR Y/Y vs 1.9% FEB

Switzerland Unemployment Rate 3.1% MAR (UNCH)

Norway Industrial Production 3.1% FEB Y/Y vs 3% JAN

Ireland Consumer Confidence 60.6 MAR vs 57 FEB

Ireland CPI 2.2% MAR Y/Y vs 2.1% FEB

Ireland Industrial Production -3% FEB Y/Y (exp. -0.5%0 vs -0.2% JAN

Finland CPI 2.9% MAR Y/Y vs 3.1% FEB

Greece Industrial Production -8.3% FEB Y/Y vs -5% JAN

Greece CPI 1.7% MAR Y/Y vs 2.1% FEB

Greece Unemployment Rate 21.8% JAN vs 21% DEC

Portugal Industrial Sales 0.7% FEB Y/Y vs 2.9% JAN

Portugal Construction Works Index 61.4 FEB vs 63.2 JAN

Portugal CPI 3.1% MAR Y/Y vs 3.6% FEB

Russia Light Vehicle and Car Sales 13% MAR Y/Y vs 25% FEB

Turkey Industrial Production 4.4% FEB Y/Y (NSA) vs 1.5% JAN

Hungary Consumer Prices 5.5% MAR Y/Y vs 5.9% FEB

Hungary Industrial Production -3.4% FEB Y/Y vs -2.7% JAN

Interest Rate Decisions:

(4/9) Russia - Bank Rossii left the refinancing rate UNCH at 8.00%; overnight auction-based repurchase rate UNCH at 5.25%; and the overnight deposit rate UNCH at 4.00%.

(4/12) Serbia Interest Rate UNCH at 9.50%

The European Week Ahead:

Sunday: Apr. UK Rightmove House Prices

Monday: Feb. Eurozone Trade Balance; Moody's Completes Review of 24 Italian Bank Ratings (Decision on Apr 20); Feb. Italy Trade Balance, General Government Debt

Tuesday: Apr. Eurozone Zew Survey Economic Sentiment; Mar. Eurozone New Car Registrations, CPI; Apr. Germany Zew Survey Current Situation and Economic Sentiment; Mar. UK CPI, RPI; Feb. UK House Prices; Feb. Italy Current Account

Wednesday: Feb. Eurozone Current Account, Construction Output; UK BoE Minutes; Mar. UK Claimant Count Rate, Jobless Claims Change; Feb. UK Avg Weekly Earnings, ILO Unemployment Rate; 1Q Spain House Price Index; Feb. Spain Trade Balance; Sweden Riksbank Interest Rate

Thursday: Group Meeting of 20 Deputy Finance Ministers (Apr 19-22); Apr. Eurozone Consumer Confidence – Advance; Feb. Italy Industrial Orders and Sales; Feb. Greece Current Account

Friday: Annual Spring Meeting of the IMF/World Bank (Apr 20-22); Mar. Germany Producer Prices, IFO Business Climate, Current Assessment, and Expectations; Mar. UK Retail Sales

Sunday: First round of the French Presidential Election

Extended Calendar Call-Outs:

22 April: French Elections (Round 1) begins, to conclude in May.

29 April, 6 or 13 May: Potential Greek Presidential Elections.

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst