“Panics do not destroy capital; they merely reveal the extent to which it has been previously destroyed by its betrayal into hopelessly unproductive works.”

-John Stuart Mill

John Stuart Mill was arguably the most influential philosopher of the nineteenth century and his writings are still widely studied. Mill is probably best known for “On Liberty”, which discusses the limits of power that can be justly exercised by society over the individual. Underscoring his views on liberty are the harm principle and the idea that the individual should have the right to act as she wants as long as those actions do not harm others. To Mill, protecting and defending individual rights in the face of a potentially tyrannical majority are critical.

One way a majority can negatively influence the rights of the minority is through capital allocation by the government. We often cite the long run historical work of Reinhart and Rogoff that highlights when government debt-as-a-percentage of GDP reaches 90%, or more, economic growth slows. Certainly governments play a critical role in providing certain services that are critical and broadly benefit society, but, at a point, government works become unproductive.

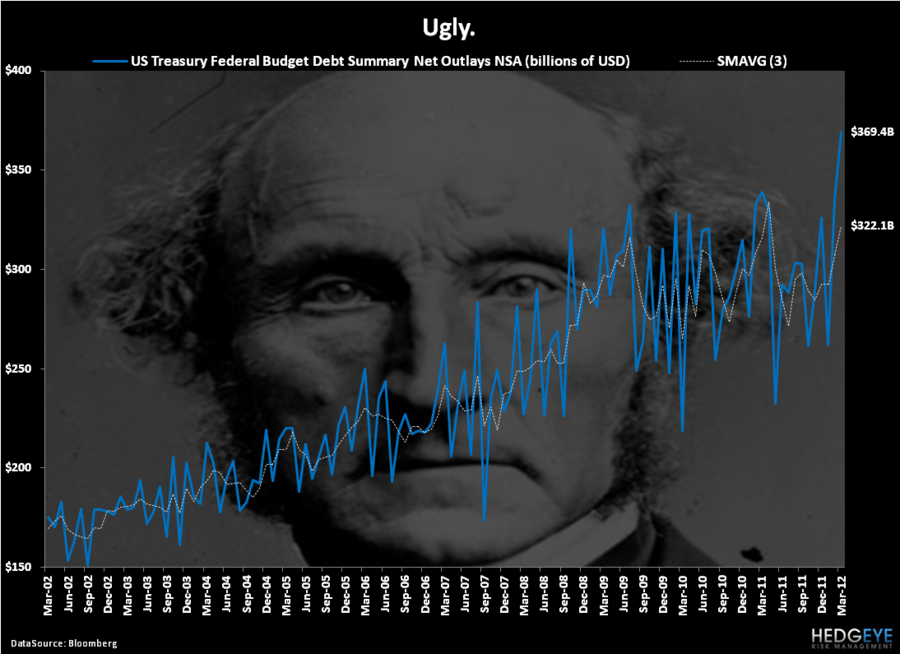

With all that is happening in the world, I’m sure many of you missed the U.S. budget numbers for March. As I said on twitter ( @HedgeyeDJ ), they were, in one word, ugly. The federal government received $171 billion in revenue and spent $369 billion for a total budget deficit of -$198 billion, or 5.5% year-over-year monthly growth in the deficit. This is the largest March budget deficit of any nation, ever.

Almost exactly a year ago, in a note titled “The Case of the Missing Stimulus”, I wrote:

“Interestingly, if we look at government spending in the 2008 – 2010 period we can actually see the impact of the stimulus act on government ledgers. In fact, according to usgovernmentspending.com the U.S. federal government spent $2.98 trillion in 2008 and $3.59 trillion in 2010. So, the net increase over this period was just over $600 billion, which roughly equates to the spending portion of The Stimulus.”

My point in that note was that while there was a one-time step up in government spending, there has not been a step down as the stimulus plan has been anniversaried. A year later the same story holds.

The Chart of the Day today highlights government outlays by month going back ten years. The conclusion is that the “one-time” increasing in government spending for the stimulus plan has led to a seemingly permanent increase in government spending. Given the anemic growth we’ve seen in the U.S. over the last 18 months, it is pretty clear this spending fits the category of Unproductive Works.

At 11 am eastern today we will be holding our quarterly theme call. (Please email if you are qualified subscriber and do not currently have the dial in information.) The quarterly theme call is our summary of what we think will matter in the coming quarter from a global macro perspective and the best way to play the themes via asset allocation. The themes for this quarter are as follows:

- The Last War: Fed Fighting - We take a historical look at U.S. Federal Reserve policy to contextualize the impact of Ben Bernanke's Policy to Inflate, Extend & Pretend rock-bottom interest rates, and Burn the Buck on the broader economy and financial markets from Main Street to Wall Street.

- Bernanke Bubbles - A highlight of the top ten leverage price bubble charts perpetuated and encouraged by The Bernank's policy stance.

- Obvious Asymmetric Risks - In a macro environment of slow global growth and historically low interest rates we present asymmetric risks to capitalize on over the intermediate term. Low equity market volatility is but one signal of what's ahead for investors.

Underlying much of the discussion today, will be our view that global growth is slowing. On that note, and despite rumors to the contrary, Chinese GDP growth came in at 8.1%. This was well short of the estimate of 8.4% growth and dramatically below the “whisper” number of 9.0% that was floated yesterday. This is the 5thconsecutive decline and the slowest growth rate in three years. As our Asian Analyst Darius Dale would likely tell you, the actual number shouldn’t surprise anyone as the Chinese have already told us they are going to slow growth.

In other global macro news, European sovereign debt issues are once again front and center. Yesterday, I wrote a note on Spain and the impact of further decline in real estate prices on Spanish growth (if you didn’t read the note and want a copy, ping ). Spanish 5-year CDS are wider again this morning at 492 basis points. Meanwhile, Spanish equities are down another -2% taking their return in the year-to-date to -14%. As if that wasn’t bad enough, Spanish CPI was also up +0.7% for the month. (Not so great for the 23% of Spaniards that are unemployed.)

If you are looking for a positive catalyst today, Chairman Bernanke speaks at 1 pm today in New York. Even if he doesn’t hint at it, no doubts rumors of QE 3, 4, 5, and 6 will be spreading faster than Chinese growth ahead of his speech.

As you head into the weekend and start contemplating the upcoming Presidential election, I’ll leave you with a quote from a guy that knows a thing or two about U.S government, former President George Washington, who said:

“Government is not reason; it is not eloquent; it is force. Like fire, it is a dangerous servant and a fearful master.”

Indeed.

The immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, Japanese Yen (vs USD), Euro/USD, and the SP500 are now $1, $118.89-122.64, $78.74-79.66, $79.83-83.02, $1.31-1.33, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research