TODAY’S S&P 500 SET-UP – April 13, 2012

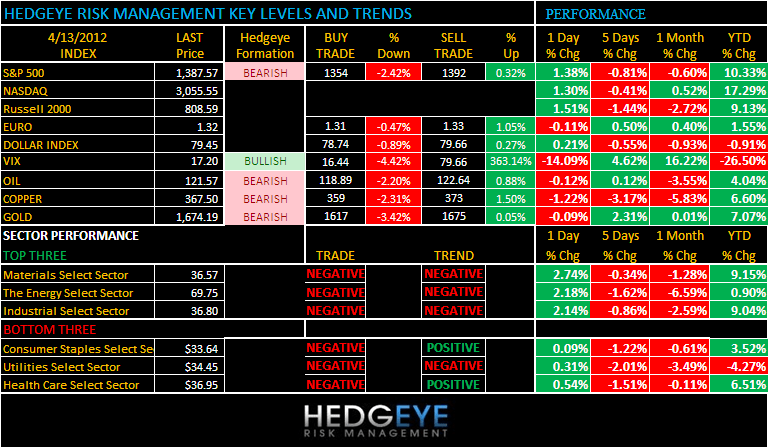

As we look at today’s set up for the S&P 500, the range is 38 points or -2.42% downside to 1354 and 0.32% upside to 1392.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 4/12 NYSE 1933

- Up from the prior day’s trading of 1684

- VOLUME: on 4/12 NYSE 756.67

- Decrease versus prior day’s trading of -4.24%

- VIX: as of 4/12 was at 17.20

- Decrease versus most recent day’s trading of -14.09%

- Year-to-date decrease of -26.50%

- SPX PUT/CALL RATIO: as of 04/12 closed at 2.11

- Increase from the day prior at 2.04

CREDIT/ECONOMIC MARKET LOOK:

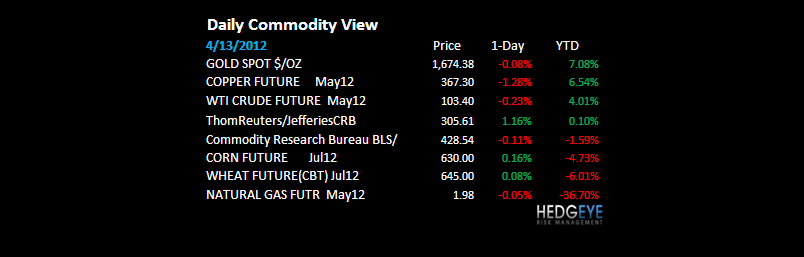

GROWTH SLOWING – away from the economic data (which now includes US employment gains slowing), Copper and 10yr UST yields are the most obvious signals this morning with Copper moving into a falling knife formation (-1.6%) and 10yr slicing back through our intermediate-term TREND support of 2.03% to 2.01% last.

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 2.01

- Down from prior day’s trading of 2.05

- YIELD CURVE: as of this morning 1.73

- Decrease from prior day’s trading at 1.77

MACRO DATA POINTS (Bloomberg Estimates):

- 8:00am, Fed’s Dudley speaks in Buffalo on the economy

- 8:30am: CPI (M/m), Mar., est. 0.3% (prior 0.4%)

- 9:55am: U.Mich, Apr. P, est. 76.2 (prior 76.2)

- 1pm: Bernanke speaks in New York on financial crisis and policy response

- 1pm: Baker Hughes rig count

- 2:15pm: Dudley visits cancer center in Buffalo

GOVERNMENT:

- President Obama speaks on benefits of trade with Latin America at Port of Tampa, Fla. 1:20pm

- Obama departs Tampa for Cartegena, Colombia, for April 14-15 Summit of the Americas

- Mitt Romney speaks to NRA annual meeting in St. Louis. 1pm

WHAT TO WATCH:

- JPMorgan Chase, Wells Fargo are first two big U.S. financial cos. to report 1Q earnings

- CPI probably rose at slower pace in March.

- Google gives founders share-issuing power at investors’ expense: corporate-governance experts

- U.S. video-game industry sales fell 25% in March, NPD says; watch GME, MSFT, EA, SNE

- Best Buy said to probe ex-CEO Dunn’s relationship with employee

- China’s below-forecast GDP growth of 8.1% may mark end of slowdown

- Spanish banks’ ECB borrowings climb to $300b in March

- Infosys sales forecast misses est.; follows report SAP off to slower 1Q start in North America; watch IT services stocks

- North Korean long-range missile launch fails

- Judge to consider approval of L.A. Dodgers bankruptcy plan

- Week Ahead preview: G-20, IMF Meetings, Goldman, Iran Talks

EARNINGS:

- JPMorgan Chase & Co (JPM) 6:58 a.m., $1.17

- Shaw Communications (SJR/B CN) 8 a.m., $0.38

- Wells Fargo & Co (WFC) 8 a.m., $0.73

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Sugar Traders Extend Longest Bear Streak Since ‘07: Commodities

- Corn Climbs on Signs of Rising U.S. Export Demand; Soybeans Drop

- Oil Drops First Time in 3 Days on China Slowdown, Naimi Pledge

- Copper Falls, Extends Second Weekly Drop as Chinese Growth Slows

- Gold May Decline as Some Investors Sell Following Weekly Advance

- Cocoa Advances as Some Investors May Be Buying; Sugar Retreats

- Coffee Crop in Vietnam Gets Boost From Heavy Rain, Aids Fruiting

- Commodities to Gain 5-20% in Second Half, Credit Suisse Says

- Gold Set for Rebound With Support at $1,600: Technical Analysis

- Cheniere Shale-Gas Exports Hinge on U.S.-Asia Price Gap: Energy

- Nuclear Halt in South Korea Seen Boosting Coal: Energy Markets

- Oil May Fall After Iranian Nuclear Program Talks, Survey Shows

- India Said to Consider 16% Increase in State Rice Purchase Price

- Sugar Traders Seen Bearish for Seventh Week

- ING Investment Favors Indonesian Coal Bonds on Asian Resilience

- Kansas Farmers May Increase Soybean Planting After Wheat Harvest

- Citigroup Countersued by Rajaraman in Singapore Over Gold Losses

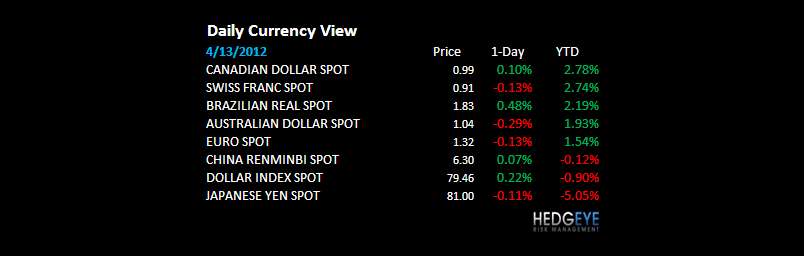

CURRENCIES

EUROPEAN MARKETS

EUROPE – certified train wreck remains in motion – it’s not different this time – you can’t ban economic gravity when imposing Stagflation on your people (Italian CPI +3.3% with Growth flat to down); Sold our long Germany position yesterday and re-shorted France because we think the gap between Spain -12% YTD and France’s CAC +2% YTD is going to narrow #Mean Reversion.

ASIAN MARKETS

CHINA – GDP growth slows from 8.9% Q4 to 8.1% Q1, missing whatever whisper found its way into the mo mo community yesterday (someone should tell them Global Macro isn’t like small cap rumoring); Chinese stocks acted fine on that because they act inversely with Commodity inflation and Chinese bank lending. Commodities bulls freak out.

MIDDLE EAST

The Hedgeye Macro Team