McDonald’s has a market capitalization of $100 billion for a reason. With the exception of a few years in the early 2000’s, McDonald’s executives have been very good stewards of their shareholders’ capital. Sadly, the same cannot be said for Burger King’s leadership over the past 10 years and the latest developments will do little, in our view, to enhance the company’s reputation. Bill Ackman recently gave a presentation which we refer to and reproduce material from time to time in this note.

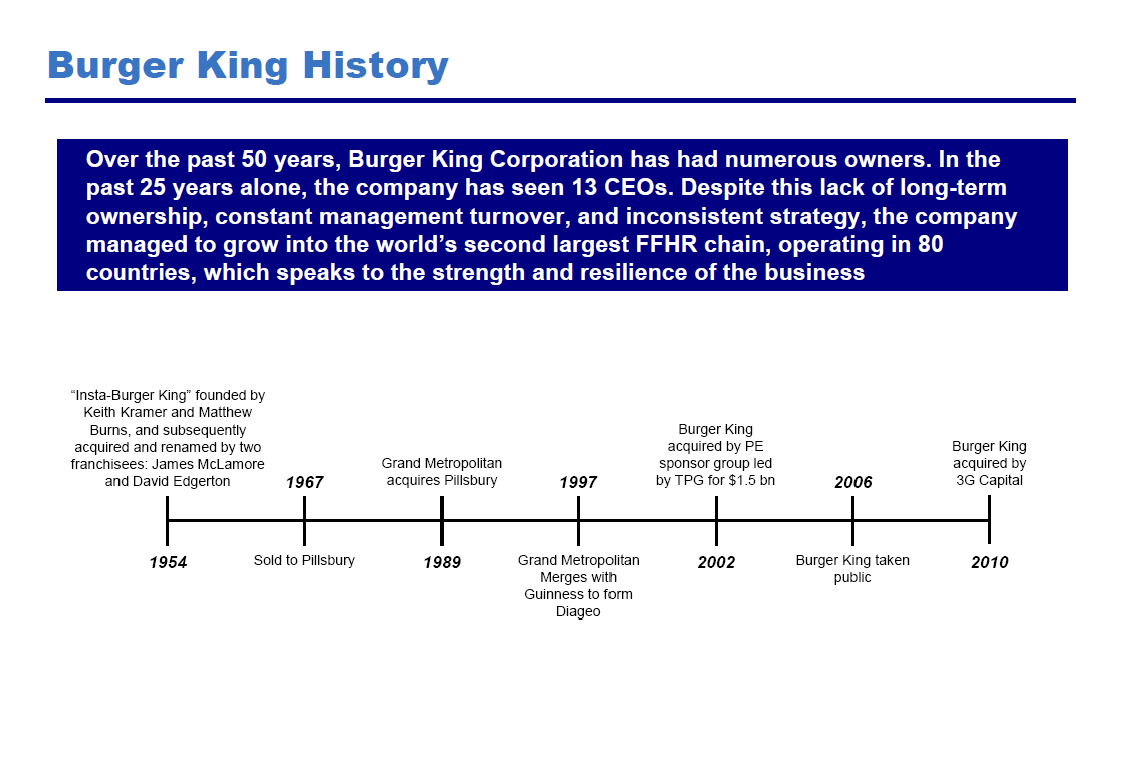

As you can see from the timeline of Burger King, below, the brand has been a cash cow that has lined the coffers of several different firms such as Pillsbury, Grand Met, and Diageo from 1989 through 2002. TPG and others got in on the act from 2002 through 2006. From 2006 through 2010, PE firms tried to cash out while the company was public but, ultimately, the chain failed to gain fundamental momentum and 3G Capital took it over.

Our view is that the overriding motivation of several owners throughout the years, and now 3G Capital, has been to starve the brand of capital in order to pay parent shareholders nice and quickly. Burger King’s issues may be so substantial that the chain may be “too big to fix”, at least in the near term. By our reckoning, the last two private equity firms that have taken ownership of the company have deprived the it of $1 billion or more in capital that could have been used to improve the company’s relative standing versus its competitors, many of whom Burger King now struggles to keep up with. The least favorable comparison for Burger King is McDonald’s. Between 2002 and 2011, McDonald’s has spent between $5 billion and $6 billion in capex on its U.S. business alone. While McDonald’s system is still in the process of being upgraded and does include some stores in need of remodeling, a plan is in place and the system has not been starved of capital as Burger King’s has.

As an aside, it is not at all surprising that Wendy’s is in a similar position. Similarly to Burger King, the company has been mismanaged for years and now faces a $3.7 billion price tag to fix its system with no prospect of generating cash flow any time soon. Over the past four years Wendy’s current owners were more concerned about buying back stock, it seems, than upgrading the asset base. We can ask the same “too big to fix” question about Wendy’s and becomes more apparent as the Burger King conversation grows as the IPO nears.

However, despite the continuous issues that have dogged the chain, its owners of 18 months have claimed that Burger King is back. Somehow, having invested no capital into fixing the business, its problems have been resolved.

Ask yourself how many of your own problems have you solved by ignoring them. Not many. Not only has 3G Capital not invested any capital in the company, it sucked $295 million out of the business last year. The evidence for the company being back, in terms of its fundamental performance, is four months of positive same-store sales during the most favorable weather the restaurant industry has seen in years. Before this recent period, comps were negative for three years.

There are very few industries that are more competitive than the QSR segment of the restaurant industry. Consumer tastes are constantly changing and barriers to entry are low. The dramatic changes that have taken place within the industry over the past ten years underscore that point. The bar has been risen in terms of the consumer experience at every stage of the process; Chipotle’s “assembly-line” ordering, Starbucks’ look and feel, and Domino’s online ordering experience are three examples of companies making the necessary investment to capture share. Burger King has done none of that and is facing a difficult reality in this new QSR world.

The harsh competitive environment awaiting Burger King is typified in every day part and most categories – the burger category in particular. Breakfast has been dominated by MCD, along with SBUX and DNKN in the North East. Others, such as Wendy’s, have found it difficult to gain traction and we expect the same for Burger King. Upstart “better burger” chains are growing rapidly and taking share in a market that Wendy’s has also signaled intent to capture better. As consumers demand higher standards, Burger King is going to have to invest billions of dollars in capital over a period of years to get its brand perception to where it needs to be.

According to Bill Ackman “the most valuable businesses in the world are brand royalty businesses that can grow without capital investment.” We have to give credit where it is due, Mr. Ackman is going to make money on this deal, but as independent observers, we have to assess what happens after his payday. Shareholders will be holding the bag and their rank will likely be swollen by new shareholders offering PE firms a selling opportunity.

It’s worth bearing in mind the factors driving the decision of Justice Holdings to make this transaction. Having been public for over a year, the company – as a SPAC – was compelled to complete a transaction by February 2014. The company’ s objective, as stated on Nicolas Berggruen’s website, was to “consummate a transation of $5 billion to $10 billion in Total Enterprise Value. We think Justice Holdings saw in Burger King the same attributes that many PE investors have seen in the past. BK is a tried and tested cash machine and it fits the bill perfectly for Justice Holdings.

Looking at valuation levels of peer companies that could accurately be labeled as “brand royalty”, it makes sense for a deal to be done now. We believe that the success of the Dunkin’ deal – for the insiders and others that got a piece of the deal – is the biggest driver behind the timing of the Burger King deal. We have reservations about Dunkin’s long term prospects for growth but, for now, the valuation implies that the market disagrees.

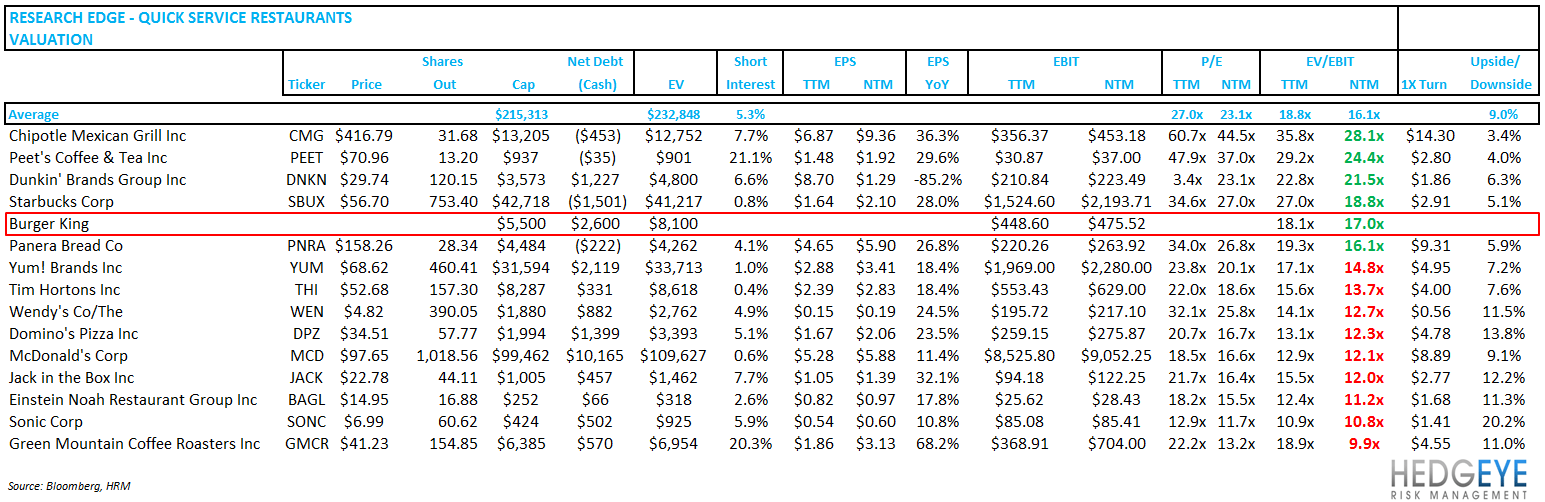

3G Capital purchased Burger King in October 2010 for $4 billion, which implied an EV/EBITDA multiple of 8.7x. Looking at the terms of the transaction with Justice Holdings, it seems the LTM EBITDA of $585 million and net debt of $2.6 million, implying a trailing EV/EBITDA valuation of 12.6x.

The clear question here is: what did the buyers of Burger King do to create ~4 multiple turns of value without one dollar of investment? The current strategy does not seem to be focused on investing in the brand. The remodel program is not yet being bought into by the franchisee base. If the current strategy fails, the question is whether that could be a death knell for the Burger King brand? We don’t think that is as dramatic as some might believe. Our best guess at this point is that Burger King may be better off shrinking in order to grow. As it currently exists, the turnaround may be too great a task. Closing underperforming stores and bringing the system AUV's higher may be a good first step on the road to recovery.

Below are our top 10 ten reasons why, according to the “Justice is Best Served Flame Broiled” slide deck, Burger King is fixed (so to speak):

- CAPITAL DRAIN: In April 2011, BK issued $685 million of notes, yielding $401.5 million of proceeds, of which $294 million was returned to 3G in the form of a dividend.

- BRAIN DRAIN: Last year, management gutted the company of G&A by $107 million and cut head count by 40%, taking EBITDA up 50% but various one-time adjustments have to be made to get there.

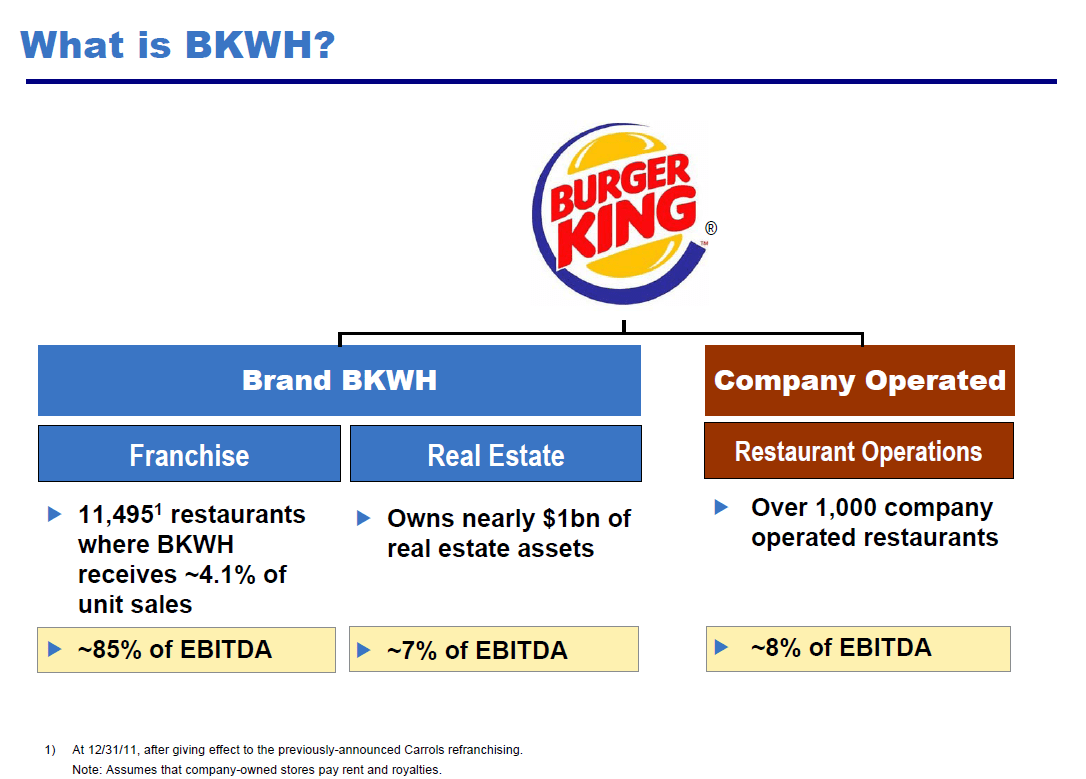

- ROYALTY STREAM/REMODEL PROGRAM: The company has reduced store ownership by 3%, reducing the need for capital spending. Unfortunately, 85% of the franchisee-base (measured in stores) has not bought into the remodel program thus far.

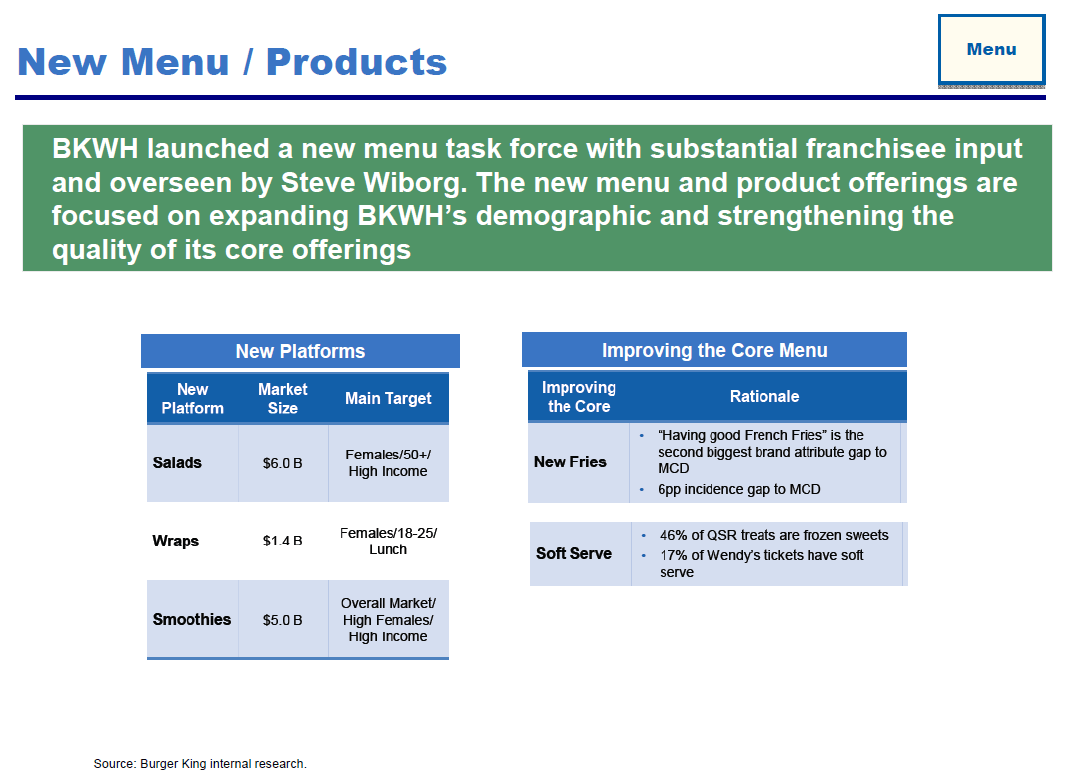

- NEW MENU INITIATIVES: BK is introducing a new menu that is defensive and looks just like products that McDonald’s is selling.

- POSITIVE SAME-STORE SALES: On the back of an extra trading day in February and the warmest winter in generations, the chain is seeing four months of positive SSS after three years of declines

- THE BRAZILIAN CONNECTION: The presence of Brazilian management professionals on the team somehow lends credence to the notion that BK could have more stores than MCD in Brazil?

- DOMESTIC QSR GROWTH: The QSR market in the USA is growing? That may be true but that growth is not coming from tired old chains like Burger King. Quick casual is the growth engine of QSR.

- IMPROVED FRANCHISEE RELATIONS: The franchisees apparently like the new management team but, at the same time, the new owners did not exactly take care of franchisees in 20 states with the Carroll’s refranchising deal.

- STRONG MANAGEMENT: Despite this claim, we are unsure that the team outlined in the presentation is best-equipped to overcome the challenges BK faces, particularly in the uber-competitive U.S. market

- THE ART OF A DEAL: The fact that Bill Ackman gave the presentation on behalf of a company he does not bode well for the storytelling capabilities of BK’s team. They will need to hone those skills rapidly over the coming months!

MANAGEMENT TEAM

As you can see from the management structure chart it does not look like the senior management team has any experience running a restaurant company or a U.S. publicly traded company for that matter. It explains why Mr. Ackman was speaking on behalf of the company in an unconventional conference call. However this story plays out, it will be very interesting.

FRANCHISEES ARE KEY TO THE STORY

The divergence between what the companies is saying and doing is very interesting. Management touted a $250 million line of credit from RaboBank as a source of capital for franchisees to help them jump start the re-image program. One slide in the presentation showed a staggering levered return of 50-87% from the remodel program. If the returns on capital offered by the reimaging package are that great, why did the Board of Managers decide to pay the shareholders of Parent, including 3G, a dividend of over $393 million in October 2011 having raised $401 million from the April 2011 sale of 11% senior discount notes due 2019.

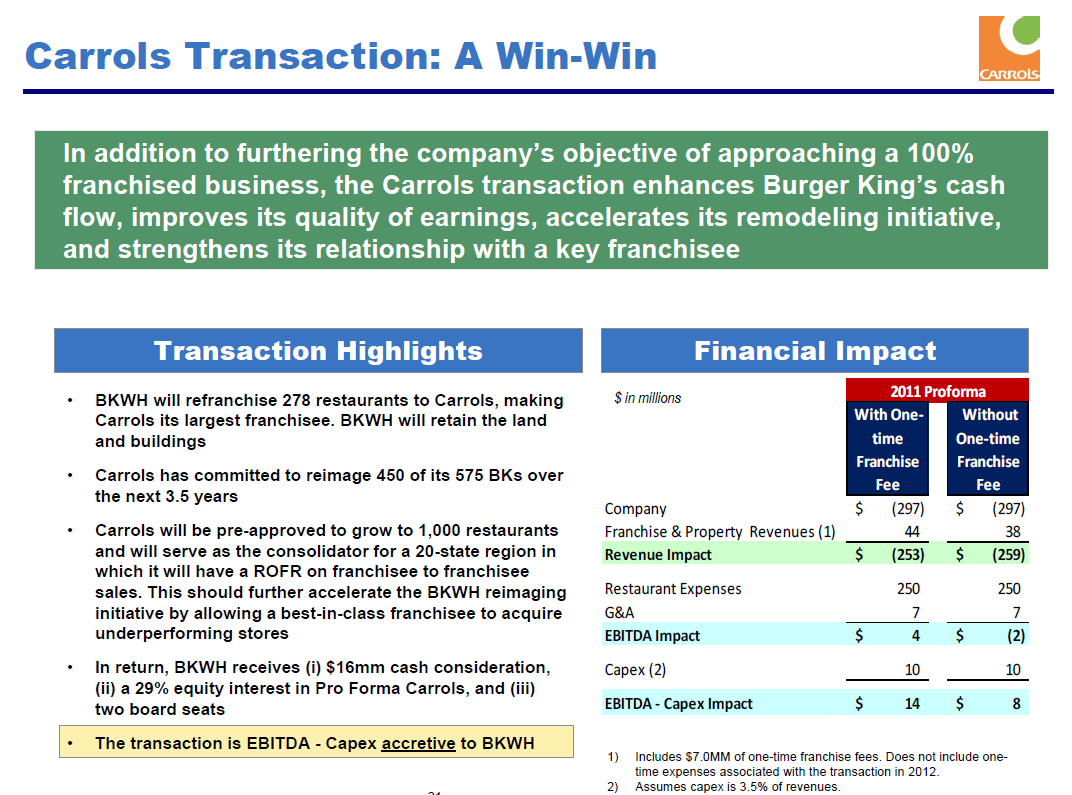

Carroll’s Corp (TAST) is a key player in the Burger King turnaround and is probably a better way to play the U.S. component of the story. On March 26th, Burger King refranchised 278 company-owned restaurants in the Ohio, Indiana, Kentucky, Pennsylvania, North Carolina, South Carolina and Virginia to Carrols Corp. In exchange for the stores, Burger King received a 28.9% equity interest in Carrols and total cash payments of $15.8 million. Upon completion of the transaction, Carrols will own a total of 575 units. To sweeten the deal, TAST also has received the right of first refusal on sales of Burger King restaurants by existing franchisees in 20 states and pre-approval to grow to 1,000 restaurants. With this transaction, Carrols also committed to remodeling approximately 450 of its units over the next three and a half years.

Strategically, the deal was great for Carrols, but came at the expense of the other franchisees. Without the Carroll’s deal in place (only completed a week before the Justice deal being announced), management could not tout the franchisees buy-in of the new remodel initiatives. But the reality is that the terms of the deal mean that Carrol’s shareholders will be gain much more than non-TAST franchisees or new BK shareholders. Without assuming further cuts to G&A, we see the deal as being dilutive to Burger King’s EBITDA.

Lastly, the company is stating that it has franchisee commitments to remodel 1,500 units with no specific time period for investors to go on besides what TAST has said in its press release. The obvious issue here is that 450 of the 1,500 units are going to be converted by Carrol’s Corp, leaving 85% of the system with no time frame or money to fix the system.

The future health of the franchise system is also far from certain. The idea that an inflection point in sales has been reached, independent of exogenous factors like weather, is premature. Sales trends have been near-worst-in-class at BK for years now. Volatility in commodity markets, particularly beef, may not impact the parent company if the store base is heavily franchised but to the extent that it impacts franchisees and their willingness or ability to agree to terms of reimaging agreements, it could impair Burger King’s ability to compete with MCD and others. If 85% of the system is not ready to play ball, who is going to pay for the reimaging program?

The management of Burger King has shown us that franchise systems are doing more now to help their franchisees get financing, and this is being confirmed by our friends at the Restaurant Finance Monitor. We have learned recently that Franchisors are not only developing their own loan programs and guaranteeing debt, but they may also need to “predict future health care costs.” The saga of the Affordable Healthcare Act and its myriad implications for the restaurant industry only adds more uncertainty to the equation for franchisees. According to the Restaurant Finance Monitor, “Brett Willis, senior vice president of franchise sales for California-based Johnny Rockets, said he was recently speaking with a lender who warned him that his bank would like to see franchisees' potential health insurance costs under the new health care law going forward."

WHICH DOES NOT BELONG AND WHY?

The new owners of Burger King have bet the ranch that the competition is “bloated”. Ackman, on the conference call last week, used that word to describe McDonald’s. The crux of the Burger King turnaround story is the reduction in expenses, not growth in EBITDA. Management cites three factors in its “Cost Reduction Initiatives” section:

- The implementation of “Zero-Based Budgeting”, resulting in $107mm G&A reduction in year one, with additional savings expected in 2012 (will G&A be cut more through refranchising?)

- Reduced 40% of corporate headcount, with entire restructuring completed by 2Q11

- Changed culture by creating meritocracy and restructuring incentive compensation

While the cost cutting drove 29% EBITDA growth in 2011 it’s a one-time event and now the story becomes more about the turnaround and the real financial performance of the store base. The easy money has been made!

More importantly, the lean corporate structure raises questions about the long-term impact of Burger King’s ability to invest human capital in future growth of the business and making the appropriate support and services available to franchisees.

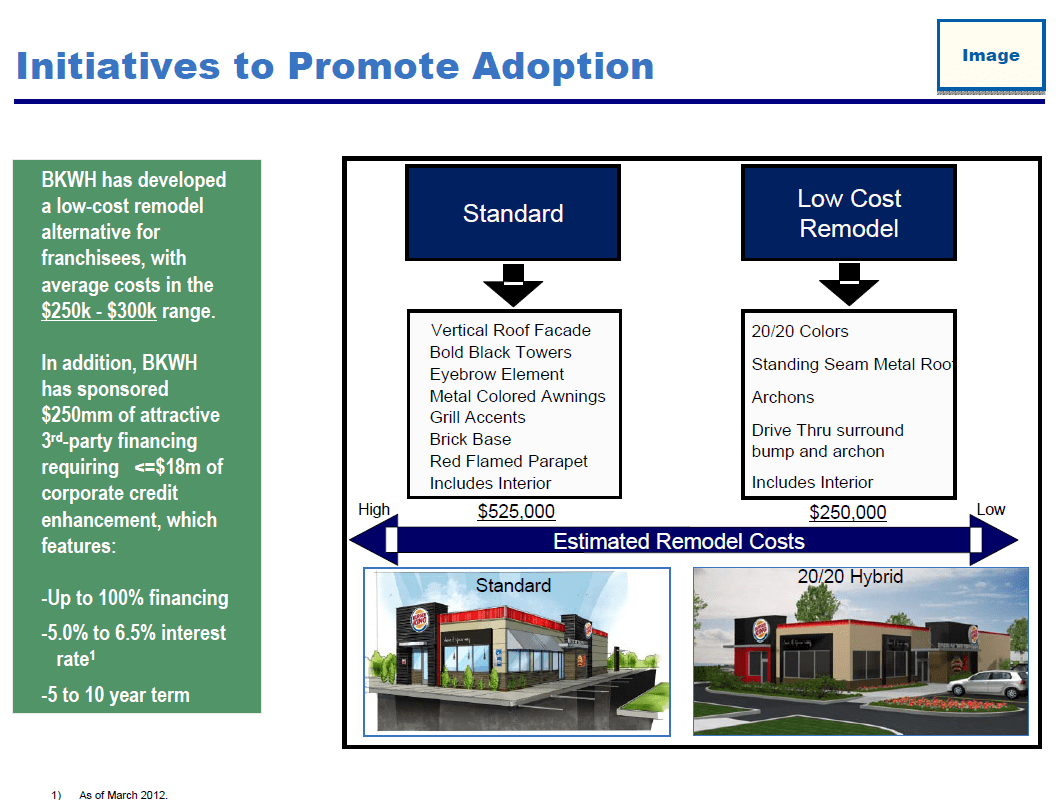

Most analysts that live and breathe the day-to-day happenings within the QSR business know that BK’s system has seen little-or-no progress in terms of the look and feel of the stores. No new formats have been introduced across a significant slice of the system for 12 years. This is evidenced by the fact that a large proportion of the system needs to be remodeled. By our estimation, as much as 95% of the asset base may need remodeling. A redesign program that was first mentioned in 2009, called 20/20, included a flashy design that included red-flame chandeliers. The cost was going to be $500-600k per store before the company decided to “revise” its plans. The reason for this revision and eventual abandonment, we believe, was that the cost was prohibitive for the majority of franchisees. Negative comps and $1.1m AUVs are not going to inspire confidence among franchisees to lever up.

The $1.1 million in average unit volumes makes the math of spending up to $600k per store a daunting prospect for franchisees. A 10-17% sales lift, or $110-187k, with a 35-40% contribution margin resulting in $75k in extra profit implies an eight-year payback period. We don’t think many of the franchisees we have spoken to would rush to sign up for that. Spending $300k per store with a 40% contribution margin halves the payback period but we think that is difficult to envision.

McDonald’s has been spending around $500,000 per store, with Wendy’s citing number closer to $750,000. This is possible because those chains’ stores generate higher unit volumes. While I think Wendy’s and their franchise system are unlikely to be able to afford to spend that much money, chances are they will come close to around $400,000 to 500,000 per store at the very least. Companies are making these capital commitments because they are compelled to; young consumers are demanding an experience – rather than just food – for their dollars and companies that are meeting that demand are driving the growth of QSR. In this respect, Burger King has been in the slow lane for a decade. Catching up to the competition, improving the consumers experience in every regard, is going to be an expensive proposition.

In order to sell a more palatable story to investors and to increase franchisee remodel activity, the current management team developed a less costly “20/20 hybrid” remodel, with an estimated average cost of $275,000. Further, the company is offering incentives of $150,000 per restaurant to franchisees, in the form of royalty reductions. The company is targeting 1,000 franchisee remodels in the US/Canada by the end of FY2012 and to complete 40% of the system in three years. As of the end of 2011 the company had 240 units remodeled and management has said that gross sales uplifts on the remodels are in the double digit range.

NEW MENU AND MARKETING INITATIVES

The new menu and marketing initiatives seem defensive to us. Devoid of anything new to the QSR consumer, the menu seems to essentially take on McDonald’s head on. We don’t see this as a viable strategy for Burger King at this stage of its turnaround. McDonald’s dramatically outspends Burger King in terms of marketing dollars (~30:1). To grow same-store sales, Burger King needs to branch out from its core customer base. With a menu that offers nothing new, essentially tackling the marketing machine that is MCD head on, how are they going to do that with a subpar asset base?

VALUATION

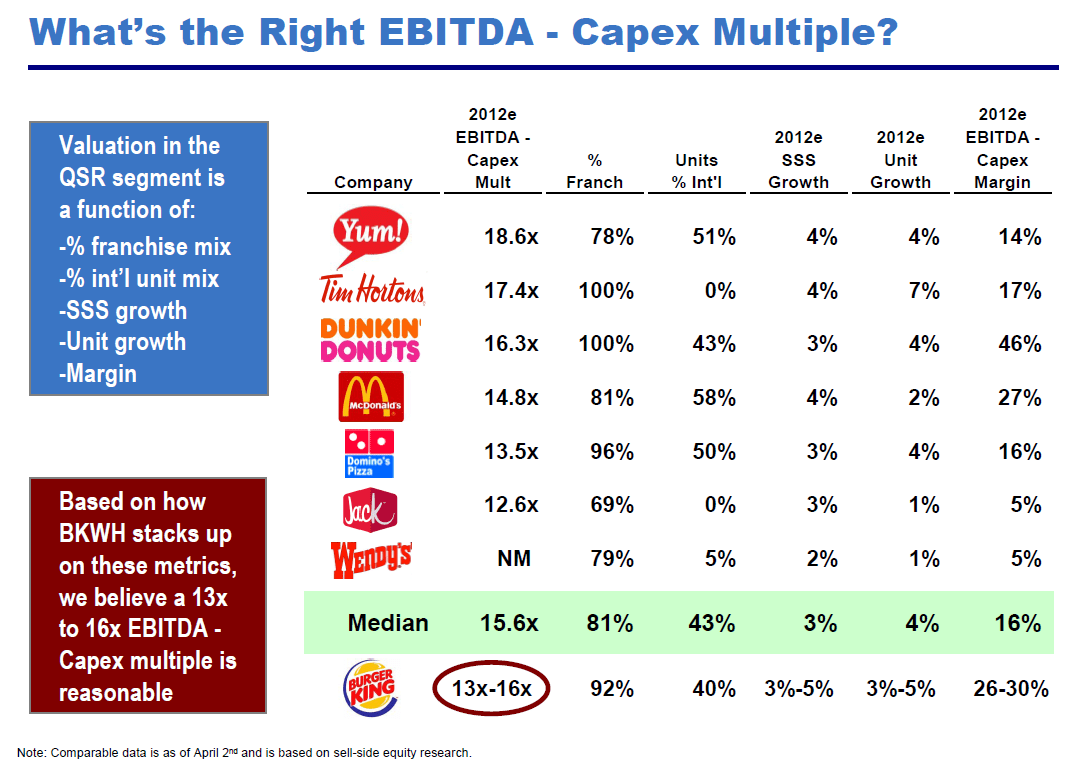

Justice Holdings likely took some time to reflect on which metric would make its Burger King story most attractive from a valuation perspective. That metric, as it turns out, is EV-to-EBITDA less capital spending.

The problem with this analysis is that it penalizes peer restaurant companies that are growing and, in the process, generating significant shareholder returns. Unfortunately for Burger King, it is not economical for the company to grow its store-base given the $1.1m AUVs and roughly $2m in cost associated with building and opening the store. Looking at EV/EBIT would be a more conventional way to frame the valuation point, and management does use it when outlining the potential value of Brazilian operations in the future, but taking capex out rather than D&A assigns Burger King a loftier multiple.

When we look at the potential transaction on an EV/EBITDA basis, Burger King is more expensive than THI, MCD, YUM, WEN, DPZ, and PNRA. Only PEET, SBUX, DNKN, and CMG would be more expensive. Should Burger King be trading at a premium to MCD? We do not think so.

Howard Penney

Managing Director

Rory Green

Analyst