Employment data released on Friday by the Bureau of Labor Statistics support the notion that restaurants saw strong top line trends in 1Q. Of course, this is not new news and whether or not those trends can meet expectations remains to be seen.

We continue to like EAT, PFCB, JACK and SBUX. DNKN and MCD are our favorite names on the short side.

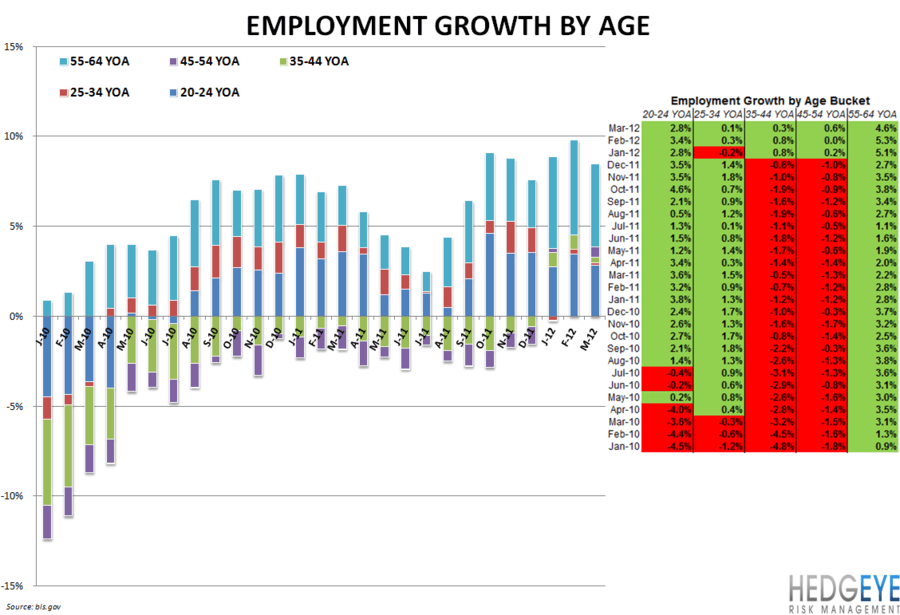

As the chart below shows, all of the age cohorts we track on a monthly basis saw employment gains in March. Besides the 45-54 YOA cohort, all of the age groups we track saw sequential declines from February’s year-over-year growth levels. This could be due to a fading of the impact of favorable weather versus last year, which is expected to have boosted 1Q employment figures and in some sectors pulled demand forward to the detriment of 2Q.

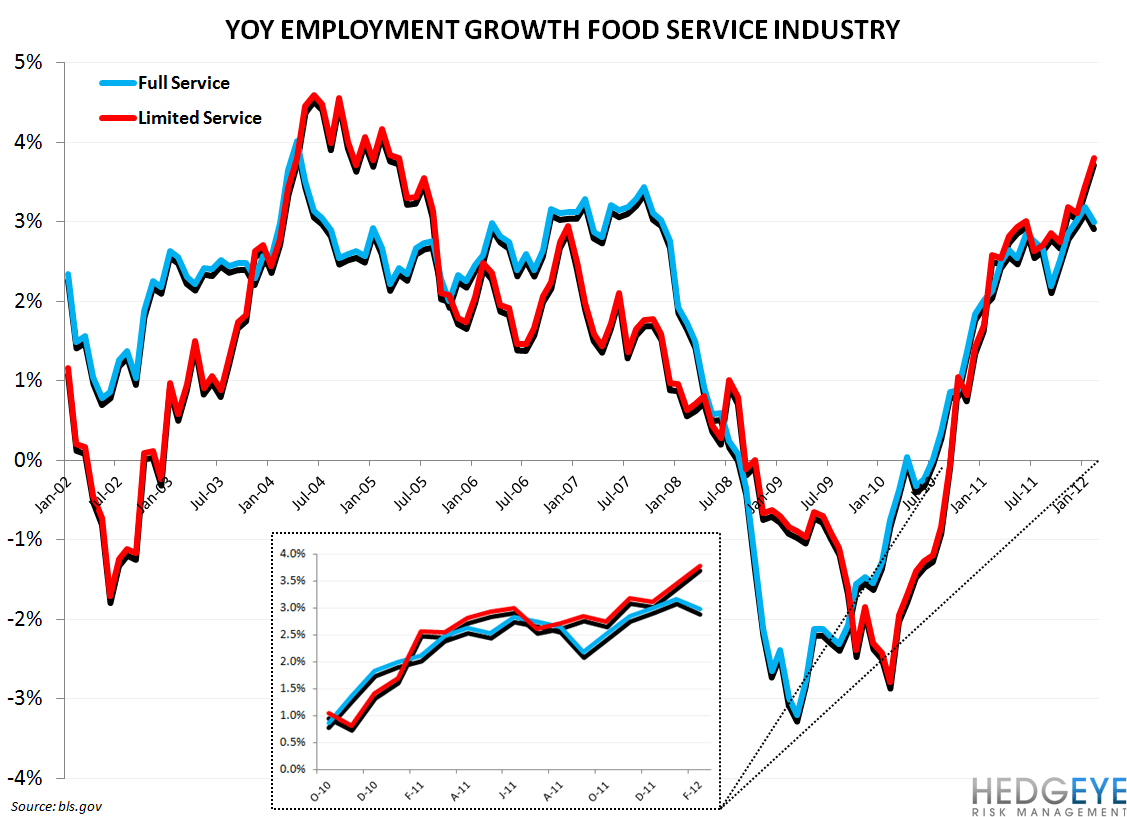

Hiring trends within the restaurant industry remains strong as of February (this data set lags by one month). As the chart below illustrates, hiring growth in the full service and limited service dining industries are growing at prerecession levels. The sequential slowdown in full service’s employment growth versus January is worth noting, however, with employment growth in that industry near peak levels.

This data is more impactful for casual than for quick service. As with the initial claims data, the correlation is far tighter between the casual dining datasets. The chart below shows an index of casual dining stocks versus full service employment annual growth. The correlation between the two datasets is almost 0.9 and tightens further when the casual dining index is lagged by one month. This makes sense, given that hiring and firing is generally reactionary. Nevertheless, in the event of a slowdown in casual dining stocks – which we expect – we will be looking to the employment data to confirm.

Howard Penney

Managing Director

Rory Green

Analyst