This note was originally published at 8am on March 26, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Failure deflates illusion, while success only makes illusion worse.”

-Nassir Ghaemi

“This isn’t a settled debate, and these interpretations could be proven wrong. But if they are correct, they raise several questions. Why do positive illusions occur? Can we only arrive at realism through personal hardship?” (A First-Rate Madness, page 55)

This weekend, as I was reading through Ghaemi’s provocative psychological discussion in chapter 3 of A First-Rate Madness (“Heads I Win, Tails It’s Chance”), I couldn’t stop thinking about our profession. Oh how the last 4 years have deflated our illusions of our analytical competence.

Or have they? Every time we’ve seen asset prices inflate (Q1 of 2008, Q1 of 2010, Q1 of 2011), we’ve seen the said seers of this business attempt to convince you that it’s “different this time.” Every time there is a “successful” rally, the consensus illusion of inflation morphing into sustainable growth gets worse.

Back to the Global Macro Grind…

The good news is that you can only pretend Growth Slowing doesn’t matter for so long. You can only ignore some of the worst volume and skew signals in global market history until you can’t. Gravity eventually bites.

Instead of Greece or Apple, this morning’s Top 3 Most Read on Bloomberg are as follows:

1. “Monti Signals Spanish Euro Risk as EU to Bolster Firewall”

2. “China Soft Landing May Be Hard For Commodity Exporters”

3. “Asia Stocks Fall as US Home Sales Damp Economic Outlook”

Hoo-wah!

Wasn’t Europe fixed? Isn’t China “decoupling” from the US? Can’t we pretend that Asian stocks and US Housing don’t matter until we get to quarter end?

“Under normal conditions, normal people overestimate themselves. We think we have more control over things than we do; we’re more optimistic than circumstances warrant…” (A First-Rate Madness, page 54)

There is absolutely nothing normal about the current Global Macro Economic conditions. Sure, you can be “optimistic” about life. I sure am. But realists tend to not blow their entire net worth to smithereens buying into fairy tales.

What is not normal and is not going away anytime soon?

- The Global Sovereign Debt Crisis

- The Bubble in Keynesian Economics (money printing)

- The Economic Reality that debt and inflation slow real (inflation adjusted) economic growth

If the US Stock market were to crash tomorrow, you’d have no business telling people you didn’t see any of this coming. This is the most obvious slow moving train wreck in world history – one that plenty of professionals still get paid to willfully ignore.

Since I doubt we’ll crash, that means the probability of a crash is going up as market prices do. Last week, global stock markets stopped going up (worst week for Asian and European stocks for 2012 YTD). Commodities have already started their decline.

Back to what’s just not normal:

- Sovereign Debt Crisis – we could have a healthy debate this morning as to who (Spain or Japan) has the more plainly obvious sovereign debt, deficit, and funding issues. The former Executive Director of the Bank of Japan (BOJ) said overnight that Japan has “crossed the Rubicon with really desperate measures.” Sounds like he was channeling his inner Hedgeye.

- Keynesian Policy Bubble – India (down another -1.8% overnight) has tried what every single Western academic dogma has suggested the Indians try, and it’s not working. They’ll be importing $125/barrel Brent Oil like the Japanese will in Q2 as their citizenry sees inflation running higher than real (inflation adjusted growth) = Stagflation.

- Inflation Slows Growth – yes, that is not only happening around the world (Commodity Inflation is generally priced in debauched Dollars), but you’ll see it in US Growth. So, when you see 3% US GDP growth for Q4 of 2011 (released on Thursday), pinch yourself and remind the person next to you that US GDP could be running at half of that growth rate right now.

The flip side of all this is that the success of our Global Macro model in forecasting intermediate-term growth slowdowns is making me delusional. Potentially, but that would imply that hedge funds who chased another top in commodity inflation are perfectly sane.

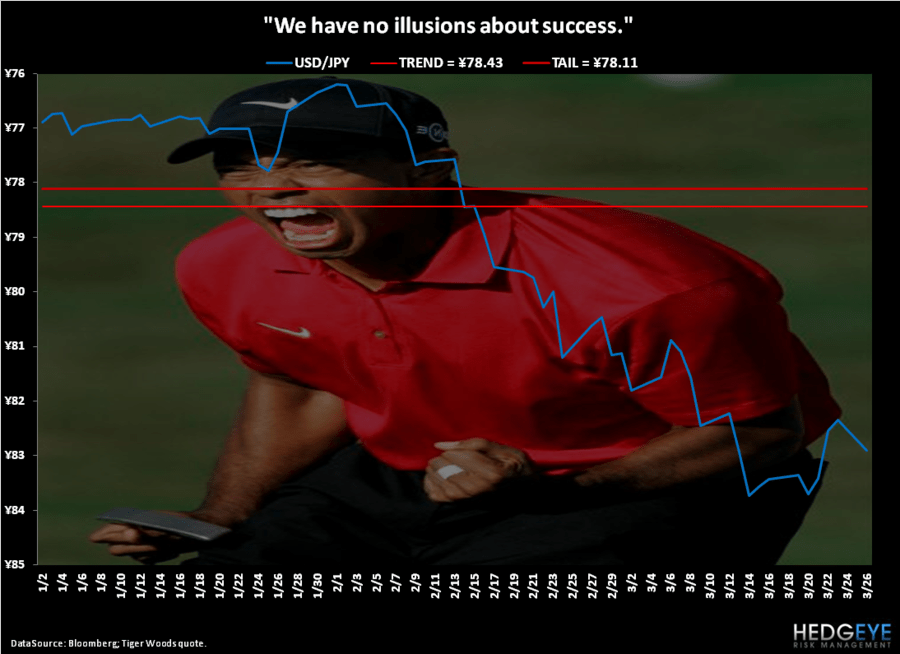

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, Japanese Yen (vs USD) and the SP500 are now $1637-1675, 124.55-126.62, $79.09-79.61, $82.22-$84.02, and 1397-1411, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer