This note was originally published at 8am on March 23, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Once you understand the main conclusion, it seems it was always obvious.”

-Daniel Kahneman

Obviously, after the SP500 is down for 3 consecutive days, Asian stocks have their worst week of the year, and the Japanese Yen drops 9% in a straight line, Global Growth Slowing matters – right? Right. Right. Everyone nailed it, again.

The aforementioned quote comes from the end of Chapter 22 in “Thinking, Fast and Slow” titled Expert Intuition: When Can We Trust It? Obviously, after seeing Sell-Side and Washington consensus miss the Growth Slowdowns in Q1 of 2008, 2010, 2011, and now 2012, the conclusion is that you cannot trust our profession’s broken “economic” sources.

“When evaluating expert intuitions you should always consider whether there was an adequate opportunity to learn the cues, even in a regular environment” (Kahneman, page 243). The globally interconnected cues associated with inflation slowing global growth have been as obvious as obvious gets.

Back to the Global Macro Grind…

Let’s check in with the “experts” this morning:

1. Credit Suisse – last week they said that “bond yields could rise further – this might help Equities” … so we’re still waiting to hear from them as to whether US bond yields falling this week might not help equities.

2. Goldman Sachs – their currency strategist, Tom Stolper (who has been on the opposite side of just about every big currency call we’ve made for the last few years) says buy the Japanese Yen and sell the US Dollar. We’re still on the other side.

3. Ben Bernanke – says “consumer spending has not recovered, it’s still quite weak relative to where it was before the crisis” and he is effectively daring consumers to draw down their savings even more to “fuel spending growth.”

You’ve just got to love how central planners think. Hey, why don’t we jam the entire world with Policies To Inflate, then chastise people for not having enough real (inflation adjusted) money left to buy things.

Nice.

The good news is that some experts still have some credibility. Some of them actually still believe in gravity. German Finance Minister official, Ludger Schuknecht, said yesterday that Italy and Spain are “too big to be saved.”

Spain looks awful, fyi.

Away from the Obvious Conclusion that stocks can in fact go down after they go straight up, it’s a fairly quiet morning here in New Haven, CT. That’s interesting, given that yesterday was actually the 2nd biggest down day for the SP500 of 2012. It was only down -0.7%!

That’s not normal. Neither are the US stock market’s volumes – they are dead as the trust embedded in America’s craw.

Looking at the 3 biggest SP500 down days of 2012:

- March 6th= down -1.5%

- March 22nd= down -0.7%

- Feb 10th= down -0.6%

Since they seem to have a completely arbitrary “year-end target” for just about everything else, ask your local expert at an Old Wall Street shop how many days we’ll have this year where the market closes down by more than 1%. Here’s my expert forecast – more than one.

Remember, as Growth Slows, intermediate-term tops are processes, not points. Here are the last 3 times we’ve shorted what we call immediate-term TRADE overbought tops in the SP500:

- February 15th= covered Short SPY for a +0.94% gain

- February 22nd= covered Short SPY for a +0.21% gain

- Current short position = +0.52% in our favor (unrealized)

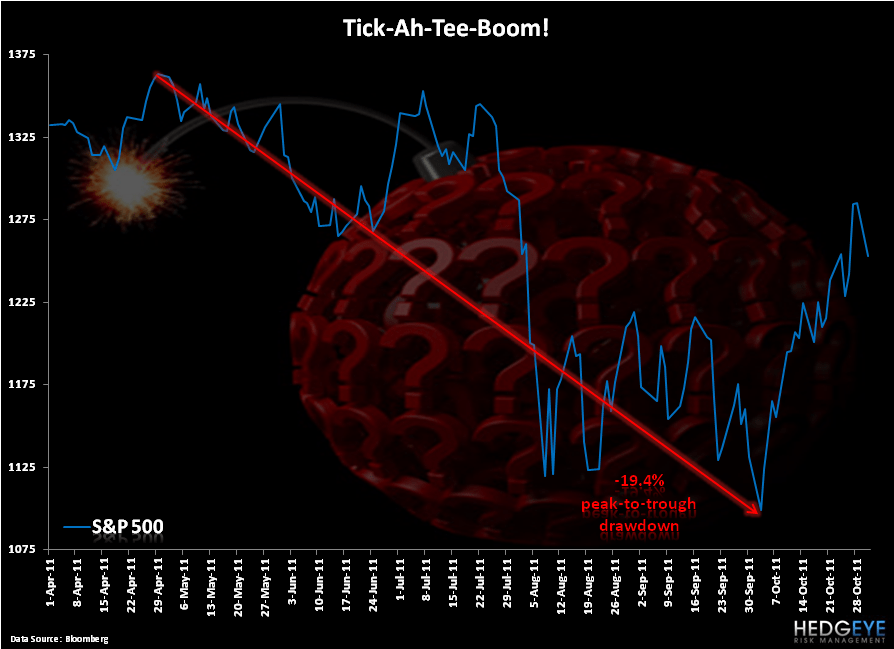

Obvious Conclusion: slim pickings for those of us who like to pick off price momentum chasing. That said, this was equally obvious in Feb-April of 2011. Then, tick-ah-tee-boom! The expert perma-bulls got run-over, again.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, Japanese Yen (USD/JPY), and the SP500 are now $1626-1666, $122.37-124.57, $79.33-80.45, $82.22-84.14, and 1375-1397, respectively.

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer