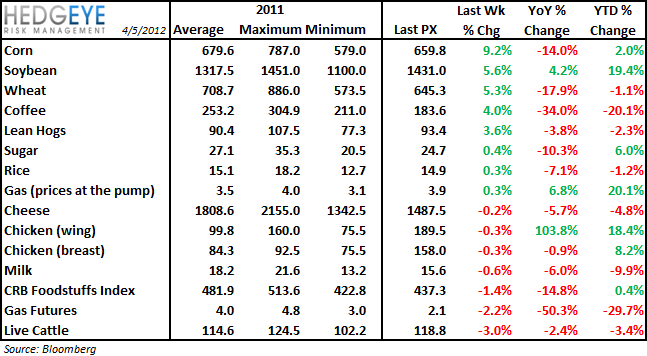

Despite dollar strength over the past week, grain prices shot up on strong USDA weekly export sales data exceeding average levels for the seventh consecutive week. Coffee took back some of the declines it has been posting year-to-date and beef prices led to the downside.

SUPPLY & DEMAND:

BEEF: prices are down -2.4% y/y and -9% since March 1st

SUPPLY

Supplies of beef within the US remain tight following the effects of last year's drought.

DEMAND

Consumer appetite for beef has been negatively impacted by the recent “pink slime” controversy. The stronger dollar also has the potential to hurt foreign demand for U.S. beef.

US beef export sales totaled 13,159 metric tons last week, moving up from -9,660MT the week prior.

CORN: prices are down 14% y/y

SUPPLY

Planting season is underway and, according to a USDA report released on March 30th, grain farmers intend to plant the largest acreage of corn since 1937. The Prospective Plantings Report by the National Agriculatural Statistics Service indicated that the nation’s growers intend to plant nearly 95.9 million acres of corn, up more than 4% or 4 million acres, from 2011.

The warm weather has enticed some to plant corn early. According to the USDA’s Risk Management Agency, Indiana and Ohio farmers with individual crop insurance plans have no replant coverage on corn planted before April 6, or soybeans planted before April 21.

DEMAND

Corn exports jumped 23% this week versus the week prior, according to the USDA’s latest U.S. Export Sales report. Corn exports totaled 793,100 MT, which was 7% above the trailing four-week average.

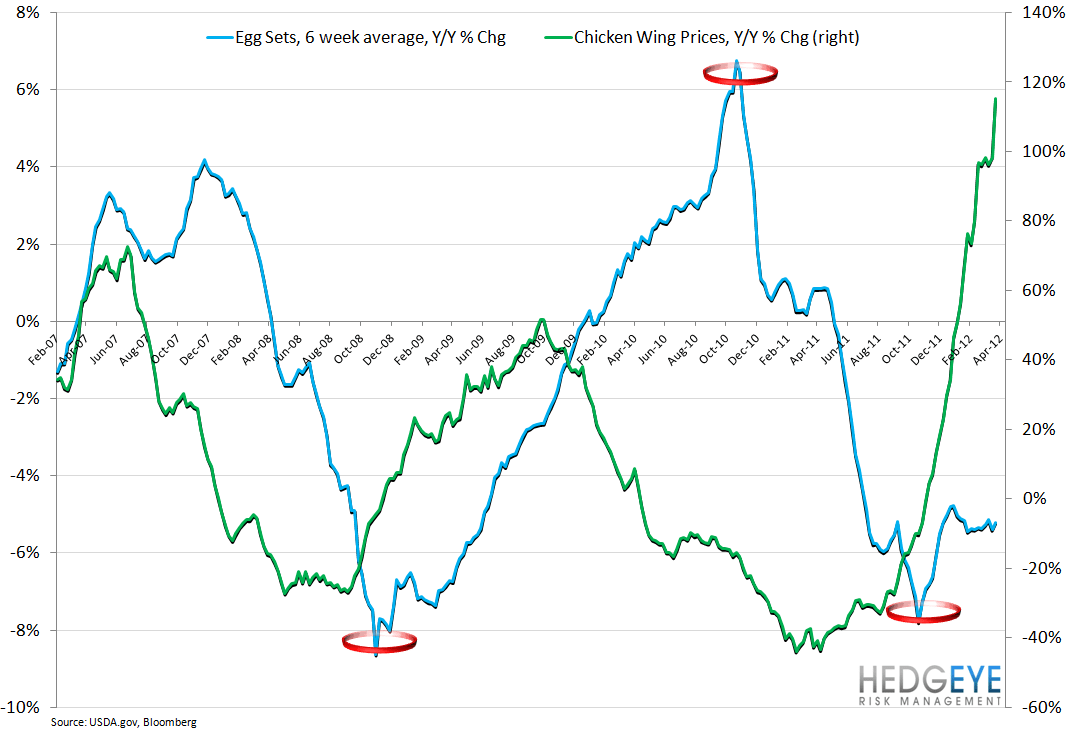

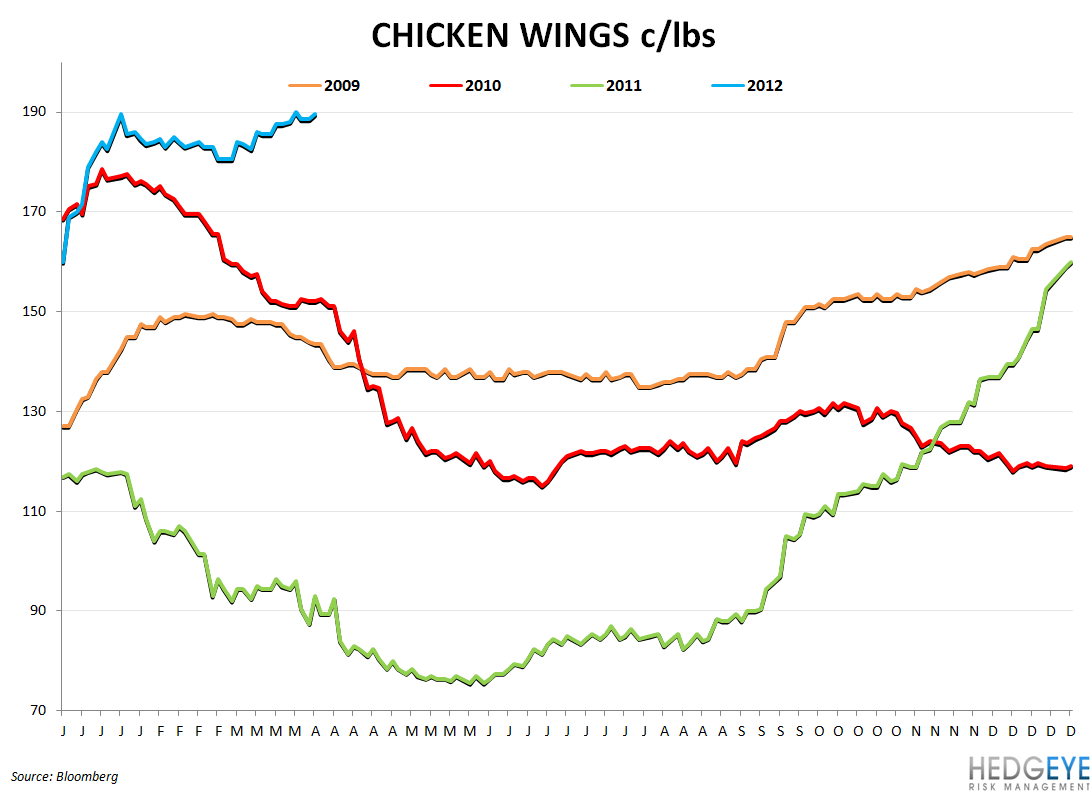

CHICKEN

SUPPLY

The egg set data, released every Wednesday by the USDA, is not signaling any recovery in chicken supplies any time soon. Year-over-year, the trailing six week egg set count is declining ~5.5% and wing prices, in turn, are trending near-vertical at almost +120% y/y.

THIS WEEK’S COMPANY COMMENTARY

On Beef… TSN COO James Lochner weighs in on the impact of “pink slime” controversy:

"In the short run, the negative publicity, I do believe had an impact negatively on ground beef demand, which will recover I think quite quickly. This was a very fast-moving thing. When you look at it, it was really a two-week event. So what will happen is, they'll be less lean beef, ground beef material available supply and the markets will adjust. Again in the spread businesses, it did have a negative short-term impact on the revenues, so the cattle cost probably will reflect that going forward. And we'll actually probably see a somewhere around a 2% to 3% reduction in the available beef supply. So it's not a positive thing. It's a very unfortunate thing because it was a very safe, very wholesome, very nutritious product that will now be not available in to the consuming public."

CONSUMER CALLOUT

Inflation

Gas prices have risen steeply year-to-date. Our view is that the impact of this has been somewhat muted by the more favorable weather conditions that most geographies have enjoyed this past three months.

Food prices are also squeezing consumers globally.

COMPANY COMMENTARY ON GAS PRICES

WEN: Obviously, we're all watching gas prices carefully and – but consumers seem to quite honestly have digested that quite nicely.

BAGL: If employment continues to be positive, again from my perspective, I think that sort of offsets any impact that you might get – we might get on gas prices … That said, if employment tightens up or we don't see continuously positive momentum than longer-term, obviously, if we get a $5 gas price, that's one of those price points that hits overall.

CBRL: We think that given our susceptibility particularly to – in the summer travel season to potential increases in gasoline prices that it is appropriate to be suitably cautious about our third and fourth quarter traffic outlook.

DRI: Yes, I would say as we look back, we don't think the current levels, the $4 current gas prices, no longer represents sticker shock.

CORRELATION

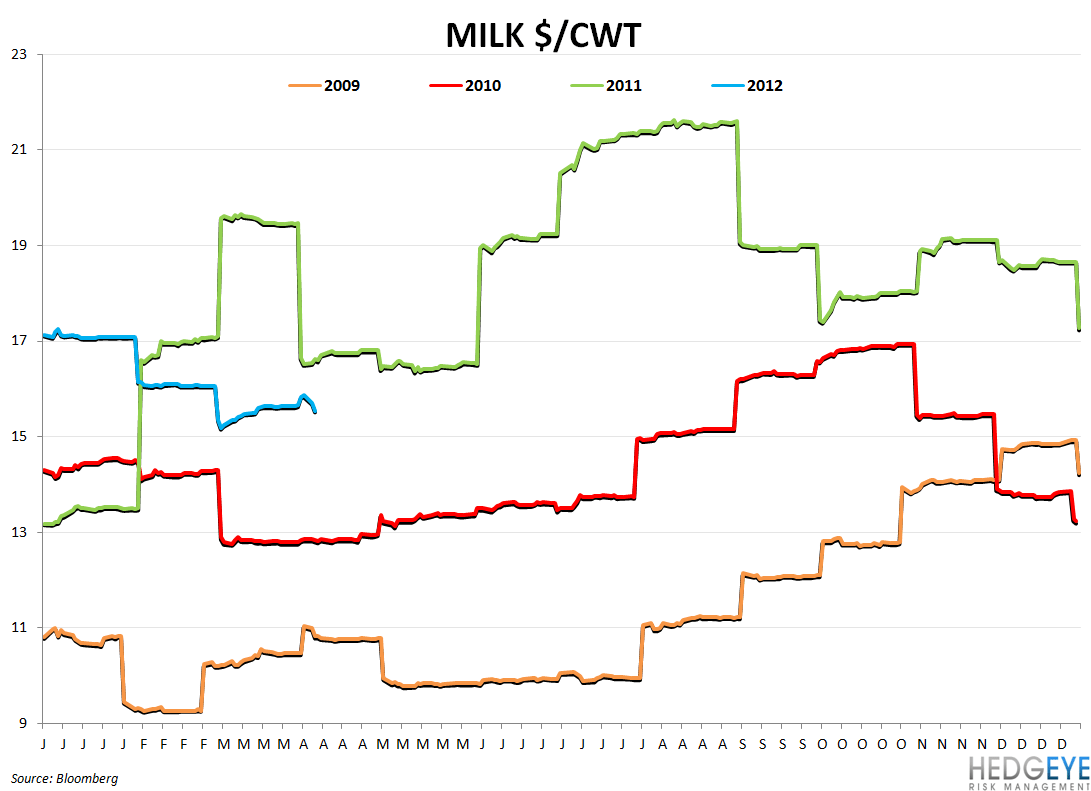

CHARTS

Howard Penney

Managing Director

Rory Green

Analyst