No Positions in Europe

Asset Class Performance:

- Equities: The STOXX Europe 600 is down -1.6% week-to-date vs -0.9% last week. Bottom performers: Italy -4.4%; Austria -4.0%; Greece -3.7%; Czech Republic -3.5%; Spain -3.2%; Portugal -3.2%. Top performers: Russia (MICEX) +2.1%; Ukraine +1.1%; Denmark+90bps.

- FX: The EUR/USD is down -2.13% week-to-date. WTD Divergences: RUB/EUR +1.78%, TRY/EUR +1.47%, GBP/EUR +1.00%, ISK/EUR +0.93%; HUF/EUR -0.51%

- Fixed Income: Greek 10YR bond yields again led the upward charge, gaining +109bps week-to-date to 22.13% (after a +100 bps move last week). In close step was Portugal, gaining +83bps to 12.23%, followed by Spain’s +37bps to 5.80%. Critically, both Spain and Italy continue to see rising yields in recent weeks, bucking an early March hold in and around 5.00% level. The German 10YR contracted -7bps to 1.75%, and remains the “risk-free” stand-out in the politically compromised Eurozone. We’ve long wondered why the lack of sovereign buying from the ECB’s SMP program in the last two months (including zero buying in the last three straight weeks) didn’t equate to rising yields. This week we clearly witnessed a reversal in this trend across the Eurozone’s weaker members.

Call Outs:

LTRO - Some of Europe’s biggest banks are preparing to return a chunk of 3yr LTRO money: senior bankers said UniCredit, BNP Paribas, SocGen, and La Caixa in Spain are preparing to pay back up to a third of the money they borrowed – estimated at €80-€100B in total – within the next 12 months.

Spain - The government said total borrowing needs will reach 79.8% of GDP for 2012, 30% below what was needed in 2011.

- PM Rajoy said: “The worst we could do now is nothing…It will be intense and difficult, but we’re laying down the grounds for Spain’s future recovery.”

- Finance Minister Luis de Guindos said: "From a budget perspective, the government is facing a lose-lose situation. If you don't make enough adjustments, markets will penalize you. But if you go too far, markets could also penalize you."

Italy - PM Monti reached an agreement with Italy’s main political parties on his proposal to ease firing rules and speed its passage through parliament.

Italy - BlackRock is buying Italian stocks amid optimism that PM Monti will succeed in cutting debt and boosting economic growth.

Swiss Franc - Broke through 1.20/euro for first time since the central bank set that rate limit but the SNB said it’s ready to buy unlimited quantities to prevent it from dropping below.

Hungary - Hungarian President Schmitt Resigns. Reason – Plagiarism.

Czech Republic - PM Petr Necas warned snap elections may be held quickly if the smallest member of the three-party ruling coalition makes good on its threat to quit amid preparations to cut the budget deficit.

In Review:

This week showed once again how much headline risk is governing European markets, especially on the equity side. Wednesday’s €2.6B Spanish bond auction, which came in at the lower range and saw yields on the 2015 maturity security jump to 2.89% vs 2.44% on March 15th and the 2016 maturity jump to 4.319% vs 3.376% on March 1st, rattled markets. The DAX closed down -2.8% on the day (Wednesday), CAC -2.7%, and FTSE -2.4%.

But the sovereign and banking risks in Spain aren’t new! We’ve signaled our bearish positioning on the PIIGS in recent months and continue to believe that the region is far from “out, and in the clear”. Not only has the fundamental data come in largely worse for the month of March (PMIs and confidence readings in particular--see below), but we continue to think the combined ESM and EFSF (€800B) is undercapitalized to deal with a sovereign default from the likes of a Spain or Italy.

Related, but getting less press, the German parliament (Bundestag) has agreed (across party lines) on a new decision-making process that requires all 620 members of the Bundestag to vote on nearly every detail of the euro rescue fundversus the previous quorum from a 41-member budgetary committee (with knowledgeable experts from all parties). Therefore, if the EFSF wants to make important decisions, in the future the entire Bundestag will have to regularly convene, in compliance with all legislative deadlines and regulations, with at least 311 parliamentarians present in order for a decision to be valid.

Can you say roadblock!

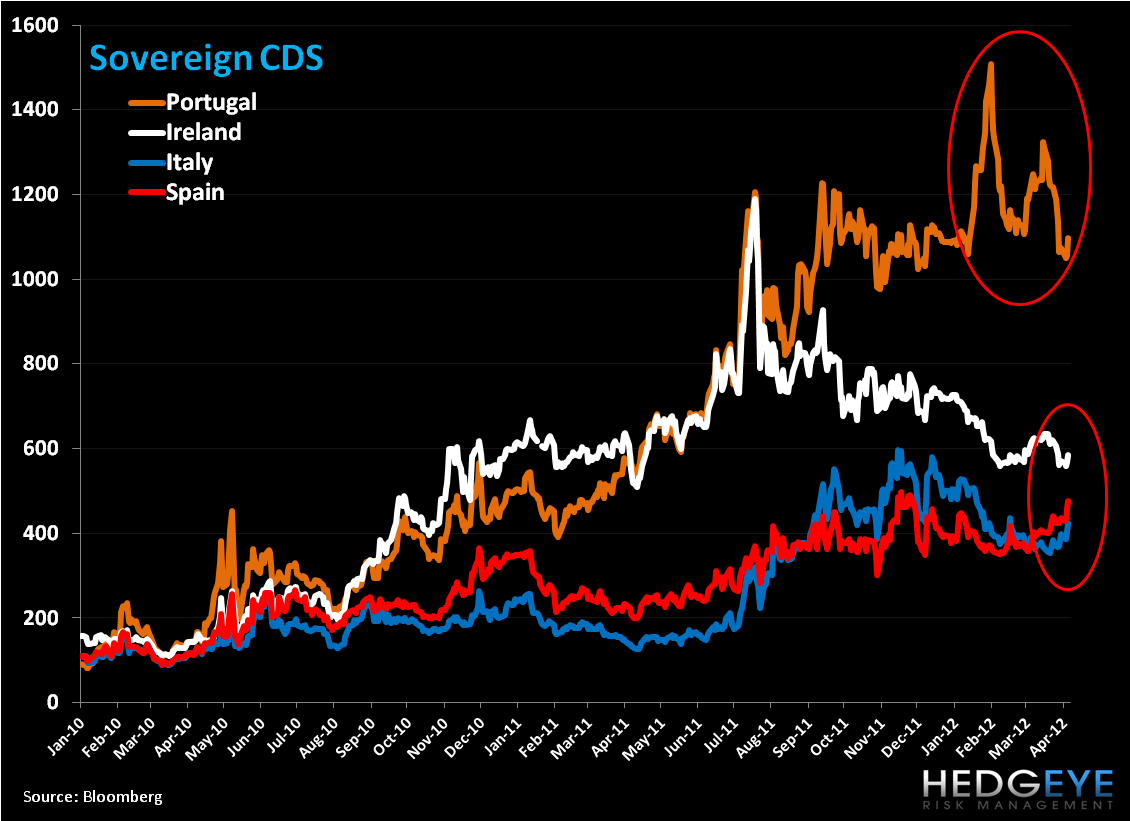

CDS Risk Monitor:

Week to date Spain saw the largest CDS gains, at +38bps to 475bps, followed by Italy (+27bps) to 424bps and Portugal (+23bps) to 1,097bps. The move in Portugal comes after two weeks of material declines, -143bps and -94bps, respectively.

Data Dump:

Eurozone Unemployment Rate 10.8% FEB vs 10.7% JAN

Eurozone Retail Sales -2.1% FEB Y/Y (exp. -1.1%) vs -1.1% JAN

Eurozone PPI 3.6% FEB Y/Y (exp. 3.5%) vs 3.8% JAN [0.6% FEB M/M (exp. 0.5%) vs 0.8% JAN]

UK New Car Registration 1.8% MAR Y/Y vs -2.5% FEB

UK Industrial Production -2.3% FEB Y/Y (exp. -2.1%) vs -4.0%

UK PMI Construction 56.7 MAR (exp. 53.4) vs 54.3 FEB

UK Manufacturing Production -1.0% FEB M/M (exp. 0.1%) vs -0.3% JAN [-1.4% FEB Y/Y (exp. 0.1%) vs -0.1%]

UK Halifax House Prices -0.6% MAR Y/Y (exp. -1.7%) vs -1.9% FEB

Germany Factory Orders -6.1% FEB Y/Y (exp. -5.5%) vs -6% JAN

Germany Industrial Production -1.0% FEB Y/Y (exp. 0.5%) vs 1.5%

Italy Unemployment Rate 9.3% FEB Prelim vs 9.1% JAN

Italy 2011 Deficit to GDP = 3.8%

Belgium Unemployment Rate 7.2% FEB vs 7.2% JAN

Ireland Unemployment Rate 14.3% MAR vs 14.4% FEB

Denmark Retail Sales -0.5% FEB Y/Y vs -3.3% JAN

Norway Credit Indicator Growth 7% FEB Y/Y vs 6.9% JAN

Switzerland Retail Sales 0.8% FEB Y/Y vs 4.7% JAN

Switzerland CPI -1.0% MAR Y/Y (exp. -1.1%) vs -0.9% FEB

Russia Q4 GDP 4.8% Y/Y vs 5.0% in Q3

Turkey Consumer Prices 10.43% MAR Y/Y vs 10.43% FEB

Turkey Producer Prices 8.22% MAR Y/Y vs 9.15% FEB

Romania Retail Sales 3% FEB Y/Y vs 9.9% JAN

Romania Producer Prices 5.9% FEB Y/Y vs 6.0% JAN

Interest Rate Decisions:

(4/4) ECB Interest Rate UNCH at 1.00% (in-line)

(4/4) Poland Base Rate UNCH at 4.50% (in-line)

(4/5) BOE Interest Rate UNCH at 0.50% (in-line)

(4/5) BOE Asset Purchases UNCH at 325B Pounds (in-line)

The European Week Ahead:

Monday: Mar. Germany Wholesale Prices (Apr 9-12); Mar. UK Lloyds Employment Confidence, RICS House Price Balance; Mar. Greece CPI; Feb. Greece Industrial Production

Tuesday: Apr. Eurozone Sentix Investor Confidence; Feb. Germany Exports, Imports, Current Account, and Trade Balance; Feb. UK House Prices; Mar. France BoF Business Sentiment; Feb. France Industrial Production, Manufacturing Production; 1Q Spain Business Confidence; Feb. Spain House Transactions

Wednesday: Feb. Spain Industrial Output

Thursday: Apr. ECB Publishes Monthly Report; Feb. Eurozone Industrial Production; Feb. UK Total Trade Balance, Trade Balance in Goods; Mar. France CPI; Feb. France Current Account; Jan. Greece Unemployment Rate

Friday: Mar. Germany CPI – Final; Mar. UK PPI Input and Output; Mar. Italy CPI - Final; Feb. Italy Industrial Production; Mar. Spain CPI - Final

Extended Calendar Call-Outs:

22 April: French Elections (Round 1) begins, to conclude in May.

29 April, 6, or 13 May: Potential Greek Presidential Elections.

30 June: Deadline for EU Banks to meet €106B capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst