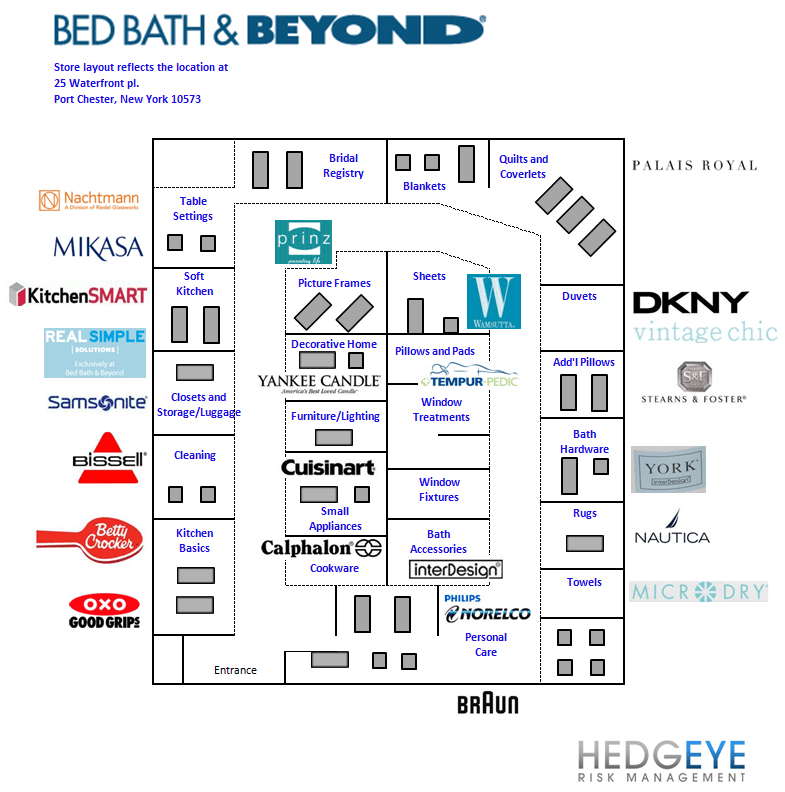

We were looking for a comp driven beat into the quarter, but results came in even better than expected with comps up +6.8% vs. +3.8%E and our +5%E. Additionally, the sales/inventory spread improved 6pts to +4% from -2%, which is gross margin bullish near-term. However, the key highlight from the call is the incremental spending in 2H of 2012 associated with a refocus on e-commerce suggesting the first increase in SG&A per sq. ft. growth in six years. The underlying fundamentals here have not changed – the Bed Bath & Beyond concept’s strength lies in its “specialty shop” format, which is designed to enhance the customer’s perception of service in-store (see our store map below). However, online BBBY remains susceptible to competitors offering the same value at a lower price. Mind the tail risk here.

Our in store analysis outlined in our 3/30 note "BBBY: E-Comm Threat Revisited" shows that BBBY’s product overlap with Amazon.com is north of 90% and for like product, Amazon.com pricing was ~1% below Bed Bath’s. Moreover, the disparity in pricing between the two was greater in higher price point categories.

While top line compares ease into 1H and inventories are well positioned entering 2012, The underlying fundamentals to our longer-term TAIL call remain unchanged. We’re at $4.51 in F12, up ~11% vs. guidance of up HSD to LDD. 1-2 years out, we’re modeling EPS of $4.80 in F13 & $5.12 in F14 vs. $4.94 & 5.91 respectively.

From our 3/30 note "BBBY: E-Comm Threat Revisited":

TAIL: (Tail=3 Years or Less)

BBBY was the primary competitor that ‘nudged’ Linens n Things into Chapter 11 in 2008 alongside the recession and bursting housing bubble. After 3 years of shrinking operating asset turns and margins eroding, BBBY improved both in 2009 & 2010. While BBBY’s aggressive expansion and promotional cadence was largely the nail in the coffin for LIN, many people overlook the pressure from the e-commerce home category. Our analysis below shows that Bed Bath and Beyond has a 93% product overlap with Amazon.com which exposes BBBY’s primary store format (85% of the 1174 stores) to online competitive threat. In other words, it was not just BBBY that put LIN out of business, it was Amazon and other dot.com competition. Dot.com is still hungry, and with LIN’s $3.5bn in revenue gobbled up by BBBY ($10bn in revs), AMZN and the like, it will still go after bricks and mortar opportunities.

While alternative store formats like Christmas Tree shops and Buybuy Baby are less at risk, we expect the long-term tail risk to amass as the consumer focus shifts to omni-channel. BBBY has already begun to reaccelerate capital spending as a percent of sales on new stores, remodels, IT enhancements & a new fulfillment center but this might be too little too late. While this may increase customer retention, our concern here is that BBBY will need to spend more to stand still.

Check out our BBBY Management Scorecard

The BIG ideas in retail come when a company’s triangulation of EBIT margins and asset turns both improve simultaneously. Check out the chart below. The three years leading up to 2008 were abysmal. So was BBBY’s stock performance. From ’08 through ’11, we’ve got asset turns improving along with EBIT margins. That’s a big RNOA accelerator. Pretty simple. But once margins OR asset turns start to stall, then multiple expansion goes out the door. That’s where the TAIL call with this company is headed.

For the past three years, earnings growth has been near 30%. For the next three, we have it hovering in the single digits. Take a look at history, this company is not afraid to shrink its net income.

Product Overlap:

What we did: We conducted a detailed analysis on the different plan-o-grams in different sized Bed, Bath and Beyond stores. Then we looked at overlap among a variety of store formats. Then we literally scanned each product, and compared to either a) the exact product online, b) a ‘pretty darn close’ product by the same brand – one with enough tweaks for BBBY to call it exclusive, when its really close to being the same thing, and c) a competing product in a more commodity category that can act as a substitute.

Out of the product sold through Bed Bath & Beyond stores, our analysis showed there was a 52% direct sku overlap with Amazon.com. However, assuming a 100% overlap in generic categories, the overlap was 93%. As a result of exclusive brands sold throughout various categories in Bed Bath & Beyond stores, certain product categories (i.e towels) had a 0% sku overlap. In reality, consumers are more sensitive to branded purchases in categories like cookware and appliances but neutral when shopping for items such as towels and sheets - a white towel is a white towel. As such, it’s important to keep the sensitivity of the overlap in perspective.

Matthew Darula

Analyst