This note was originally published at 8am on March 21, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Simple question: are we making sufficient progress to believe that our original strategic hypothesis is correct?”

-Eric Ries

I’ve been on the road for the last three days in Canada and Minnesota and had an opportunity to finish reading a book that our engineering team recommended by Eric Ries’, “The Lean Startup.” That quote comes from Chapter 8 which is titled Pivot (Or Persevere). Solid risk management read.

Solid is as solid does. Whether you are building your own company, nurturing a family, or serving as a fiduciary of other people’s money, you constantly have to Re-think, Re-work, and Re-build what isn’t working. If you are challenging yourself to evolve, you are going to break things.

What do you do when fundamental operating principles like trust break? Do you get out there and earn it back? Or do you sit there and make excuses? I thought UBS Chairman Kaspar Villager nailed it yesterday when he said this about trust:

“it cannot be tied to a far-dated founding year; trust has to be constantly won anew… reputation is the most important capital for a bank. It takes just a thoughtless action to lose it and the sweat of thousands to rebuilt it.”

If that doesn’t resonate with you, try playing on a Championship Team that sits facing one another in a 4-walled dressing room.

Back to the Global Macro Grind…

I’m not going to apologize for using sports analogies and/or team building concepts. That’s who I am – and I take great pride in working alongside teammates who think about the name on the front of their jersey before the one on their backs.

The leadership concept of Pivot (or Persevere) is a critical one in Global Macro Risk Management inasmuch as it is one in building a business. You really need to be Duration Agnostic when considering whether or not your strategic hypothesis is correct. Markets wait for no one and you’re constantly getting real-time feedback on the validity of your research views.

That’s why we’ve separated our process into two really big components:

- The Fundamental Research Process (Growth, Inflation, Policy, etc.)

- The Quantitative Risk Management Process (Price, Volume, Volatility, etc.)

Quite frequently these 2 components disagree with each-other. Usually that’s because they aren’t both speaking to you on the same duration. That’s why, contrary to popular efficient market hypothesis belief, Timing Matters.

As of 6AM EST today, here are our summary Fundamental Research Process updates:

- GROWTH: on our intermediate-term TREND duration, both globally and domestically, it’s slowing

- INFLATION: on our intermediate-term TREND duration, it’s rising

- POLICY: with the exception of very few countries (Iceland raised rates this morning), the Keynesian Bubble remains

From a Quantitative Processing perspective:

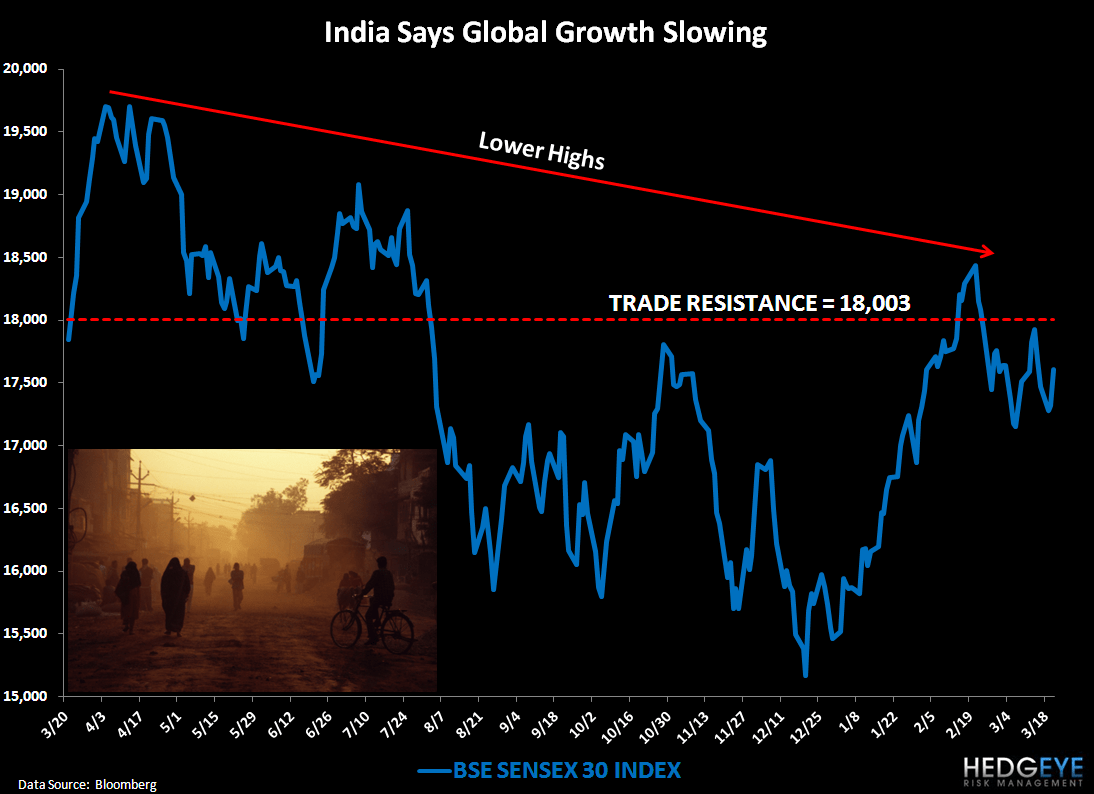

- PRICE: US and German Equities remain in Bullish Formations whereas China, India, and Hong Kong have broken TRADE lines

- VOLUME: Asian Equity volumes are ok, whereas US Equity Volumes continue to hit generational lows

- VOLATILITY: everything big beta (Inflation Policy stocks, commodities, etc.) is pseudo normal; SP500 VIX is bombed out

So what do I do with that?

Like I did in Q1 of 2008, 2010, and 2011, I sell beta (anything that’s eventually going to fall hostage to Growth Slowing, globally, in the intermediate-term). That doesn’t mean I wasn’t early in any of those prior Q1 Selling Opportunity periods. That doesn’t mean I’m not wrong right now being short the SP500 either (the position is -0.37% against me).

It just means I have plenty of room to improve my timing process.

Pivot Points (like intermediate-term tops and bottoms), are processes, not points. Every hour of every day we are offered more Fundamental Research points that can help proactively predict the changing slopes of the lines embedded in market expectations.

Market expectations, unfortunately, aren’t wrapped up in a pretty baby blue fundamental research box with a white bow. They fully factor in greed, fear, and performance chasing. They can be jubilant; they can be abrupt. And they have a not so funny way of surprising the most amount of people at the most unexpected times.

Who would have thunk that the SP500 would be down -10.2% from those topping process days of 2007 (you still need to be up over 12% from here to break-even by the way)? Are they the same people who nailed the SP500 being up +11.7% for 2012 YTD?

I don’t know. And I think that if you really want to capture the big intermediate-term Pivot Points of market prices, you really need to embrace the uncertainty of that three word statement.

My immediate-term support and resistance ranges for Gold, Oil (WTIC), US Dollar Index, and the SP500 are now $1627-1679, $105.70-108.91, $79.33-79.87, and 1391-1411, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer