No Current Position in Europe

We expect both the ECB (on Wednesday) and BoE (on Thursday) to keep their main interest rates on hold at 1.0% and 0.5%, respectively, and not to add any major non-standard measures or asset purchases. We expect both banks to continue implementing a “wait-and-see” process to determine the impact of policy moves, including the LTROs, reduced collateral requirements, and reduced SMP sovereign bond purchases in the last two months by the ECB and increases in the BOE’s asset purchasing program (increased purchases by £50 Billion on 2/9 and remained unchanged on 3/8).

Below we present our quantitative views on the EUR/USD and GBP/USD over the near term TRADE and intermediate term TREND.

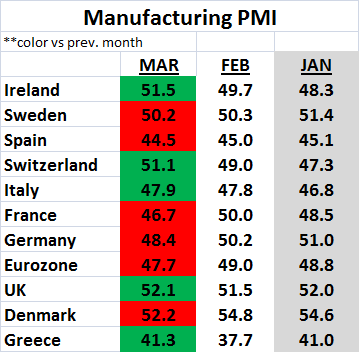

We continue to highlight that despite pockets of optimism on the Eurozone and UK economies, recent data continues to be weak. Yesterday we received European Manufacturing PMIs, which, as the table below shows, largely declined month-over-month in March (the UK saw a positive inflection), or were at or below the 50 line that divides contraction (below) from expansion (above). We expect a similar trend with European Services PMIs, which will be announced tomorrow.

Matthew Hedrick

Senior Analyst