“The current international currency system is the product of the past.”

-Chinese President Hu Jintao, January 2011

If Ben S. Bernanke thinks that he can continue to debauch the US Dollar and the rest of the world is going to say nothing this time, that will be different.

In James Rickards chapter titled “Prewar” of Currency Wars, he uses the aforementioned Chinese quote. It’s a year old now, but the East versus West policy waters are starting to boil. Since Commodity Inflation Slows Global Growth, many sharp minds are figuring this out.

Whether it’s the Reinhart & Rogoff Op-ed for Bloomberg this morning that tells the Fed to “stop moving the goal posts”, or it’s China’s Central Bank Governor Zhou telling the Fed it has a “responsibility to consider the global effects” of devaluing the world’s reserve currency, the battle lines are being drawn. Bernanke’s War is on.

Back to the Global Macro Grind…

It’s really easy for US centric stock market investors to not see what’s going on across the rest of the world right now. It requires a repeatable and globally interconnected Macro process to absorb all of the world’s real-time data. Few on the Old Wall have one. Even fewer Washington “economists” and “strategists” even know what that means.

Got un-awareness? In Currency Wars, Rickards hammers my point home in telling his story about a war games exercise he took part in that was sponsored by the Department of Defense: “I noticed the absence of representatives with any actual capital markets experience… we needed people who, in the immortal words of John Gutfreund, were “ready to bite the ass off of a bear”…” (page 9)

To be clear, I’d much rather dance with a bear than bite one.

Altogether though this is a very serious point that needs to be crystal clear in the minds of any American Patriot who regards the credibility of his or her currency as something worth fighting for. Cheering on a market that moves like it did yesterday (Down Dollar = Up Oil and Energy stocks) is effectively asking for $5 bucks at the pump come Memorial Day weekend.

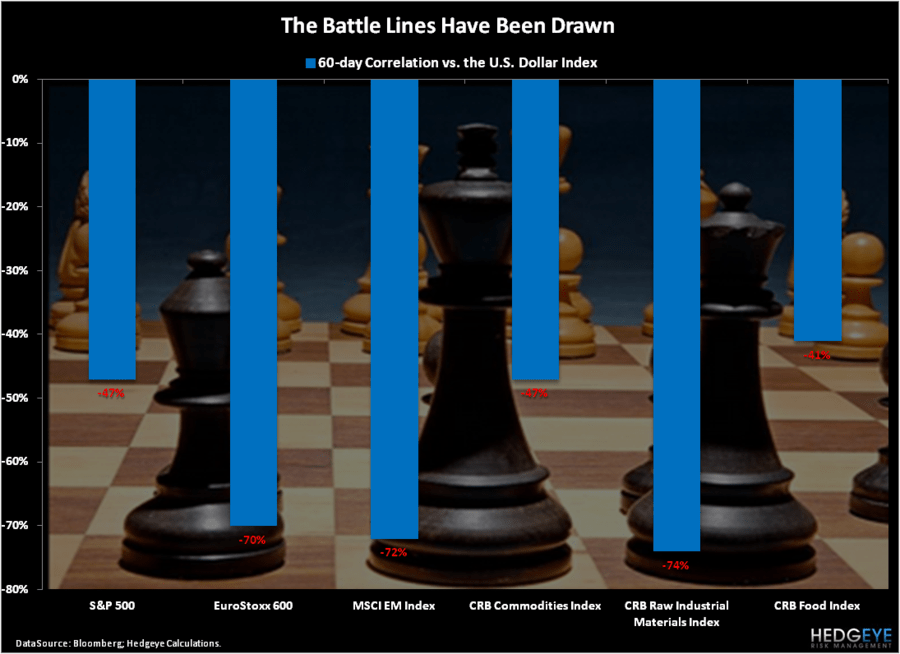

Taking a step back to Bernanke’s Dollar Debauchery Decision of 2012 (January 25th when, despite running 3% US GDP growth in Q4, he pushed the 0% rate of return on American Savings accounts to 2014), here are the 60-day correlations to the US Dollar Index:

- SP500 = -0.47

- EuroStoxx600 = -0.70

- MSCI EM Index = -0.72

- CRB Commodities Index = -0.47

- CRB Raw Industrials Index = -0.74

- CRB Food Index = -0.41

In other words, no matter what you think about correlation versus causality (I think the relationship between a country’s monetary policy and currency valuation is very causal), these are highly correlated moves.

Now, Bernanke or his banker buddy at the NY Fed, Bill Dudley (who also takes car service to work), might tell you to go eat an iPad or stick some natural gas in your tank – and like it. But the rest of the world doesn’t get paid that way.

The people who get paid are the few of us who have figured out that this Policy To Inflate is something to be long, until that very moment when it becomes obvious to everyone else that commodity inflation is slowing growth, again.

Again!

If Inflation from these food and energy price levels doesn’t slow growth – then why:

- Didn’t yesterday’s no-volume rally in US Stocks equate to higher bond yields? Treasury yields are down -3bps day/day

- Didn’t the rest of the world’s Equity markets open with a boom this morning? Italy chasing Spain lower now

- Didn’t Commodities continue to rock to the upside? Most of them are down this morning because the US Dollar isn’t

A: because world markets know (just as well as Bernanke should) that the US Dollar is being held, artificially, like a ball under-water.

How much longer can he hold the ball under water? How close does he have it to his face? What happens when that thing rips out of the water (like it has multiple times since he took over at the Fed), and deflates every asset price he’s trying to inflate?

I fear, my friends, that gravity is going to catch up with us when the least amount of us are positioned for it. Whether I am right on this or Reinhart, Rogoff, and the Chinese are doesn’t matter – it’s the when that will determine Bernanke’s legacy.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, and the SP500 are now $1, $121.94-126.12, $78.62-79.21, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer