TODAY’S S&P 500 SET-UP – April 3, 2012

As we look at today’s set up for the S&P 500, the range is 16 points or -0.92% downside to 1406 and 0.21% upside to 1422.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1516 (1043)

- VOLUME: NYSE 763.39 (-21.01%)

- VIX: 15.64 -0.90% YTD PERFORMANCE: -33.16%

- SPX PUT/CALL RATIO: 1.86 from 2.63 (-29.28%)

CREDIT/ECONOMIC MARKET LOOK:

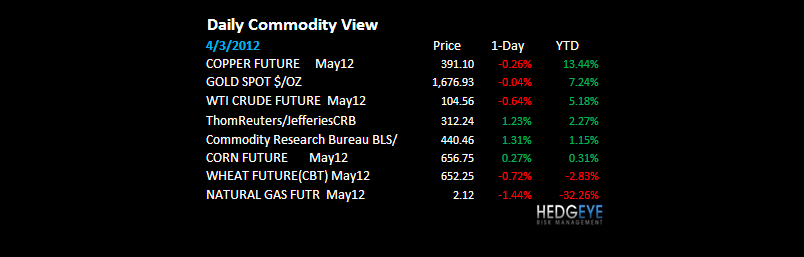

INFLATION – inflation slows growth. Yesterday’s US Equity move was led by Basic Material and Energy stocks + the CRB Index was up 2x what the SP500 was. The Bond market agrees. The 10yr and the Yield Spread (10s – 2s) wouldn’t be down 3bps for the wk to date if US growth was still 2.5-3%).

- TED SPREAD: 40.72

- 3-MONTH T-BILL YIELD: 0.07%

- 10-Year: 2.17 from 2.18

- YIELD CURVE: 1.84 from 1.86

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 9:45am: ISM New York, Mar., (prior 63.1)

- 10am: Factory Orders, Feb., est. 1.5% (prior -1.0%)

- 11:30am, U.S. to sell 4-week, $26b 52-week bills

- 2pm: Minutes of FOMC March 13 meeting released

- 4:05pm: Fed’s Williams participates in university symposium simulating FOMC meeting in San Diego

- 4:30pm: API weekly inventories

GOVERNMENT:

- Republicans hold presidential primaries in Wisconsin, Maryland, Washington, D.C.

- EIA Acting administrator Howard Gruenspecht speaks about gasoline supplies. 9:15am

- President Obama addresses Associated Press’s annual convention. Noon

- Treasury Secretary Timothy Geithner presides over FSOC mtg, vote on final rule regulating non-bank financial firms. 2:30pm

- Vice President Joe Biden answers questions via Twitter on college affordability. 3:45pm

- House, Senate not in session

WHAT TO WATCH:

- U.S. auto sales released today; March light-vehicle sales may have climbed to 14.5m seasonally adjusted annual rate; analysts

- Carl Icahn’s tender offer to acquire CVR Energy expired yday; Icahn said he wouldn’t extend unless 36% shrs tendered

- U.S. factory orders may have risen 1.5% in Feb., rebounding from a drop

- China eco. may have expanded ~8.4% in 1Q, the least since 1H of 2009, according to an est. given by an official 10 days before the data are due

- European producer prices rose 3.6% in yr, ahead of est. 3.5%

- Royal Bank of Canada sued by U.S. regulators over claims engaged in illegal futures trades worth hundreds of millions of dollars to garner tax benefits tied to equities

- Coty said to flip from seller to Avon buyer; yesterday went public with $10b offer that was rejected

- Cablevision accused NY Daily News publisher Mort Zuckerman of “a campaign of intimidation and extortion” to bring about a merger with Cablevision’s Newsday

- U.S. sales of repossessed properties probably will rise 25% this yr from 1m in 2011: Moody’s Analytics

- Olympus said it received capital alliance offers from Sony, Fujifilm Holdings and Terumo, may decide by next month

- IATA says outlook “fragile,” raises concerns about business travel growth

- Analyst says Roche to hold meeting this morning in New York after Illumina rejects offer

- Amazon.com is testing a service that lets tablet users make purchases through mobile applications

- SecondMarket said to hold its final auction of Facebook shares

EARNINGS:

- International Speedway (ISCA) 7am, $0.39

- Comverse Technology (CMVT) 7:30am, $0.17

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Arabica Premium Seen Higher on Robusta Supply Surge: Commodities

- Copper Retreats 0.6% to $8,590 a Ton on London Metal Exchange

- Copper May Drop as Higher Inventories Undermine Demand Outlook

- Oil Drops After Biggest Gain in Six Weeks on Outlook for Supply

- Palm Oil Rallies to One-Year High on Soybean Planting Concerns

- Gold May Fall in London on Concern Physical Buying Is Slowing

- Wheat Drops as Global Crop Prospects Improve; Corn Increases

- Sugar Falls in London for Second Day on Surplus; Cocoa Declines

- Australia LNG Boom Threatened by U.S. Shale Exporters: Energy

- India May Remain a Net Sugar Exporter for Third Year

- Fortescue’s Power Says China Steel Demand Will Be ‘Very Strong’

- Rusal Would Study Norilsk Sale at Right Price, New Chairman Says

- Pakistan Exchange to Begin Foreign-Currency Futures by June

- Tanker Rates Seen Reversing Rally as Oil Glut Expands: Freight

- Oil Drops After Biggest Gain in Six Weeks

- Oil Supplies Rise to Seven-Month High in Survey: Energy Markets

- Jewelers in India Extend Strike for 18th Day Over Higher Taxes

CURRENCIES

EUROPEAN MARKETS

ITALY – joins Spain this morning as the 2nd major Global Macro Equity market to snap its intermediate-term TREND line (15,961 was TREND support for the MIB Index). On a no volume rally in US Equities (down -17% vs my intermediate-term TREND avg yesterday), do not forget how bad those European PMI prints for March were yesterday.

ASIAN MARKETS

CHINA – explicit comments from Chinese central bank head Zhou this morning telling the Fed that Bernanke has a “responsibility to consider global effects” of its dollar debauchery policy. We called this Bernanke’s War last week and from a Global Macro perspective, it’s on. Japan just printed its lowest money supply number in 3yrs. Japanese Liquidity drying up.

MIDDLE EAST

The Hedgeye Macro Team