No Current Positions in Europe

Asset Class Performance:

- Equities: The EuroStoxx50 closed down -1.9% week-over-week vs -3.2% last week. Bottom performers: Russia (MICEX) -4.6%; Finland -3.5%; Italy -3.5%; Sweden -3.5%; France -3.3%. Top performers: Greece 1.0%; Portugal 70bps; Slovakia 10bps.

- FX: The EUR/USD is up +0.52% week-over-week. W/W Divergences: SEK/EUR +1.26%, NOK/EUR +0.59%, GBP/EUR +0.29%, CHF/EUR +0.09%; RUB/EUR -0.77%, CZK/EUR -0.75%, ISK/EUR -0.74%.

- Fixed Income: Greek 10YR yields gained +100 bps to 21.04% week-over-week after a rise of +192bps last week. 10YR Portuguese yields dropped the most, -126bps to 11.40%, while most other countries we track were broadly flat.

Call Outs:

Germany - Chancellor Merkel’s party won a regional ballot in the western state of Saarland, the first electoral test of her crisis-fighting policy since she persuaded European leaders into a pact to limit budget deficits. [Federal elections due in 2013].

Greece - In comments to privately-owned television station Antenna, Greek Government spokesman Pantelis Kapsis confirmed three possible dates on which the country is widely expected to hold national elections: April 29, May 6, or May 13 ("It will be one of these three Sundays," he said).

Ireland - The Government said a referendum on the EU’s new fiscal treaty will be held on May 31. Formally starting a campaign to persuade voters to back the compact or risk exclusion from access to future bailout funds.

UK - The economy shrinks more than previously estimated (Q4 GDP Q/Q -0.3% vs -0.2 estimate).

UK - Is in talks to sell as much as a third of its RBS stake to Abu Dhabi.

In Review:

Book ends. The week started with increased fears that Spain is the next domino to fall after Italy’s PM Mario Monti responded in a Q&A session at a conference that “it doesn’t take much to recreate risks of contagion.” While he praised Spain’s efforts to loosen work regulations, he advised Spain to focus on cutting the national budget, saying it “hasn’t paid enough attention to its public accounts.” Meanwhile, the market waited around for today’s decision (and seemingly liked it as European equities shot up 1%), on the structure of a combined ESM and EFSF bailout facilities and Spanish PM Rajoy’s 2012 Budget announcement.

The unnerving part remains days like today when equities (and EUR/USD) are rising despite underlying imbalances that are far from corrected, understood, or revealing an improving trend. After all, there is to be no increase in the combined size of the bailout fund, ESM (€500B) + EFSF (€240B existing) + €50-60B of addition loans, and it’s laughable to think that Spain will reach its deficit target of 5.3% of GDP this year versus 8.5%, along with the issue of Portugal requiring (another) bailout. Are we really out of the clear on the sovereign and banking sides because of two rounds of LTRO?

In between the events we continue to just hear a lot of “chatter” (including Monti back pedaling his statement on Spain this week) from leading Eurocrats and commentators that demonstrated: 1. How little Eurocrats understand about the severity of the region’s sovereign imbalances, 2.) the extent to which Eurocrats are saving face for their own job security, 3.) how uncertain Eurocrats are on future policy measures to shore up fiscal risks, reset expectations, sustain a union, and 4.) a combination of all of the above.

Here are some notable comments this week:

- Draghi sees signs of stabilization in economic activity and bank lending

- Draghi says Ireland and Portugal programs are on track, Spain showing progress “to some extent”

- Merkel says that it would be a huge political mistake if Greece was allowed to leave the Euro

- IMF sees improvements in global outlook but severe downside risks remain (Deputy MD Shinoha)

- Mario Monti says Eurozone crisis is almost over, Italy has helped stop crisis from getting worse

- Risk of a Spanish debt restructuring is higher now than it's been since the beginning of the crisis, said Citigroup Inc. chief economist William Buiter

What comes out in the wash is an unwillingness to turn the dial on years of fiscal excess. This “New Reality”, or “New Normal”, as PIMCO’s Gross has called it, is not fun, sexy, or easy. It means real pain for real people (see strikes and riots on the streets in Spain this week), and there’s no alternative? Spending your way out of a crisis doesn’t work. After all, it was this spending over the last decade that got these nations into the fiscal gutter. Sky-high unemployment rates across the PIIGS nations won’t recede over night. Countries like Portugal and Greece, for example, must figure out ways to increase competitiveness and grow their economies. As an example, over the last 10 years, Portugal’s GDP has averaged an annual -0.5%! What’s clear is that if the Eurozone project is going to work in the long run, we’re likely to see it at the hand of subsidization of the weak countries by the strong, and an acceptance of The New Normal standard of living and consuming (or at least uneven wealth across countries). However, a persistent headwind for Eurocrats will be managing this union around the underlying challenges of one common currency and one monetary policy, which we think is inherently flawed.

From the “Data Dump” below we want to point out that March fundamentals continue to be challenged. The five Eurozone confidence surveys all ticked down month-over-month, following on weak March Services and Manufacturing PMI numbers for the Eurozone, an unemployment rate of 10.7%, and CPI holding steady above the 2% target.

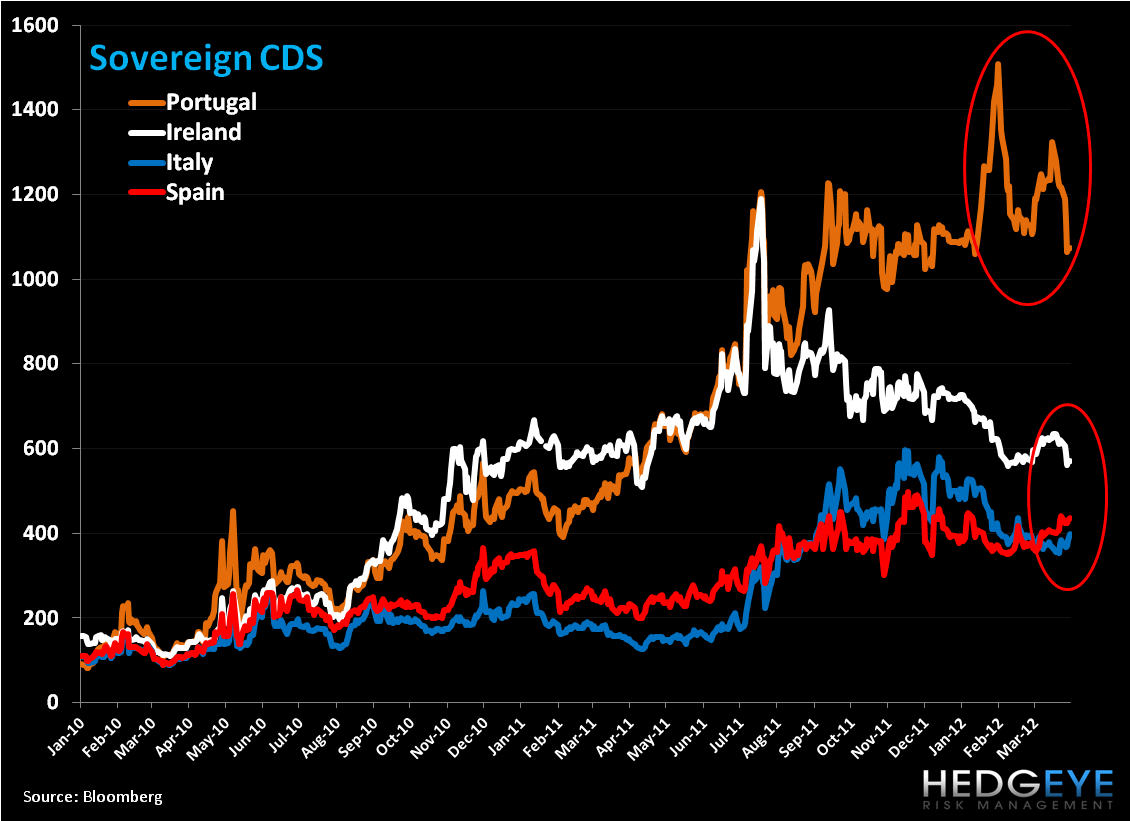

CDS Risk Monitor:

CDS fell -143bps to 1,074bps in Portugal on a w/w basis after a -94bps move last week, to lead decliners. Ireland fell -47bps to 570bps. Like sovereign yields, we did not see large moves on a week-over-week basis for the countries we track. Italy led gainers at +13bps to 397bps.

Data Dump:

Eurozone Business Climate -0.30 MAR (exp. -0.16) vs -0.16 FEB

Eurozone Consumer Confidence -19.1 MAR (exp. -19.0) vs -19 FEB

Eurozone Economic Confidence 94.4 MAR (exp. 94.5) vs 94.5 FEB

Eurozone Industrial Confidence -7.2 MAR (exp. -5.8) vs -5.7 FEB

Eurozone Services Confidence -0.3 MAR (exp. -0.8) vs -0.9 FEB

Eurozone M3 2.8% FEB Y/Y (exp. 2.4%) vs 2.5% JAN [3M AVG = 2.3% FEB Y/Y vs 2.0% JAN]

Eurozone CPI Estimate 2.6% MAR Y/Y (exp. 2.5%) vs 2.7% FEB

Germany GfK Consumer Confidence 5.9 APR (exp. 6) vs 6 MAR

Germany IFO Business Climate 109.8 MAR (exp. 109.6) vs 109.7

Germany IFO Current Assessment 117.4 MAR (exp. 117) vs 117.4 FEB

Germany IFO Expectations 102.7 MAR (exp. 102.6) vs 102.4 FEB

Germany Import Price Index 1% FEB M/M (exp. 0.9%) vs 1.3% JAN

Germany CPI 2.3% MAR Prelim Y/Y (exp. 2.3%) vs 2.5% FEB

Germany Unemployment Rate 6.7% MAR (20yr low) (exp. 6.8%) vs 6.8% FEB

Germany Unemployment Chg -18K MAR (to 2.84 million) vs -3K FEB

Germany Retail Sales 1.7% FEB Y/Y (exp. 0.1%) vs 1.7% JAN [-1.1% FEB M/M (exp 1.1%) vs -1.2%]

France Consumer Confidence Indicator 87 MAR (exp. 82) vs 82 FEB

France Q4 GDP Final 0.2% Q/Q = UNCH vs prev. est [1.3% Y/Y = down 10bps vs prev. est.]

France Producer Prices 4.3% FEB Y/Y (exp. 4%) vs 4.3% JAN

Italy Consumer Confidence 96.8 MAR (exp. 93.5) vs 94.4 FEB

Italy PPI 3.2% FEB Y/Y (exp. 3.3%) vs 3.5% JAN [0.4% FEB M/M vs 0.8%]

Italy CPI 3.8% MAR Prelim Y/Y (exp. 3.3%) vs 3.4% FEB

Italy Hourly Wages 1.4% FEB Y/Y vs 1.4% JAN

UK Q4 GDP Final -0.3% Q/Q = down -10bps vs prev. est.

UK Total Business Investment 1.6% in Q4 Y/Y vs 6.6% in Q3

UK Nationwide House Prices -1.0% MAR M/M (exp. 0.2%) vs 0.4% FEB [-0.9% MAR Y/Y (inline) vs 0.9% FEB]

UK M4 Money Supply -3.4% FEB Y/Y vs -1.8% JAN

UK Mortgage Approvals 49K FEB (exp. 57.2K) vs 57.9K

Spain Housing Permits -25% JAN Y/Y vs -27.9% DEC

Spain Mortgages on Houses -41.3% JAN Y/Y vs -37.2% DEC

Spain CPI 1.8% MAR Prelim. Y/Y (inline) vs 1.9% FEB

Spain Retail Sales -3.4% FEB Y/Y vs -4.6% JAN

Switzerland UBS Consumption Indicator 0.87 FEB vs 0.93 JAN

Switzerland KOF Swiss Leading Indicator 0.08 MAR vs -0.11 FEB

Sweden Retail Sales 3.4% FEB Y/Y (exp. 1.6%) vs 1.6% JAN

Sweden Household Lending 5% FEB Y/Y (exp. 5%) vs 5.1% JAN

Sweden PPI 0.5% FEB Y/Y (exp. 0.3%) vs 0.1% JAN

Sweden Consumer Confidence 0 MAR (exp. -2.1) vs -3.2 FEB

Sweden Manufacturing Confidence 1 MAR (exp. -11%) vs -13 FEB

Sweden Economic Tendency Survey 101.8 MAR (exp. 94) vs 93.4 FEB

Ireland Property Prices M/M -2.2% FEB vs -1.9% JAN [-17.8% FEB Y/Y vs -17.4% JAN]

Norway Unemployment Rate 2.6% MAR vs 2.7% FEB

Finland Business Confidence -4 MAR (exp. -2) vs -2 FEB

Finland Consumer Confidence 8 MAR (exp. 10) vs 8.3 FEB

Belgium CPI 3.37% MAR Y/Y vs 3.66% FEB

Portugal Consumer Confidence -54.5 MAR vs -55.8 FEB

Portugal Economic Climate Indicator -4.8 MAR vs -4.9 FEB

Portugal Industrial Production -6,8% FEB Y/Y vs -5.4% JAN

Portugal Retail Sales -8.9% FEB Y/Y vs -7.8% JAN

Hungary Unemployment Rate 11.6% FEB vs 11.1% JAN

Slovakia Consumer Confidence -32.3 MAR vs -32.5 FEB

Slovakia Industrial Confidence 3 MAR vs -1.3 FEB

Lithuania Consumer Confidence -21 MAR vs -23 FEB

Interest Rate Decisions:

(3/27) Turkey Benchmark Repo Rate UNCH at 5.75%

(3/27) Hungary Base Rate UNCH at 7.00%

(3/29) Romania Interest Rate CUT 25bps to 5.25%

(3/29) Czech Repo Rate UNCH at 0.75%

The European Week Ahead:

Friday/Saturday: Eurozone Financial Ministers and Central Bankers will meet in Copenhagen to discuss strengthening the region's firewall

Sunday: Mar. UK Lloyds Business Barometer, Hometrack Housing Survey

Monday: Mar. Eurozone, Germany, and France PMI Manufacturing - Final; Feb. Eurozone Unemployment Rate; Mar. UK, Italy, and Greece PMI Manufacturing; 4Q UK BoE Housing Equity Withdrawal; 4Q Italy Unemployment Rate, Budget Balance; Feb. Italy Unemployment Rate - Preliminary

Tuesday: Feb. Eurozone PPI; Mar. UK PMI Construction, BRC Shop Price Index; Mar. Spain Unemployment MoM

Wednesday: ECB Policy Meeting/Announces Interest Rates; Mar. Eurozone PMI Composite and Services - Final; Feb. Eurozone Retail Sales; Mar. Germany and France PMI Services - Final; Feb. Germany Factory Orders; Mar. UK, Italy, and Spain PMI Services; Mar. UK Official Reserves; 4Q Italy Deficit to GDP

Thursday: Feb. Germany Industrial Production; BoE Announces Rates; Apr. UK BoE Asset Purchase Target; Mar. UK NIESR GDP Estimate; Feb. UK Industrial and Manufacturing Production

Friday: Feb. France Central Government Balance, Trade Balance

Extended Calendar Call-Outs:

22 April: French Elections (Round 1) begins, to conclude in May.

29 April, 6 or, 13 May: Potential Greek Presidential Elections.

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst