This morning Keith added a short position in Freeport-McMoRan (FCX) in the Hedgeye Virtual Portfolio at $37.54.

We like FCX on the short side right now because it plays off two of our key macro calls – Global Growth Slowing and Bullish US Dollar.

FCX is the world’s second-largest copper miner. Every $0.10/lb change in the price of copper equates to +/- $380MM in annual EBITDA for FCX (on a base of $8.9B in annual EBITDA). We think that demand for copper, as well its price, will decline alongside the slowdown in global growth. On our quantitative model, copper is broken from an immediate-term TRADE perspective with resistance at $3.85/lb. Shares of FCX and the spot price of copper have between a +0.50 and +0.65 correlation on every duration between three months and three years.

While FCX is the beneficiary of a stronger USD on its income statement due to foreign currency translation, a break-out in the USD is a net negative for FCX, as the prices of copper and gold are strongly inversely correlated to the dollar. Over the past year, copper and gold have had inverse correlations with the USD of -0.70 and 0-.79, respectively.

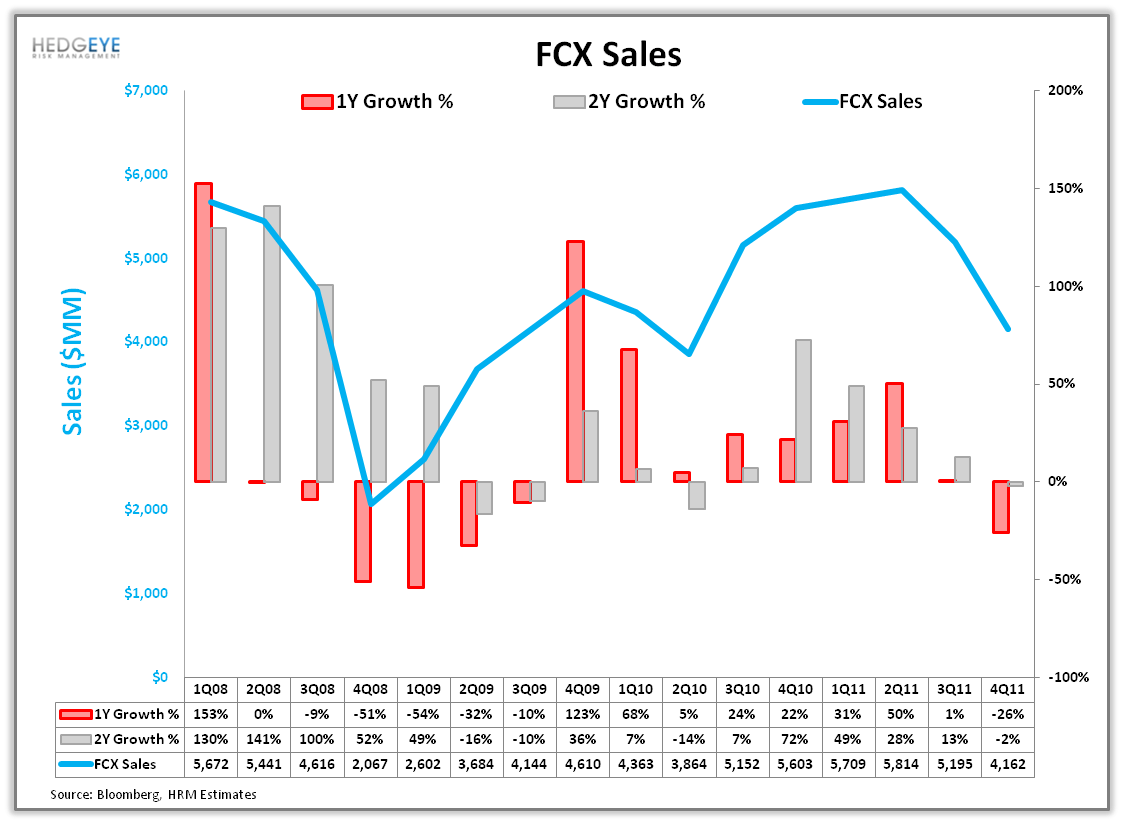

The macro back drop is negative, and FCX’s 2012 fundamentals do not look better. Contrary to popular opinion, FCX is not “cheap” at 4X EV/2012 consensus EBITDA. Notwithstanding the fact that consensus EBITDA is wrong if copper prices go down, we project that FCX will put up negative top line growth in 2012 versus +9% in 2011, and gross margins are contracting rapidly, down 2200 bps YoY to 36% in 4Q11. A super-cyclical like FCX gets a lower multiple when the top line is slowing and margins are contracting (see Charts 1 and 2 below).

FXC screens well as a short on our sentiment model. The sell-side is bullish with 21 buys, 4 holds, and 0 sells despite negative revenue and earnings estimates over the last six months (top line revised 9% lower, EPS revised 21% lower). And with only 2% short interest, there is little risk of this being a consensus idea or the stock squeezing higher.

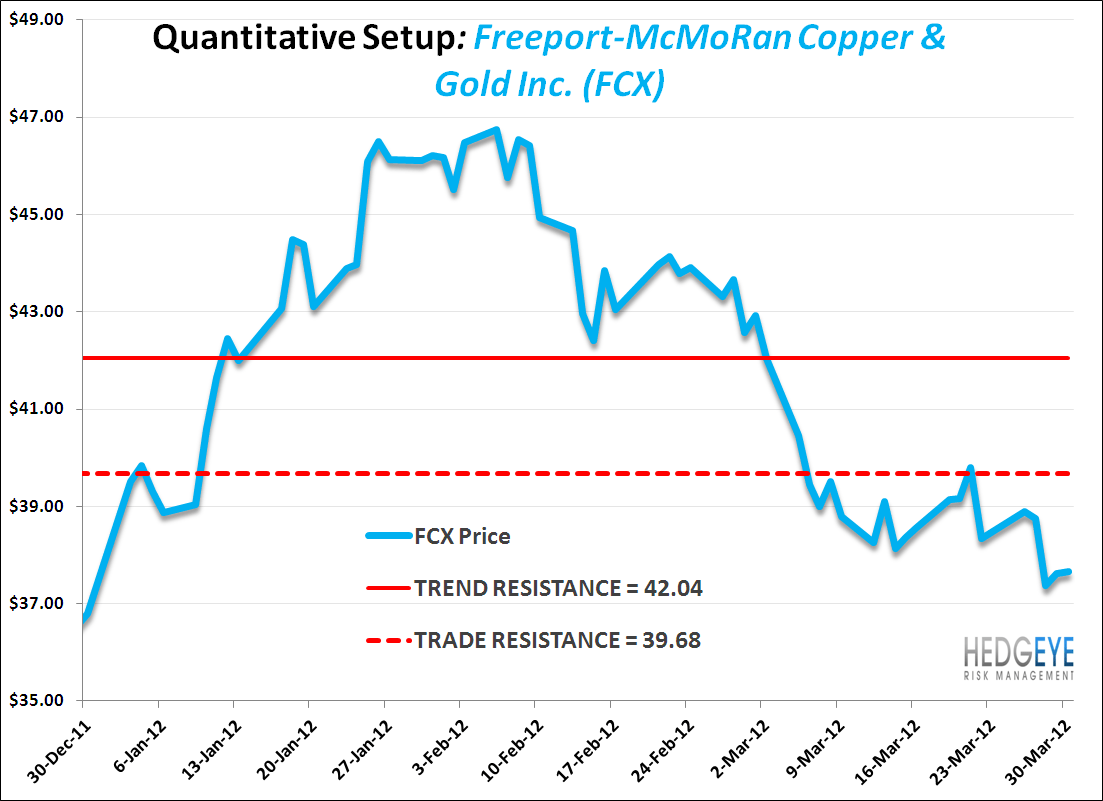

Per our Macro Team’s quantitative model, FXC is bearish on the TRADE and TREND durations with resistance at $39.68 and $42.04, respectively.

Kevin Kaiser

Analyst