Here’s a solid overview of BBBY by my colleague Matt Darula.

BED, BATH & BEYOND: DURATION ANALYSIS

Conclusion: The consensus call on BBBY is clear. That it is a well-managed company, but one that will face increased pressure from dot.com given the commodity nature of its product. That said, the roadmap is quite opaque, and though there will be pressure, no one is sure how much is at risk, and when it will begin to really impact numbers. We think that’s probably right, but our conclusion is that we’re seeing a meaningful bifurcation in BBBY’s business across durations. Our Home Furnishings Indicator suggests that BBBY will surprise on the upside with comps, and as such we’re a nickel ahead on the quarter. But then we have a sharp deceleration in earnings growth next year due to increased commoditization due to a disrupted organization that is not prepared for the magnitude of stress on its core from new competition. We conducted a lengthy, and accurate, overlap analysis (see end of this note) to assess the damage. The result… 93% at risk. We’d be selling on a strong quarter.

Here’s Our View By Duration

TRADE: (Trade = 3 Weeks or Less)

BBBY Reports its fourth quarter and full year results April 4thafter the close. We expect fourth quarter earnings to be about a nickel ahead of consensus driven by a stronger than excepted 5% comp vs. 3.6%E (and guidance of 2-4%), partially offset by weaker margins from a more promotional holiday shopping season. Our home furnishings model has a 5 year correlation of 0.74 with BBBY comps. What’s notable is that this includes the period where BBBY was gaining share at the expense of Linens N Things. Excluding this gap, the relationship is even tighter. In maintaining the backtested spread, we’re looking at a comp of 5-6% out of BBBY. Earlier this month, WSM reported results that were in-line with original guidance – after they came out and preannounced a miss (that really never materialized). Lots of issues at WSM, and not a direct comp, we realize. But worth noting.

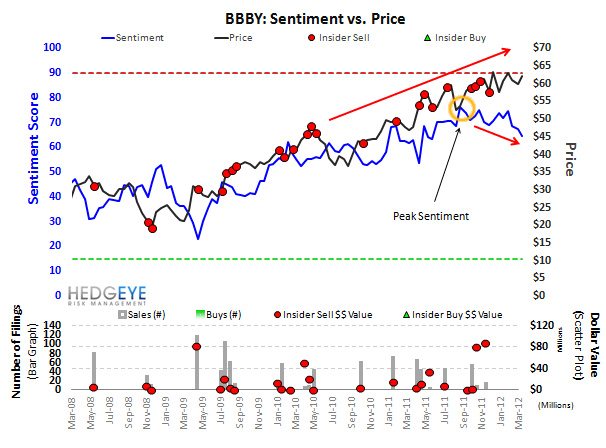

What’s notable is that our Sentiment Monitor has been rolling over as the stock hits all-time highs. We usually see the opposite. BBBY has 16 Buy ratings, 12 Holds and only 1 Sell. Short interest is sitting at about 3.2% of float, and while that seems low, it’s actually high for BBBY relative to its own history. The point is that over the past 5-months, BBBY lost 9 points on our Sentiment Indicator (i.e. people got less bullish) while the stock marched forward to the tune of 28%. Perhaps the market is looking for a beat. If so, no problem. It’ll get it. But if not, look out below. Two of the past three quarters have not had the greatest quality of earnings, and the price reactions have not been fun for the bulls.

TREND: (Trend=3 Months or less)

A Big risk factor that BBBY faces over the intermediate term is the relocation and consolidation of its Farmingdale and Garden City, NY headquarters to Union, New Jersey. Farmingdale and Garden City are each ~40-50 miles from Union. That’s certainly enough to dissuade some of the current corporate employees from moving including members of BBBY’s buying department. The company expects the move to be settled by the second half of F12.

Aside from ‘hiccup’ let’s acknowledge the risk inherent when a company with a culture that is as strong as BBBY simply ups its roots to another tax jurisdiction (for employees, not the company). Good people will be lost, and there will be important shoes to fill. Some of what made the culture here so great will be disrupted. There is an obvious cost element – that management highlights for us, but it’s tougher to quantify the intangibles, not the least of which is lost revenue and productivity.

TAIL: (Tail=3 Years or Less)

BBBY was the primary competitor that ‘nudged’ Linens n Things into Chapter 11 in 2008 alongside the recession and bursting housing bubble. After 3 years of shrinking operating asset turns and margins eroding, BBBY improved both in 2009 & 2010. While BBBY’s aggressive expansion and promotional cadence was largely the nail in the coffin for LIN, many people overlook the pressure from the e-commerce home category. Our analysis below shows that Bed Bath and Beyond has a 93% product overlap with Amazon.com which exposes BBBY’s primary store format (85% of the 1174 stores) to online competitive threat. In other words, it was not just BBBY that put LIN out of business, it was Amazon and other dot.com competition. Dot.com is still hungry, and with LIN’s $3.5bn in revenue gobbled up by BBBY ($10bn in revs), AMZN and the like, it will still go after bricks and mortar opportunities.

While alternative store formats like Christmas Tree shops and Buybuy Baby are less at risk, we expect the long-term tail risk to amass as the consumer focus shifts to omni-channel. BBBY has already begun to reaccelerate capital spending as a percent of sales on new stores, remodels, IT enhancements & a new fulfillment center but this might be too little too late. While this may increase customer retention, our concern here is that BBBY will need to spend more to stand still.

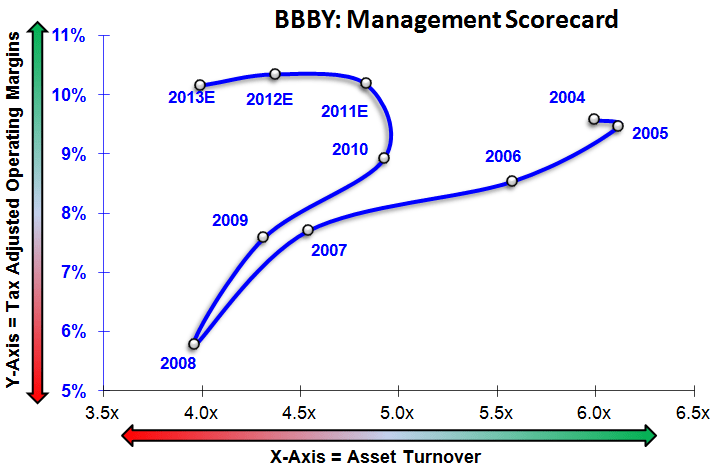

Check out our BBBY Management Scorecard

The BIG ideas in retail come when a company’s triangulation of EBIT margins and asset turns both improve simultaneously. Check out the chart below. The three years leading up to 2008 were abysmal. So was BBBY’s stock performance. From ’08 through ’11, we’ve got asset turns improving along with EBIT margins. That’s a big RNOA accelerator. Pretty simple. But once margins OR asset turns start to stall, then multiple expansion goes out the door. That’s where the TAIL call with this company is headed.

For the past three years, earnings growth has been near 30%. For the next three, we have it hovering in the single digits. Take a look at history, this company is not afraid to shrink its net income.

Product Overlap:

What we did: We conducted a detailed analysis on the different plan-o-grams in different sized Bed, Bath and Beyond stores. Then we looked at overlap among a variety of store formats. Then we literally scanned each product, and compared to either a) the exact product online, b) a ‘pretty darn close’ product by the same brand – one with enough tweaks for BBBY to call it exclusive, when its really close to being the same thing, and c) a competing product in a more commodity category that can act as a substitute.

Out of the product sold through Bed Bath & Beyond stores, our analysis showed there was a 52% direct sku overlap with Amazon.com. However, assuming a 100% overlap in generic categories, the overlap was 93%. As a result of exclusive brands sold throughout various categories in Bed Bath & Beyond stores, certain product categories (i.e towels) had a 0% sku overlap. In reality, consumers are more sensitive to branded purchases in categories like cookware and appliances but neutral when shopping for items such as towels and sheets - a white towel is a white towel. As such, it’s important to keep the sensitivity of the overlap in perspective.

Higher Ticket = Higher Risk:

Overall, Amazon.com’s pricing was ~1% less than Bed Bath & Beyond’s in store prices. This varied dramatically across each shop with Amazon’s pricing most competitive in the higher cost categories. As consumers shift their spending more and more online, the greatest risk in the home space will be realized first in higher ticket categories including small appliances, cookware & luggage. We realize it will take longer for consumers to purchase smaller ticket items like picture frames, table settings and basic kitchen needs online but as companies continue to offer free shipping and put a greater emphasis on the online shopping experience and browsing tools we expect this to change.

Bed Bath & Beyond/Amazon Product Overlap Methodology:

Our product overlap analysis pertains to the Bed Bath and Beyond concept only (993 of the current 1174 BBBY store fleet). Within the Bed Bath concept, the brick and mortar locations are primarily between 20K to 50K square feet with the sku count per store varying based on the size of each individual box as well as the market. We estimate that the sku count range in the Bed Bath and Beyond concept is between 10K-20K per store. BBBY’s primary concept has a distinctive merchandise presentation that is relatively homogenous across all stores and is designed to segment the store into more focused specialty “shops” that are used to channel the product offering by category. There are about 20-30 “shops” in each Bed Bath and Beyond store. The variability in “shops” across each location is another driver of overall sku count given the product density of each section. Most stores begin with the “Small Appliance,” “Kitchen Basics,” & “Cookware” sections which are relatively dense in sku count and end with the “Rugs” & “Towels” shops which house fewer skus. Conversely, less stores have a “Decorative Pillow” & “Luggage” section which are far less dense(see image below). We scanned ~150-200 skus per shop using the Amazon.com I-Phone app for overlap and price comparisons in 20 “shops” (spread across multiple locations) to estimate the online threat (~2500 skus overall).

Further driving the product offering in each store is the site manager selection - only 30% of the sku count in each store is fixed at a regional level with the remaining 70% selected by the store manager from a pre-established catalog to cater to the local market/consumer. While the 70% variability typically creates a differentiating product mix by “shop” in each location, the brands and categories remain consistent.

One unique quality that differentiates the Bed Bath & Beyond store format is the “walkthrough” layout that defines a start and end to the store and requires shoppers to pass each “shop” before hitting the register. Take a look at our store mockup below based on the Port Chester, NY store. This is one clear advantage to the concept given many trips to these stores that were originally intended for individual purchases can potentially be converted into a multi-item basket. This however can only happen as long as customers continue to shop the stores - once that single item purchase goes online the opportunity cost could be exponential.

The 93% overlap in Bed Bath & Beyond’s product offering with Amazon poses a risk that while fundamentally long term, will play out over time as the consumer gradually evolves into an omni-channel shopper and ultimately chooses to shop from the comforts of their living room.

Brian McGough

Matt Darula