TODAY’S S&P 500 SET-UP – March 29, 2012

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -900 (-393)

- VOLUME: NYSE 817.02 (11.88%)

- VIX: 15.47 -0.77% YTD PERFORMANCE: -33.89%

- SPX PUT/CALL RATIO: 3.16 from 2.25 (40.44%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 39.33

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.18 from 2.20

- YIELD CURVE: 1.84 from 1.86

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: GDP, 4Q T, est. 3.0% (prior 3.0%)

- 8:30am: Personal consumption, 4Q T, est. 2.1% (prior 2.1%)

- 8:30am: Jobless claims, March 24, est. 350k, prior 348k

- 9:45am: Bloomberg Consumer Comfort, March 25(prior -34.9)

- 10am: Freddie Mac 30-yr mortgage

- 10am: Fed’s Braunstein testifies on mobile payments

- 10:30am: Fed’s Lacker to speak on credit markets in N.C.

- 10:30am: EIA natural gas

- 11am: Kansas City Fed Manufacturing, March, est. 13, (prior 13)

- 12:15pm: Fed’s Lockhart speaks on global economy in Atlanta

- 12:45pm: Fed’s Bernanke gives lecture at George Washington U. (4 of 4)

- 1pm: U.S. to sell $29b 7-yr notes

- 1pm: Fed’s Plosser speaks on economic outlook in Wilmington, DE

- 6:45: Fed’s Lacker speaks to bankers in Charlotte, N.C.

GOVERNMENT:

- Senate plans to debate bill that would repeal tax breaks for big oil companies

- Lawmakers will seek an extension to a highway funding measure that expires Saturday

- CFTC holds a meeting of its advisory panel on automated and high-frequency trading. 10 am

- House, Senate in session:

- House Energy and Commerce Committee hears from FTC Chairman Jon Leibowitz on balancing privacy and innovation. 9am

- Senate Energy Committee holds hearing on gasoline prices. 9:30am

- House Financial Services Committee hears from CFPB Director Richard Cordray on the bureau’s semi-annual report. 9:30am

- Senate Government Affairs subcommittee holds hearing on how cost information is used to make decisions. 10am

- Senate Banking Committee votes on Fed Board of Governors nominees Jerome Powell and Jeremy Stein. 10am

- Senate Appropriations Committee hears from Agriculture Secretary Tom Vilsack on the agency’s budget. 2pm

WHAT TO WATCH:

- Best Buy releases 4Q results, probably will give yr forecast; watch 4Q gross margin

- Research in Motion releases first earnings under CEO Thorston Heins, having missed sales est. for four consecutive qtrs

- Roche raises hostile takeover offer for Illumina to ~$6.7b, or $51/share

- Express Scripts said to get FTC ruling as early as tomorrow on proposed Medco Health takeover

- Fed nominees Jerome Powell and Jeremy Stein face Senate Banking Committee vote

- Tata, Vodafone get extension to April 19 to decide on Cable & Wireless offer

- FDA advisers to recommend whether makers of new obesity drugs should be required to complete studies on heart risks

- Oil trading near lowest close in a week as Western countries discuss tapping emergency reserves

- Canadian finance minister releases his annual budget, 4pm

- Pearson CFO says FT newspaper is not for sale, co. seeking targets in India, Brazil and China

- SEC investigators said to review short-term VIX ETN from Credit Suisse that became unhinged from its benchmark

- Economic confidence in the euro region unexpectedly declined in March

- Greece may have to restructure debt again, S&P’s Kraemer says

EARNINGS:

- Sprott (SII CN) 7:00am, C$0.06

- Movado (MOV) 7:30am, $0.10 (1 est.)

- Shaw Group (SHAW) 8am, $0.45

- Best Buy (BBY) 8am, $2.15

- Worthington Industries (WOR) 8:15am, $0.35

- Cascade (CASC) 4pm, $1.09

- Forest City Enterprises (FCE/A) 4:02pm, $0.32

- Tibco Software (TIBX) 4:04pm, $0.19

- Research In Motion (RIM CN) 4:15pm, $0.81

- Finish Line (FINL) 4:40pm, $0.81

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Palladium Seen Beating Gold With Record Car Sales: Commodities

- Oil Falls Near One-Week Low on Stockpile Gain, Talk of Release

- Sugar Falls for Fifth Session on Surplus Prospects; Cocoa Drops

- Soybeans Rise as Demand for U.S. Crops May Strengthen on Drought

- Former UBS Executives Will Start London Commodities Hedge Fund

- China Buys Five Cargos U.S. of Corn, State Researcher Says

- Copper May Fall on Speculation of More Supplies; Nickel Declines

- Gold May Drop in London on U.S. Outlook, Weak Physical Demand

- Japanese Crude-Oil Imports From Iran Dropped 43% in February

- Commodity Holdings Expand as Volatility Drops: Chart of the Day

- Palm Oil Declines for Second Day as High Prices May Erode Demand

- Gold May Gain 8.5% on Moving Average, Hammer: Technical Analysis

- Runaway Gas Well Threatens Total Revival as Shares Slump: Energy

- Palladium May Beat Gold on Rising Demand

- China Cotton Demand to Recover, Lifting Prices, Weiqiao Says

- Vitol’s Taylor Says Atlantic Oil Refinery Closings Spur Shipping

- World-Leading Platinum, Rubber Stall on China: Chart of the Day

CURRENCIES

US DOLLAR – the USD went from up +0.25% at this hour yesterday (commodity inflation was deflating = good) to down -0.62% on the close. What changed intraday? Bernanke reminded the world of his conflicted and compromised policy to inflate. Fun while it lasts (if you’re long), but our strong sense is that the next stock/commodity market crash will be perpetuated by the bubble in Easy Money. There’s no one left to blame.

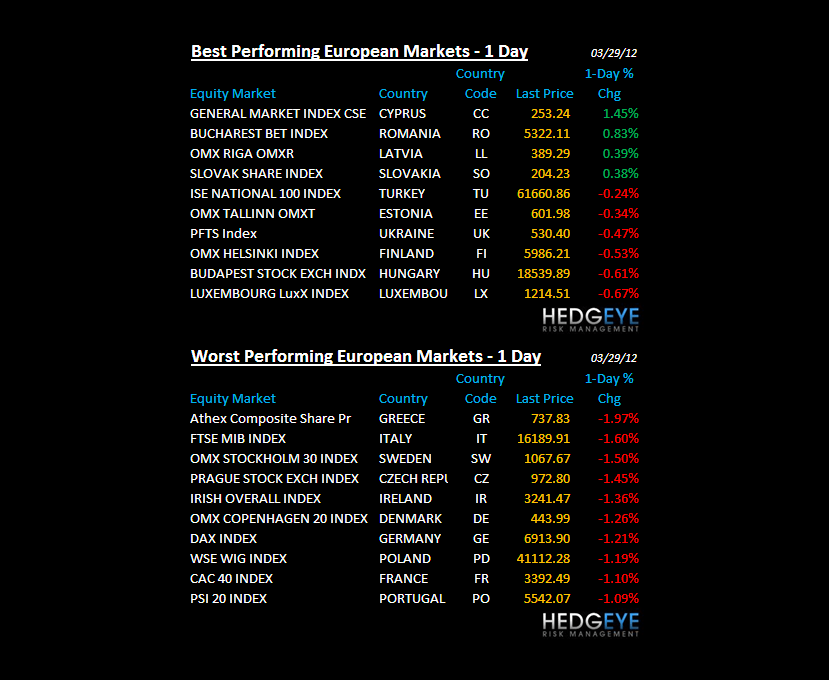

EUROPEAN MARKETS

SPAIN – rising bond yields and a down -3.4% stock market YTD finally manifesting into higher yields (sequentially) on the 6mth side of the Spanish bond auction. Major stagflation issues in the Spanish south perpetuating political issues for Rajoy as he attempts to implement an austerity budget.

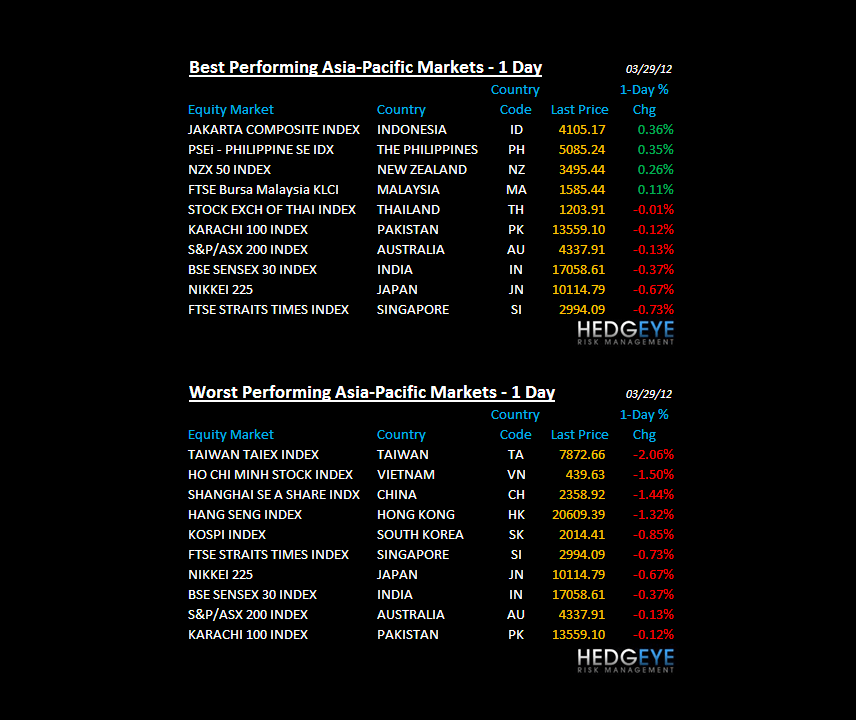

ASIAN MARKETS

CHINA – someone forgot to tell the Chinese to stop slowing; stocks in China closed down -0.15% overnight and India rallied +0.8% on no volume to another lower-high. Down Dollar/Up Oil (particularly Brent oil) is what keeps China and India from cutting rates here.

MIDDLE EAST

The Hedgeye Macro Team