Conclusion: We expect a solid quarter driven by robust February sales to finish out the quarter and believe that current trends suggest March is running ahead of expectations for Q1 as well.

TRADE (3-Weeks or Less):

We’re at $0.86 for FINL headed into Thursday’s print after the close ahead of Street estimates at $0.81E.

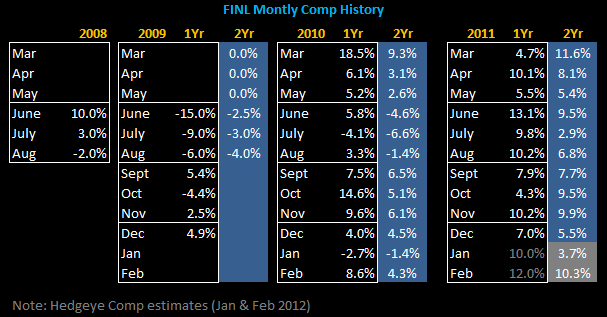

- February sales in the Athletic Specialty channel came in big up +17% increasing the quarterly average a full 4pts to +10.3% from +6.3%. Based on the Hedgeye FINL Comp index below, which has proven to be a strong indicator, we expect comps of +10% vs. +6.7%E to drive sales up +15.5% reflecting the 14thweek and ~$25mm in incremental sales.

- These results are even stronger than FL’s bullish commentary last month noting that February sales were up mid-teens month-to-date. This strength isn’t captured in consensus estimates.

- In addition, weekly sales suggest that March is running up HSD. While a sequential deceleration from February levels, this too is better than expectations and will be viewed favorably if confirmed as expected on the call.

- In light of a more robust top-line, we are modeling GMs up +150bps driven by +110bps in occupancy leverage and +40bps of merchandise margin and SG&A up +15% yy reflecting incremental e-commerce investment.

TREND (3-Months or More):

The company remains committed to investing in its digital platform, which has and will continue to drive higher than average SG&A growth for the next few quarters. This is a known, however, and is largely the reason why FINL has been trading at a discount relative to its historical range as well as to FL among other reasons. What’s changed here recently is the top-line. Sales are coming in stronger than expected helping to offset FINL’s higher costs. If this trend continues as we’ve seen since February, we could see upside to our $1.85 2012 estimates.

TAIL (3-Months or Less):

FINL is spending when it should to fuel its e-commerce business, which now accounts for ~10% of total sales. With 60% growth last quarter there is little question that this is a key growth engine. As investment spending rolls off and e-commerce grows in addition to further growth in its run specialty store initiative, we expect earnings to approach $2.20 in two years. At $25, will FINL make you rich? Probably not, but we're definitely positively inclined on the name here.

Casey Flavin

Director