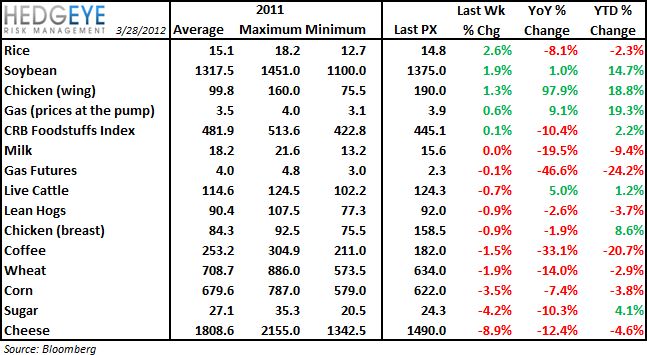

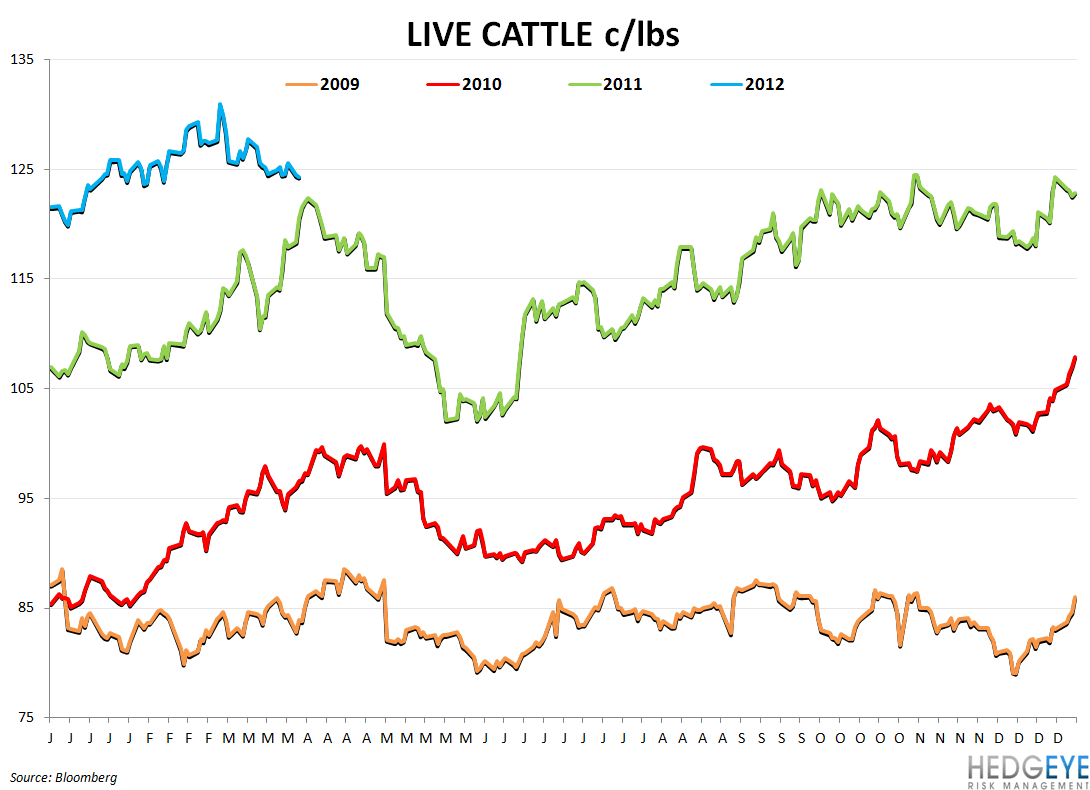

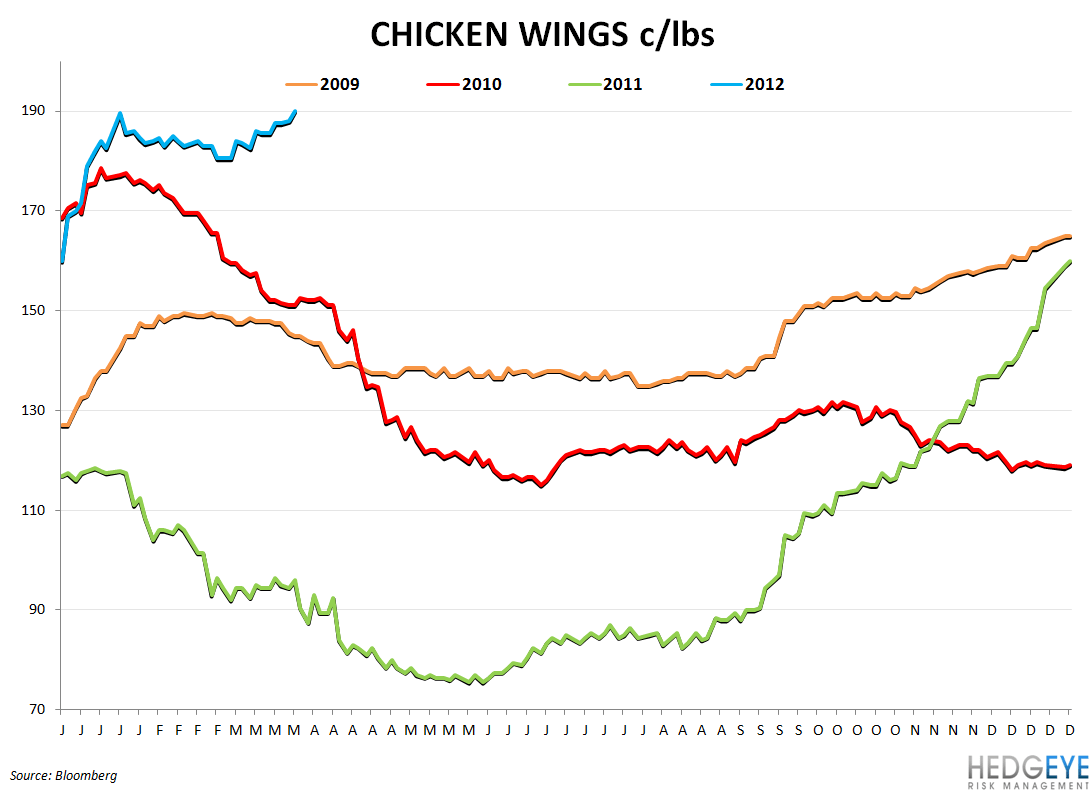

Despite dollar weakness over the past week, most agricultural commodities that we monitor declined week-over-week. Chicken wing prices continue to gain as leading indications of chicken supply and increasing demand for chicken from food service.

CONSUMER CALLOUT

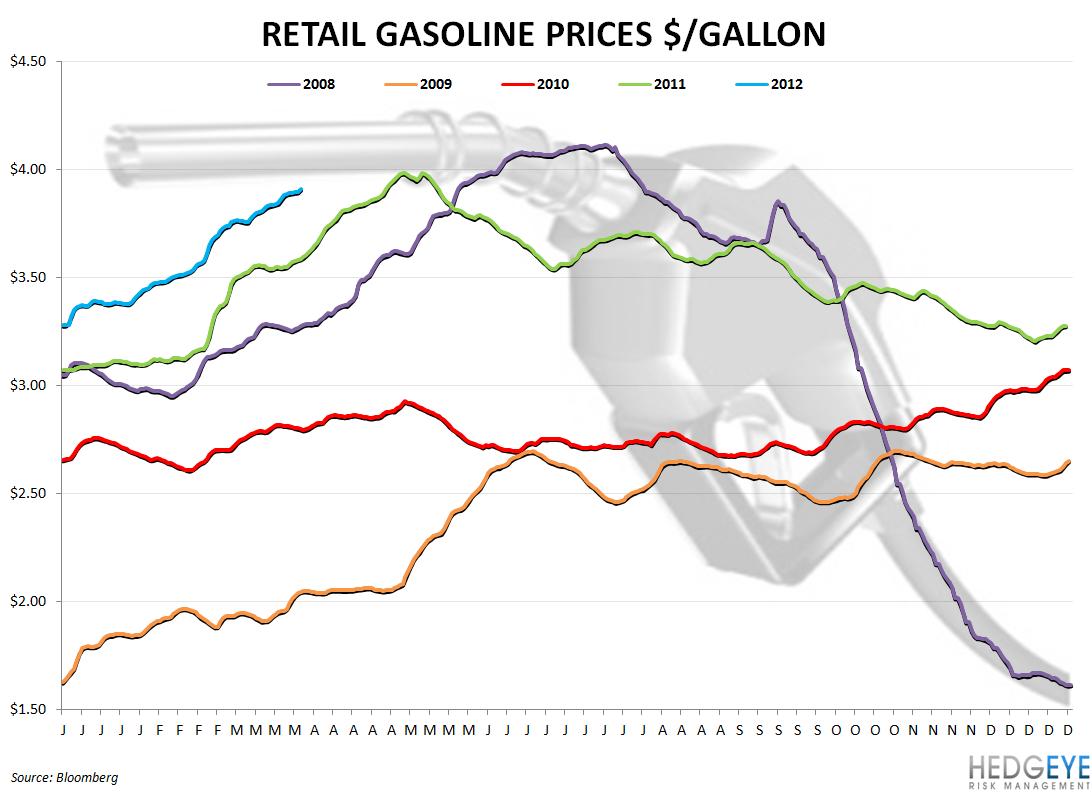

Gasoline prices continue to rise as Ben Bernanke’s recent commentary sent the dollar lower. Average national prices are now above $3.90 and consumers’ displeasure is increasingly apparent. Below, we present the most recent quotes from a select group of companies on the issue of gasoline prices. We expect, if the current trend continues, for the tone of these statements to change when each management team discusses gas prices again.

There have been two dueling schools of thought during the recent debate on gas prices that we feel are worth calling out. First, there seems to be a camp that has a fixed price such as $3.75 or $4.00 that is seen as the “rubicon” beyond which consumer demand is greatly impaired. Second, there is another group that proposed that it is the rate of change, rather than the dollar price, that impacts consumer spending. While we have a view on that debate, the important takeaway from the chart below is that there is ample evidence to suggest that a consensus can be reached; not only are gas prices closing in on $4, they have gotten there in an expedited fashion (+20% YTD, roughly).

WEN: Obviously, we're all watching gas prices carefully and – but consumers seem to quite honestly have digested that quite nicely.

BAGL: If employment continues to be positive, again from my perspective, I think that sort of offsets any impact that you might get – we might get on gas prices … That said, if employment tightens up or we don't see continuously positive momentum than longer-term, obviously, if we get a $5 gas price, that's one of those price points that hits overall.

CBRL: We think that given our susceptibility particularly to – in the summer travel season to potential increases in gasoline prices that it is appropriate to be suitably cautious about our third and fourth quarter traffic outlook.

DRI: Yes, I would say as we look back, we don't think the current levels, the $4 current gas prices, no longer represents sticker shock.

SUPPLY & DEMAND

Coffee

SUPPLY

Goldman released a note yesterday saying that coffee may gain in Brazil if weather remains dry in the country’s crop growing regions. German researcher, F.O. Licht GmBH, also said in a report that the main coffee growing areas in Brazil were “drier than usual” in February.

DEMAND

World coffee demand growth remains “resilient”, according to Roberio Silva, executive director of the London-based International Coffee Organization. Silva attributes the resilience to emerging market demand, increased consumption in producing countries, and the expanding popularity of single-cup dispensers.

Chicken

SUPPLY

Egg sets placements continue to contract at around the same rate, -6%, according to the Broiler Hatchery report released by the USDA today. This implies that supply will remain tight as the industry looks for more favorable business conditions before expanding production. As the chart below shows, supply is not showing any clear signs of picking up.

RECENT COMPANY COMMENTARY

Coffee: Prices are now down -24% versus last year

PEET: We expect 2012 coffee costs to rise 12% instead of last year's 42%.

SBUX: We've taken advantage of the recent declines in the C-price to lock in more of our coffee needs for fiscal 2013. We now have six months of our fiscal 2013 requirements secured at costs moderately favorable to 2012.

CORRELATION

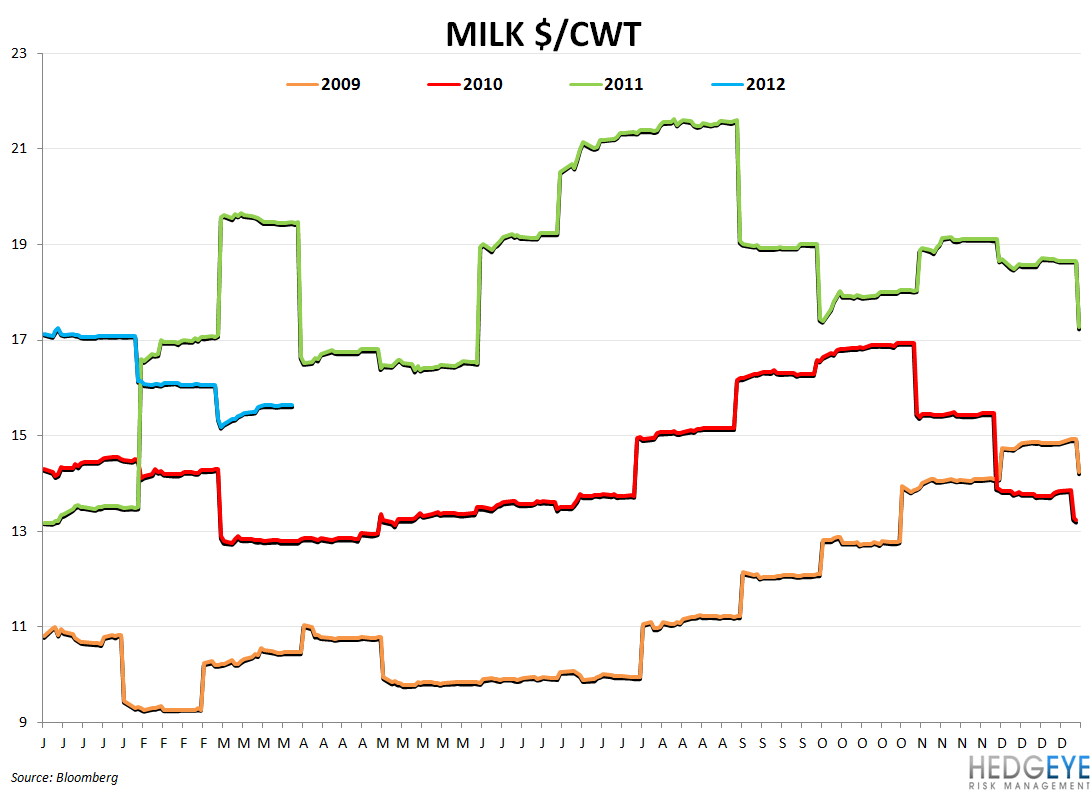

CHARTS

Howard Penney

Managing Director

Rory Green

Analyst