Hedgeye’s Retail Sentiment Monitor, comprised of short interest stats & sell-side sentiment, supports our bullish view on URBN and LIZ, as well as our bearish view on HBI, GIL and JNY. It suggests our view on JCP, PVH, TJX and ROST are closer to consensus.

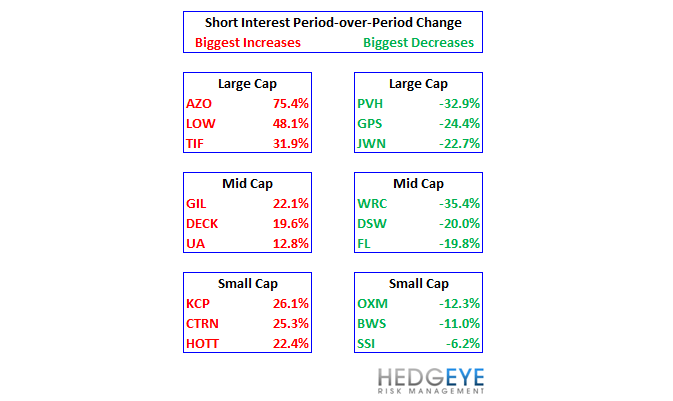

As for retail overall, there were some meaningful changes in short interest since the prior release on March 11th. We saw the greatest changes out of Large cap retail (+3.19% PoP) with less meaningful changes out of the small (+1.75% PoP) and mid cap names (-2.46% PoP). The 3.19% increase in large cap short interest was driven primarily by growing bearish sentiment at AZO (+75.4%), LOW (+48.1%) & TIF (+31.9%). PVH experienced the greatest short covering in large cap retail period over period with shares selling short down ~33%; there were also notable reductions in GPS (-24.4%) and JWN (-22.7%) short interest on the margin.

Here are some thoughts on changes we’re seeing in our sentiment monitor:

URBN: Sentiment has leveled out and has begun to improve after a simply massive 40-point hit over the past year. We like URBN here- these problems are identifiable and although it will take several quarters to fix, URBN has some of the cleanest inventories in retail with improving topline/margin compares headed into 2H. For additional detail on our URBN thesis, please see URBN: A Winner in 2012 (3/22/12).

ROST/TJX: Sentiment remains overwhelmingly positive -- near two year highs in sentiment for both names. We expect the off-price space to continue to benefit as the pricing battle at the mid-tier heats up and creates a domino effect on both margins and inventories for the industry. Excess inventory = better buys for the off-price channel. We wouldn’t chase them here. But the fundamental call is a tough one to bet against.

HBI/GIL: Sentiment scores remain elevated with HBI improving 3 points on the margin despite our expectation that both companies will underperform expectations in 2012.

JNY: Sentiment remains in the 20-25 range, the lowest score amongst low/mid tier apparel brands. JNY’s score might come across as overly bearish, but keep in mind that it is still 2.5x more positive than LIZ, which is a better company in every way. We don’t like JNY here. Sales are rolling organically, and JNY continues to cut SG&A to mitigate margin hit setting the company up for a miss later this year. We don’t believe JNY’s brands have a loyal customer base which creates a dangerous environment when competitive pressures are about to heat up at JCP, KSS, M, TGT, and SHLD. See our JNY note following the quarter; JNY: 9W & Other (2/9/12).

PVH: Per our note out yesterday, PVH is one of our favorite large cap longs in 2012 headed into and out of this afternoons print- PVH: Still Positive Pre & Post Qtr (3/26/12) but we need to stay mindful of the fact that its sentiment score is near historical peak.

JCP: Continues to decline on the margin. We still think that Johnson’s execution on his reinvigorated department store concept remains akin to the biggest retail Hail Mary in 25 years, and will be extraordinarily disruptive to the supply beginning yesterday.

SCVL: now has the highest sentiment score in retail (NKE in 2nd at 85), thought only up 1 point period over period, the score has improved 16 points over the past 3 months. Short interest as a % of float remains below 2% and 6/6 of the ratings on the stock are BUY. Yes, it’s micro cap ($450mm) with tight borrow. But it is a significant divergence nonetheless.

JWN/M: The spread between M & JWN sentiment is currently at 31 points vs an average of 10 points throughout 2011. Fundamentally, we like JWN better than M.

Sentiment Framework Methodology

Our updated Hedgeye Retail Sentiment scorecard is published in conjunction with last night’s short interest release. As a reminder, we use our Scoreboard as a piece of our TRADE (Trade=3 week or less duration) framework. The sentiment scores combines buy-side and sell-side conviction measures (Including Buy/Sell Ratings & Short Interest as a percent of float); we standardize those measures to an index of 0-100, where 100 is the best possible sentiment ranking and 0 is the worst. The idea is that a contrarian strategy can be employed at the extremes (positive extreme >90, negative extreme <20) to screen for names that provide the opportunity for the greatest upside relative to the consensus view. A sentiment score above 90 (overly bullish) has proven to be a good historical ‘sell’ signal, while a signal below 20 has proven to be better to Buy. We recognize that some names may break into the 90+ or 20/below thresholds and won’t immediately trade contrary to consensus. In fact, companies like Nike & LIZ have remained in the high/low bands over extended period of times. While our sentiment monitor acts as an excellent screening tool at major inflection points, we incorporate additional tools/analysis (SIGMA, Management Scorecard, etc.) to properly contextualize fundamental opportunities across all durations. Some stocks will never break out of their band, but marginal directional changes matter. We have back tested these levels for our group and the result can be seen below. Note that the analysis below was performed using the ~100 companies included in the monitor when the framework was initially created.

In an effort to provide additional context and compliment a company’s sentiment score, we also focus on insider transactions in conjunction with shifts in buy/sell side sentiment to gauge the overall conviction on a particular name. For additional detail on the methodology behind our proprietary sentiment measures or historical detail for a specific company, please contact the team. Below, we have included HIBB as an example as well as the historical trends in sentiment by retail subsector.