Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

Key Takeaways:

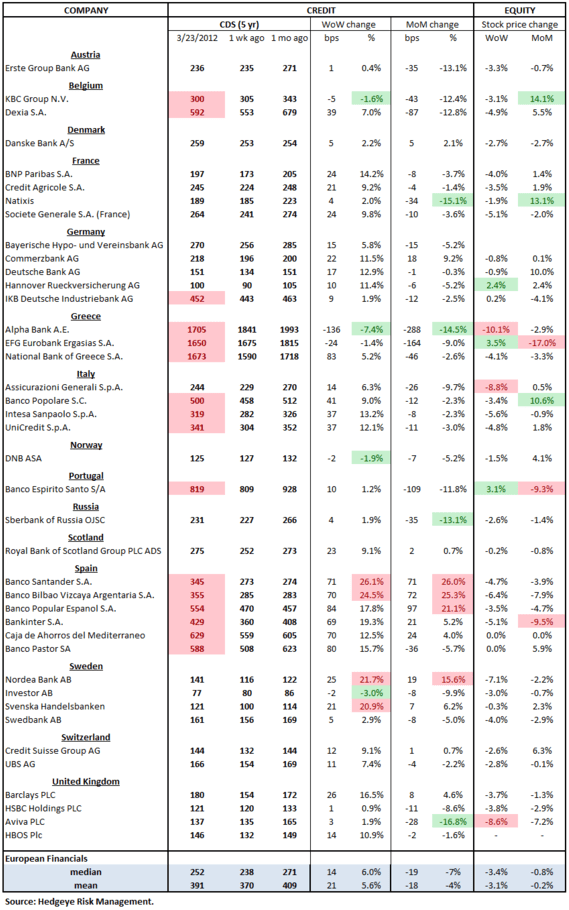

* Spain and its banks are getting worse. Spanish bank default swaps were materially wider week-over-week, rising an average 74 bps, or 18%. All six of Spain's major banks, on which swaps trade, are trading well over 300 bps (the "Lehman line"). Spanish Sovereign swaps widened by 27 bps to 427 bps. While most investors are focused on the rapid deterioration taking place in Portugal, we think Spain is the one to watch more closely. Will 2012 be a redux of 2011 on the Europe front, this time with Spain playing the lead role? Looking at sovereign and bank swaps of a country in conjunction has generally been a solid cointegrated risk measure.

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 3 bps to 45 bps.

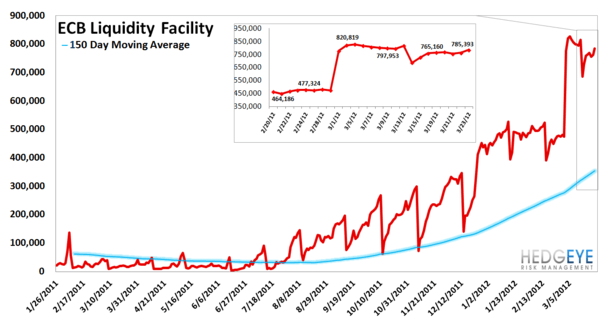

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis. The facility reached €785.4 Billion on 3/23.

European Financials CDS Monitor – Bank swaps were wider in Europe last week for 35 of the 40 reference entities. The average widening was 5.6% and the median widening was 6.0%.

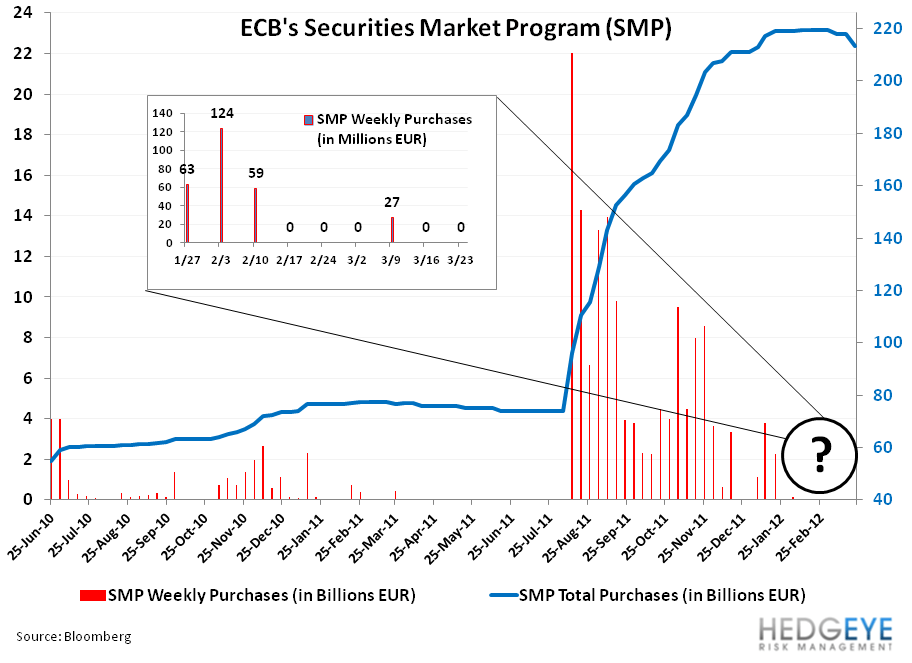

Security Market Program – The ECB's secondary sovereign bond purchasing program purchased no sovereign paper in the week ended 3/23, for a second straight week of zero buying. February-to-date the Bank has purchased a mere €210 Million versus €2.2 BILLION in the week ended 1/20 and €3.8 BILLION in the week 1/12. When questioned on the lack of buying over recent weeks, ECB President Draghi has only answered that the SMP is a non-standard measure that is “neither eternal nor infinite.” Clearly, with the some €1 Trillion injection of liquidity across the LTROs, the Bank is paring back buying and watching the results of sovereign bond auctions.

Matthew Hedrick

Senior Analyst