TODAY’S S&P 500 SET-UP – March 26, 2012

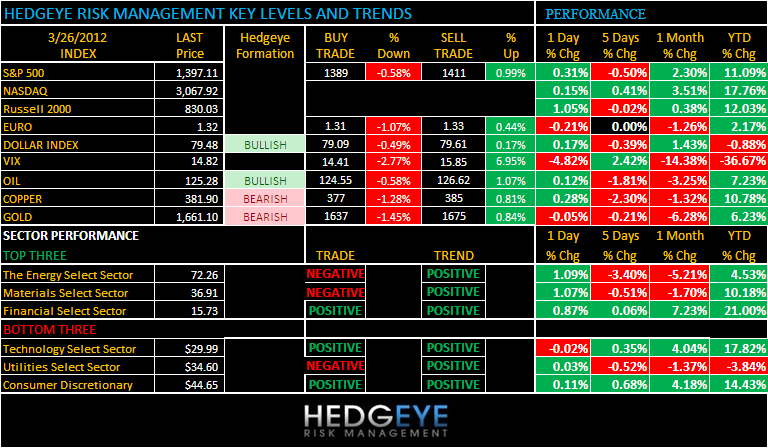

As we look at today’s set up for the S&P 500, the range is 22 points or -0.58% downside to 1389 and 0.99% upside to 1411.

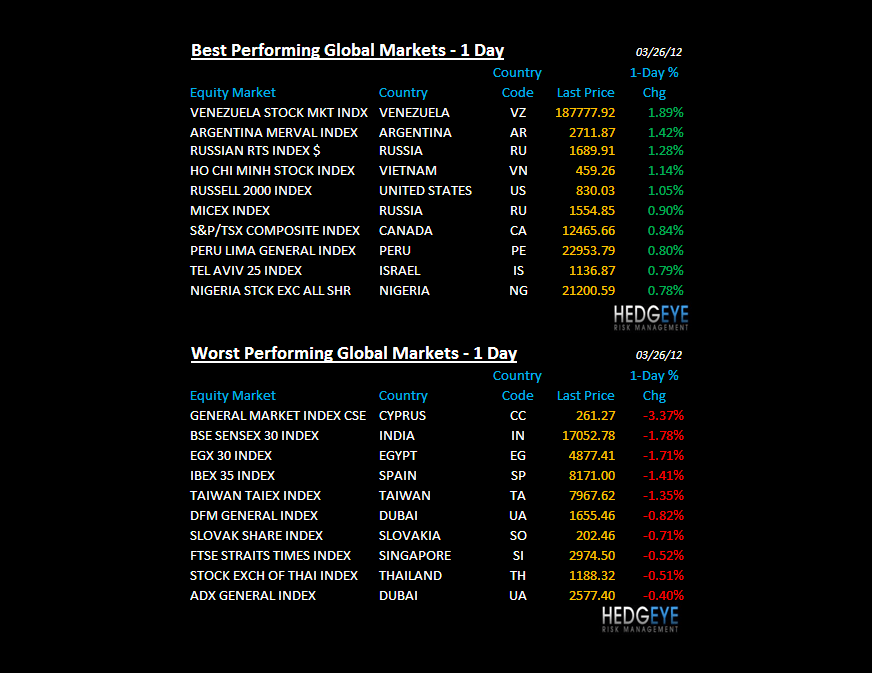

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1262 (2770)

- VOLUME: NYSE 741.64 (-2.79%)

- VIX: 14.82 -4.82% YTD PERFORMANCE: -36.67%

- SPX PUT/CALL RATIO: 1.96 from 2.49 (-21.29%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 40.19

- 3-MONTH T-BILL YIELD: 0.07%

- 10-Year: 2.28 from 2.23

- YIELD CURVE: 1.91 from 1.88

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: Fed’s Plosser speaks in Paris

- 8am: Fed Chairman Bernanke speaks in Virginia

- 8:30am: Chicago Fed Nat Activity Index, Feb. (prior 0.22)

- 10am: Pending Home Sales (M/m), Feb., est. 1.0% (prior 2.0%)

- 10:30am: Dallas Fed Manufacturing, Mar., est. 16 (prior 17.8)

- 11:30am: U.S. to sell $30b 3-mo., $29b 6-mo. bills

GOVERNMENT:

- Supreme Court hears health-care challenge

- President Obama attends nuclear summit in South Korea

- FTC hosts press conference on release of final privacy framework report

- House, Senate in session

WHAT TO WATCH:

- Supreme Court hears first of three days of arguments over President Obama’s health-care law

- Yahoo named three new board members after failing to reach compromise with Third Point, which pledged a proxy fight

- Rick Santorum won Louisiana Republican primary on Saturday; next major primary is Wisconsin on April 3

- Obama warned North Korea its plan to fire long-range rocket undermined prospects for future negotiations

- Bats Global blamed computer malfunction for trading errors last week that results in Bats pulling IPO

- Pending home sales may have climbed 1% in Feb. after a 2.0% gain in Jan., economists est: Weekly eco preview

- U.K., most of Europe set clocks ahead one hour over weekend

- Citigroup expects $700m impairment charge in 1Q as it cuts its investment Turkey’s Akbank by more than half

- Roche extended its $5.7b hostile takeover offer for Illumina for a second time

- U.S. Treasury Department set to sell on or around today preferred stock in six banks it bought stakes in as part of TARP

- ING said to be seeking at least $7b for Asian insurance business and has drawn interest from potential suitors including MetLife

EARNINGS:

- Cal-Maine Foods (CALM) 6:30 a.m., $1.02

- Kior (KIOR) 4:01 p.m., $(0.15)

- Apollo Group (APOL) 4:05 p.m., $0.37

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – the Doctor continues to look exactly like the slope of global growth, slowing. Copper now bearish TRADE and TAIL with big TRADE resistance overhead at $3.85/lb.

- Hedge Funds Make Wrong-Way Bets for a Fourth Week: Commodities

- Soybeans Jump to Six-Month High as U.S. Growers Favor Corn

- Copper Swings Between Gains, Drops as European Crisis May Worsen

- Oil Falls, Extending Two-Week Drop on Europe Debt, Slower China

- Sugar Falls to One-Week Low on Indian Supplies; Cocoa Advances

- Gold May Fall in London as Dollar Strengthens, ETP Holdings Drop

- China’s Soft Landing Still May Be Hard for Commodity Exporters

- Robusta Coffee May Gain 10% as Emerging Markets’ Demand Climbs

- Gold Imports by India to Slump as Jewelers Extend Shutdown

- Shale Boom in Europe Fades as Polish Wells Come Up Empty: Energy

- Vitol Said to Buy Diesel From Mangalore Refinery for May Loading

- Total Says North Sea Elgin Field Output Halts After Gas Leak

- Asia Naphtha Crack Rebounds; Chevron Sells Fuel: Oil Products

- Hedge Funds Make Wrong Way Bet for 4th Week

- BG, Eni Make New East Africa Gas Finds Larger Than U.K. Reserves

- Japan Has One Reactor With 1.9% of Total Capacity Online

- German Next-Month Clean-Dark Spread Falls to Lowest Since August

CURRENCIES

EUROPEAN MARKETS

SPAIN – continued selling in Spanish stocks, down -1.8% to start the week and now down -5.1% for the YTD (vs Germany +18.6%) and Super Mario Monti wants “firewall.” It ain’t over, till its over folks.

ASIAN MARKETS

JAPAN – clients want a “catalyst” in the Japanese Sovereign Debt Crisis – here’s ours: gravity. The Yen kicks off the week down -0.4% vs the USD (after Goldman said buy Yen Fri) and former exec director of the BOJ (Hirano, from 2002-2006) saying that Japan has “crossed the Rubicon with really desperate measures.”

MIDDLE EAST

The Hedgeye Macro Team