Positions in Europe: Short Greece (GREK), Short Spain (EWP)

Asset Class Performance:

- Equities: The EuroStoxx50 closed down -3.2% week-over-week. Bottom performers: Russia (MICEX) -4.6%; Finland -3.5%; Italy -3.5%; Sweden -3.5%; France -3.3%. Top performers: Greece 1.0%; Portugal 70bps; Slovakia 10bps.

- FX: The EUR/USD is up +0.67% week-over-week. W/W Divergences: HUF/EUR -1.41%, NOK/EUR -1.09%, PLN/EUR -0.77%; RON/EUR +0.28%. YTD Performance: PLN/EUR +7.56%, RUB/EUR +7.28%, HUF/EUR +7.17%, CZK/EUR +3.93%, NOK/EUR +1.42%, CHF/EUR +0.90%; ISK/EUR -5.11%, RON/EUR -1.00%, GBP/EUR -0.21%, SEK/EUR -0.12%.

- Fixed Income: Greek 10YR yields gained +192bps week-over-week to 20.04%, with a +181bps change in the Friday/Thursday period ahead of today’s deadline for holders of international law Greek bonds to give notice on swap participation. 10YR yields for Spain and Italy move higher by 34bps (to 5.53%) and 31bps (to 5.15%), respectively, as Portugal saw the largest contraction versus its peers at -98bps to 12.66%.

Call Outs:

Germany - Merkel is planning to build offshore wind farms that will cover an area six times the size of New York City and erect power lines that could stretch from London to Baghdad.

- The program will cost €200 billion (~ 8% of 2011 GDP) and aims to replace 17 nuclear reactors that supplied about a fifth of its electricity with renewables such as solar and wind, according to the DIW economic institute in Berlin.

- (+) Suntech Power Holdings Co. (STP) (Solar Panel), Vestas Wind Systems A/S (VWS) (Wind Turbines). (-) nuclear stations, RWE AG (RWE) and EON AG (EOAN).

Germany - Mercedes dealers in China are offering record markdowns of 25% on high-end models such as the S300 sedan, according to data stretching back to 2009 at cheshi.com.

Ireland - A fund affiliated with Apollo Global Management said that it will buy the Irish consumer-credit-card portfolio from Bank of America BAC.

Spain/Ireland - Goldman notes Spanish housing market is bad and getting worse. Ireland remains the worst of the worst and Goldman sees yet another growing divide between the haves and have-nots of Europe as the residential property price performance can essentially be split into four groups: Strong, Recovering, Weak, and Ireland/Spain.

France - Sarkozy vs. Hollande: A BVA poll of 978 voters taken March 21 and 22 after the terrorist incident gave Hollande 29.5 percent support, compared with 28 percent for Sarkozy.

In Review:

In last week’s European Monitor titled “Guiding Expectations” we set out the fundamentals and market trends that we believe should temper expectations that Europe is “out and in the clear”. These days of our lives spell very weak growth in Europe due to fiscal consolidation, a necessary evil in particular for the PIIGS.

This week, equity market performance tanked alongside Manufacturing and Service PMIs for March that showed a decidedly negative month-over-month move to the downside, to levels at or below the 50 line representing contraction (see chart below).

As we explained in recent research, we’re increasingly worried about Spain. This coming Friday’s budget announcement from Spanish PM Rajoy will be an important signal for the market. Rajoy must push through further fiscal consolidation to help meet the deficit target of 5.3% of GDP this year from 8.5% in 2011. This is a tall order, and already there’s been much push-back from the populace on issued austerity. Given an already fractured economy with weak confidence and sky-high unemployment (23% avg. and +50% for youth), we think a social uprising is in the cards.

One indicator of rising concern is 10 YR Spanish bond yields rising higher then Italian, the first occurrence since August 2011. Further there’s indication that many Spanish lenders have yet to recognize the full extent of their loan losses, which puts further pressure on the underfunded EFSF and ESM bailout packages.

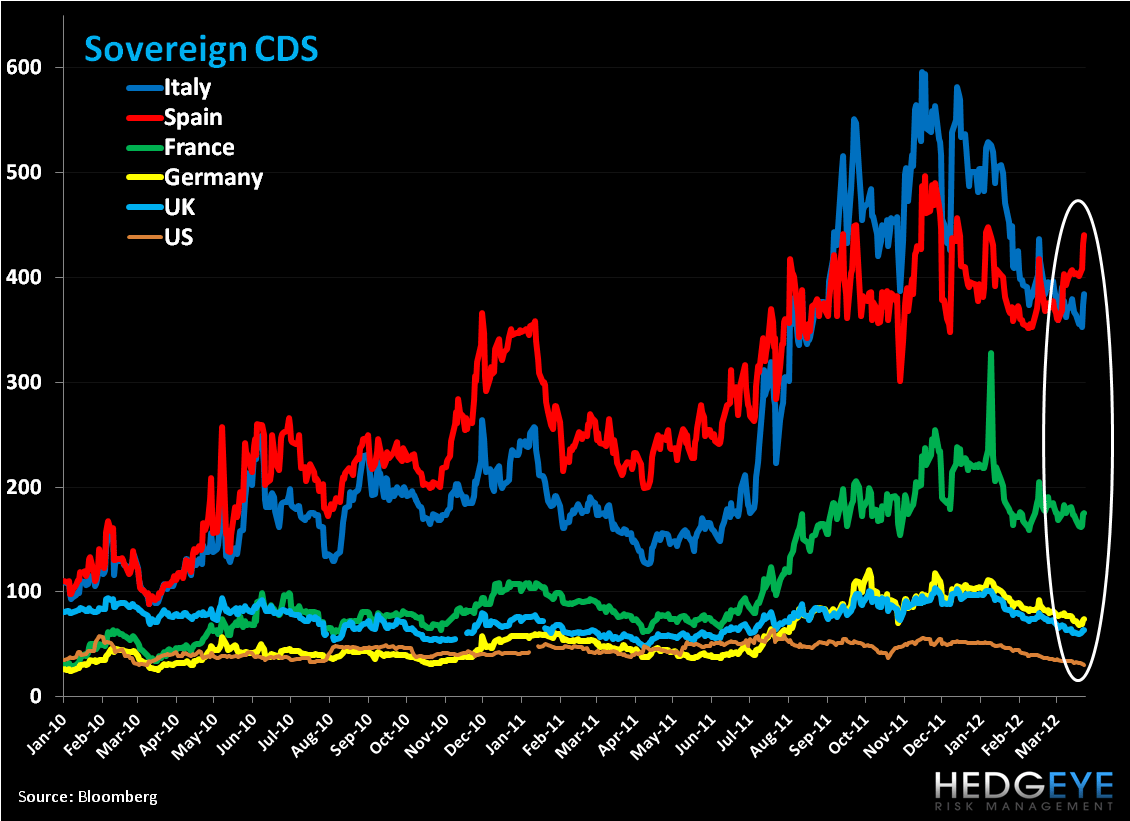

CDS Risk Monitor:

CDS fell -94bps to 1217bps in Portugal on a w/w basis to lead decliners. Ireland fell -18bps to 617bps. Spain led gains, advancing +36bps to 440bps (or 140bps over the Lehman Line of default risk) and Italy pushed up +20bps to 384bps.

Data Dump:

Eurozone Construction Output -1.4% JAN Y/Y vs 9.8% DEC [-0.8% JAN M/M vs -1.9% DEC]

Eurozone Composite 48.7 MAR (exp. 49.6) vs 49.3 FEB

Eurozone Current Account (net nsa) -12.3B EUR JAN vs 18.3 B EUR DEC [4.5B EUR JAN vs 3.4B EUR DEC]

Eurozone Industrial New Orders -3.3% JAN Y/Y (exp. -3.1%) vs -0.4% DEC [-2.3% JAN M/M (exp. -2.2%) vs 3.5% DEC]

Germany Producer Prices 0.4% FEB M/M (exp. +0.5%) vs 0.6% JAN [3.2% FEB Y/Y (inline) vs 3.4% JAN]

Italy Industrial Sales -4.4% JAN Y/Y vs 5.4% DEC

Italy Retail Sales -0.8% JAN Y/Y (exp. -3.4%) vs -3.7% DEC [0.7% JAN M/M (exp. -0.1%) vs -0.8% DEC]

France Business Confidence Indicator 96 MAR (exp. 93) vs 93 FEB

France Production Outlook -15 MAR (exp. -28) vs -27 FEB

France Own-Company Production Outlook 6 MAR vs -1 FEB

Switzerland Industrial Production 7.9% Q4 Q/Q (exp. +2.6%) vs -2.0% in Q3

Switzerland Money Supply M3 6.4% FEB Y/Y vs 7.3% JAN

Switzerland Exports 9.2% FEB M/M (exp. +0.3%) vs -10.4% JAN

Switzerland Import -12.3% FEB M/M vs 5.5% JAN

UK CPI 3.4% FEB Y/Y (exp. 2.3%) vs 2.6% JAN [0.6% FEB M/M (exp. 0.4%) vs -0.5% JAN]

UK RPI 3.7% FEB Y/Y (exp. 3.5%) vs 4.0% JAN

UK Public Sector Net Borrowing 12.9B GBP FEB vs -10.2B GBP JAN

UK Retail Sales w/ Auto Fuel -0.8% FEB M/M (exp. -0.5%) vs 0.3% JAN [1.0% FEB Y/Y (exp. 2.4%) vs 1.4% JAN]

UK BBA Loans for House Purchase 33,103 FEB (exp. 37,250) vs 37,977 JAN

Spain Producer Prices 3.4% FEB Y/Y (exp. 3.4%) vs 3.7% JAN [0.6% FEB M/M (exp. 0.7%) vs 0.9% JAN]

Portugal Producer Prices 4.1% FEB Y/Y vs 4.7% JAN [0.3% FEB M/M vs 2.3% JAN]

Ireland PPI 2.3% FEB Y/Y vs 2.7% JAN

Ireland Q4 GDP -0.2% Q/Q (exp. +1.0%) vs -1.1% in Q3 [0.7% Y/Y (exp 2.2%) vs 0.2% in Q3]

Finland Unemployment Rate 7.7% FEB vs 7.8% JAN

Interest Rate Decisions:

(3/21) Iceland Sedlabanki Interest Rate HIKE 25bps to 5.00%

The European Week Ahead:

Monday: Mar. Germany Import Price Index (Mar 26-20), IFO Business Climate, Current Assessment, and Expectations; Mar. UK Nationwide House Prices; Feb. France Jobseekers; Mar. Italy Consumer Confidence Indicator

Tuesday: Apr. Germany GfK Consumer Confidence Survey; Mar. UK CBI Reported Sales; Mar. France Consumer Confidence Indicator; Feb. Spain Budget Balance YtD

Wednesday: Feb. Eurozone Money Supply; Mar. Germany CPI; Q4 UK GDP – Final; Q4 France GDP – Final, Total Business Investment – Final, Current Account; Mar. Italy Business Confidence

Thursday: Mar. Eurozone Consumer Confidence Indicator – Final, Business Climate Indicator, Economic, Industrial, and Services Confidence; Mar. Germany Unemployment Data; Mar. UK GfK Consumer Confidence Survey, Feb. UK Net Consumer Credit, Net Lending, Mortgage Approvals, M4 Money Supply; Jan. UK Index of Services; Mar. Spain CPI – Preliminary; Jan. Spain Total Housing Permits

Friday: Mar. Eurozone CPI Estimate; Feb. Germany Retail Sales; Feb. France Producer Prices, Consumer Spending, Hourly Wages; Feb. Italy PPI; Jan. Greece Retail Sales; Spain Prime Minister Rajoy to present 2012 Budget; Feb. Spain Retail Sales; Jan. Spain Current Account

Extended Calendar Call-Outs:

22 April: French Elections (Round 1) begins, to conclude in May.

29 April: Potential Greek Presidential Elections.

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst