TODAY’S S&P 500 SET-UP – March 23, 2012

As we look at today’s set up for the S&P 500, the range is 22 points or -01.28% downside to 1375 and 0.30% upside to 1397.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1508 (-1476)

- VOLUME: NYSE 762.96 (5.02%)

- VIX: 15.57 2.91% YTD PERFORMANCE: -33.46%

- SPX PUT/CALL RATIO: 2.49 from 3.27 (-23.85%)

CREDIT/ECONOMIC MARKET LOOK:

US TREASURIES – the top in bond yields came last week when Credit Suisse said “buy stocks because bond yields are rising”; now it’s game time with TRADE line support for 10s at 2.27% and the long-term TAIL of resistance up at 2.47%. We are expecting to see a battle royal in this 20bps range.

- TED SPREAD: 40.25

- 3-MONTH T-BILL YIELD: 0.07%

- 10-Year: 2.26 from 2.28

- YIELD CURVE: 1.90 from 1.92

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: New-home sales, Feb., est. 325k (prior 321k)

- 10am: New-home sales (M/m), Feb., est. 1.3% (prior -0.9%)

- 1pm: Baker Hughes rig count

- 1:45pm: Bernanke gives opening remarks at Fed central banking conference

- 2:30pm: Fed’s Lockhart speaks in Washington

GOVERNMENT/POLITICS:

- Mitt Romney, Rick Santorum, Newt Gingrich, Ron Paul campaign across Louisiana ahead of state’s Republican primary tomorrow

- House, Senate not in session

WHAT TO WATCH:

- New-home purchases U.S. probably rose 1.3% in Feb. to 325k annual pace, highest level in more than a year, economists est.

- Bats Global Markets priced 6.3m shrs at $16 each, low end of range

- President Obama faces deadline today to make nomination for World Bank president

- Manhattan office leasing in 1Q is poised to be lowest in almost three years: Studley

- St. Louis Fed President James Bullard said U.S. monetary policy may be at turning point, Fed’s next interest-rate increase may come in late 2013

- US Airways said to be discussing plan for AMR takeover with some creditors

- Credit Suisse will start resupplying market with VelocityShares Daily 2x VIX Short-Term ETN, or TVIX, after cutting issuance off in February, causing market to whipsaw

EARNINGS:

- Darden Restaurants (DRI), 7am, est. $1.24

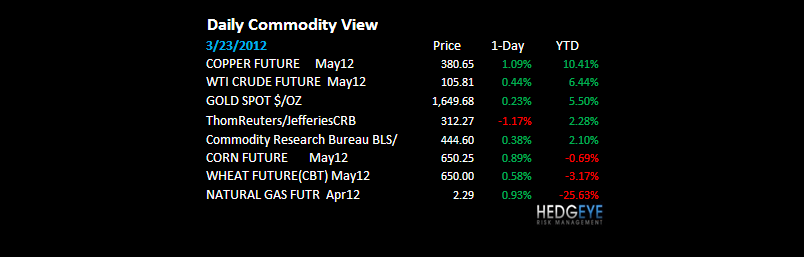

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Bear Streak Extends as Manufacturing Shrinks: Commodities

- Soybeans Rise as U.S. Growers May Shun Oilseeds in Favor of Corn

- Copper Advances as Housing Report May Show Increased Purchases

- Crude Rebounds From One-Week Low, Paring Decline for the Week

- Palm Oil Jumps to 10-Month High on Malaysia Production Concerns

- Commodity Brokers Get Shelter From Europe’s Shift to Exchanges

- Gold May Advance From 10-Week Low as Weaker Dollar Spurs Demand

- Glut Sends Gas Toward Worst Quarter Since 2010: Energy Markets

- Rubber Set for Third Weekly Drop on Europe, China Demand Outlook

- China’s Appetite for U.S. Farm Goods Target of USDA Mission

- Palladium May Decline on ‘Trend Momentum’: Technical Analysis

- Texas Tops Finds From Brazil to Bakken as Best Prospect: Energy

- Oil May Fall on Lower U.S. Demand, Saudi Capacity, Survey Shows

- Copper Bear Streak Extends as Output Falls

- Cargill Says Gavilon May Likely Be Acquired by ‘New Player’

- Country-Best Rally Spurs Minerva’s Market Return: Brazil Credit

- Resource Firms Lead Surge in Convertible Issuance: Canada Credit

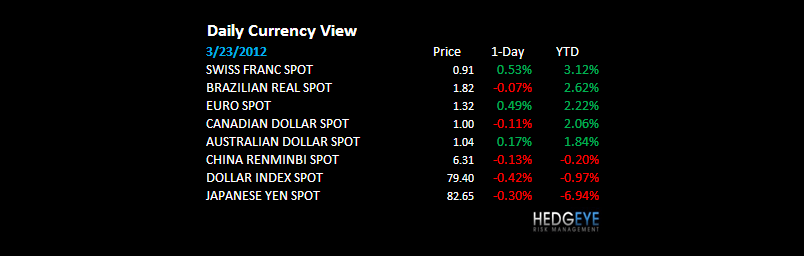

CURRENCIES

EUROPEAN MARKETS

SPAIN – the Spanish IBEX continues to flag negative divergences vs most major markets of the world (down -2% YTD vs Russia +20%) and Spain’s bond yields continue to move up into the right. German Finance Minister on Spain and Italy yesterday: “they are too big to save”… alrighty then.

ASIAN MARKETS

JAPAN – currencies lead bonds, then currencies/bonds lead stocks – that’s what happened into the European Sovereign Debt Crisis and we don’t know why that would change in Japan. The Yen looks awful and finally the Nikkei broke an important line of immediate-term support (10,065) last night.

MIDDLE EAST

The Hedgeye Macro Team