Keith added Urban Outfitters to the Hedgeye Virtual Portfolio today. This is a name we’ve watched for the better part of the past year while it was a lightning rod of the hedge fund community. But we think that the setup for the stock is turning favorable across multiple durations.

TAIL (3 years or less):

This is one of the few companies that can put up double digit square footage growth over the course of our 5-year model – and likely beyond. It’s not married to one concept that will simply max out growth when it runs out of malls – like what we saw at brands like Gap, American Eagle and Ann Taylor. We don’t think that its two major brands – Urban Outfitters and Anthropologie – are broken. They had fashion problems over the past year, which we think stem from poor execution by management. Fashion is a tough business, but when the right buying infrastructure is in place, there shouldn’t be a whole lot of risk for a company that sells third party brands. Rather, URBN got sloppy in both product selection, quality and even PR. It lost sight of who its customer is, and merchandised accordingly. Yes, there is a customer ‘piss off’ factor that hurts for a time. But ultimately if URBN has the right organization in place, it will have the right product, which it will then sell to the right customer.

The good news from our perspective is that a merchandising issue like this for a vertically integrated company often takes 1.5-2-years to fix. But for URBN, we can see results much sooner. We saw CEO Glen Senk ‘step down’ in early January, and we saw founder Richard Hayne – who is extremely well liked and respected by the organization - stepping back in totake control. Ted Marlow is also back heading the Urban Outfitters brand, after leaving when Senk was chosen for the CEO role.

Bears on this name say that this will never be the URBN of old. We could care less. It does not need to be the URBN of old to work from here. Recouping only half of its margin erosion of the past two years gets us to 12x earnings and 6x EBITDA based on today’s price. We’ll take that any day.

TREND (3 months or more):

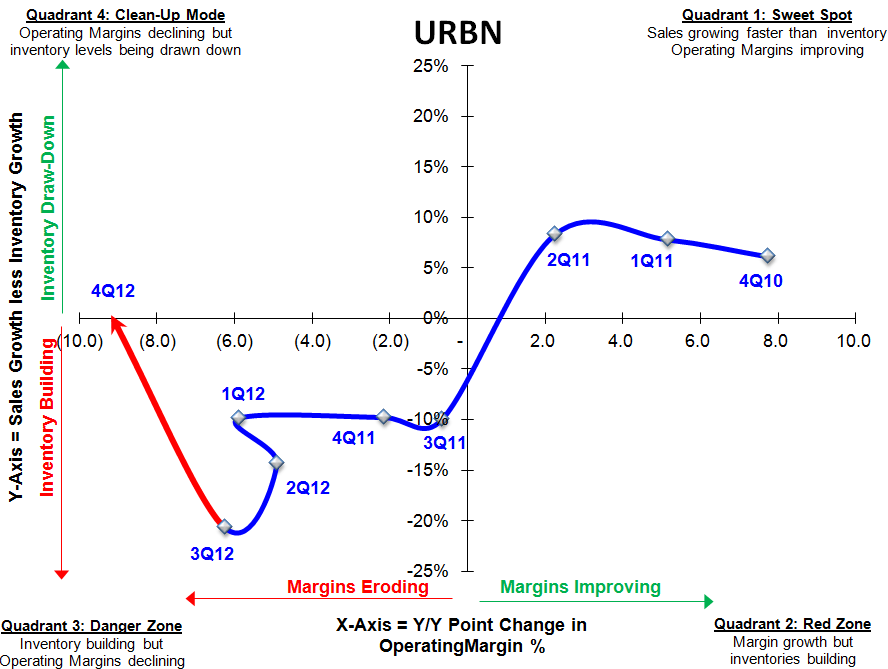

While we’re not looking for an immediate turnaround, we should start to see tangible results within two quarters. Starting with the April quarter, revenue compares at both Anthro and Urban get increasingly easy. More notably, its inventories are exceptionally clean. The company’s move in our SIGMA analysis is unlike most other companies in retail (see below). Given our concern about 2H margins for the space in aggregate, we think that URBN will buck the trend in every direction. Better working capital and capex driving better margins simultaneously with better execution and sales.

TRADE (3 weeks or less):

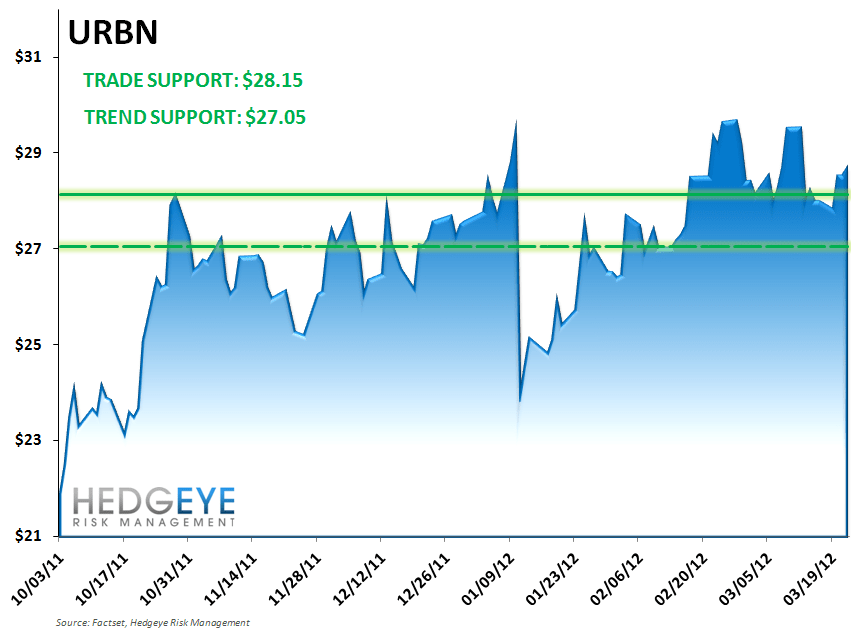

The stock has stopped going down on bad news, the short interest as a percent of float is high at 12%, and 53% of sell side ratings are NOT Buy. Near-term risk management levels on Keith’s models are :

TRADE = 28.15

TREND = 27.05

He’ll be managing risk around near-term positioning from a PM vantage point. Looking longer out, you’re going to see us get louder on this one. We think it could be a LIZ-like winner in 2012.