POSITIONS: Long Utilities (XLU), Short SPY, XLI, and XLY

Both my Fundamental Research and Risk Management positions are crystal clear. Global Growth Slowing (like it has after Q1 of 2008, 2010, and 2011) as inflation accelerates sequentially, remains the most important signal coming out of our globally interconnected macro model.

Strong Dollar is the only long-term protection against rising inflation expectations. Since I am long the US Dollar again, I expect that to eventually A) Deflate The Inflation (bad for Commodities) and B) provide a stimulus for Global Consumption, on a lag.

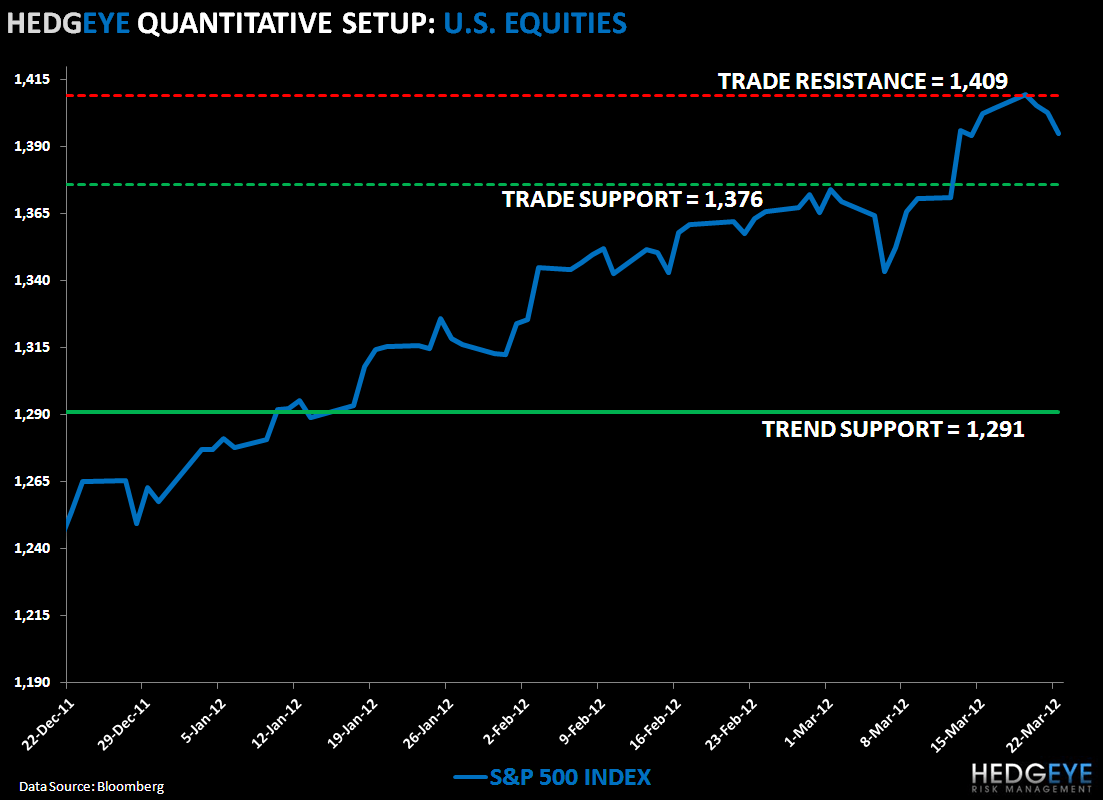

Across all 3 of my core risk management durations (TRADE, TREND, TAIL), here are the lines that matter most:

- Immediate-term TRADE resistance = 1409

- Immediate-term TRADE support = 1376

- Intermediate-term TREND support = 1291

In other words, if a Strong Dollar emerges ($85-88 on the US Dollar Index), the market should hold 1291.

KM

Keith R. McCullough

Chief Executive Officer