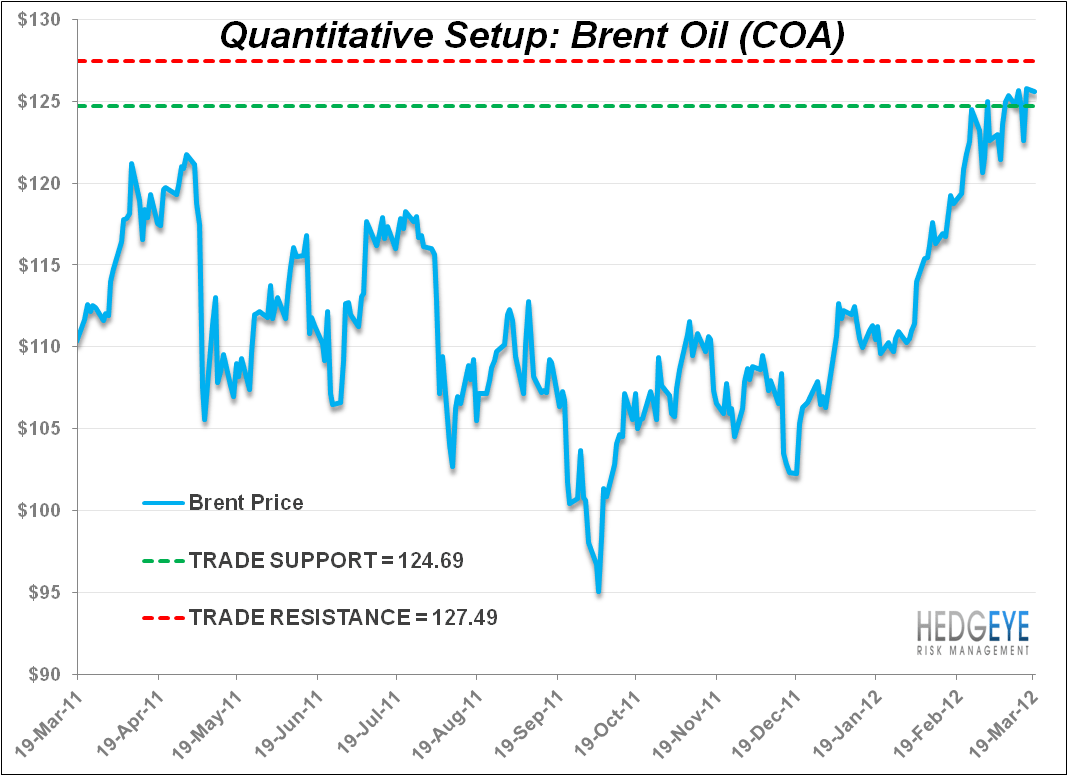

Conclusion: While recent comments by Israeli Prime Minister Netanyahu suggest an attack on Iran’s nuclear facilities by Israel could occur in 2012, it is not clear if he would have the broad support of the Israeli people. Further, there are potentially a number of unintended consequences. As we highlight in the chart below, oil continues to trade with a premium due to the heightened rhetoric in the Middle East.

Positions: Long Oil via the etf OIL

We are planning on doing a conference call in the coming weeks with a foreign policy expert on Israeli and Iranian relations, but in the meantime we wanted to provide some context on the next potential catalyst in this standoff. Rather than introduce our own speculation, we’ve compiled specific public comments related to potential timing of an attack by Israel, the route or plan that the Israelis would likely follow, and some secondary consequences.

Potential Timing of Attack

As for the timing of the attack, Prime Minister Binyamin Netanyahu told Israeli TV after his trip to Washington that, “it's not a matter of days or weeks but also not of years” before Israel would resort to military action in response to the potential nuclear threat from Iran. (UPI)

YNet News, Israel’s most read newspaper, reported that Israel will attack Iran no sooner than November of this year (after the presidential election). This came out through a White House official after the meeting between President Obama and Prime Minister Netanyahu in early March. (Ynet)

Dr. Emanuele Ottolenghi, a senior fellow at the Foundation for Defense of Democracies in Washington added, “I think the Israelis will take that action only if they feel that their back is completely against the wall, that Iran is about to cross the finish line on its road to a nuclear weapon, and no-one else is willing to do it.” (ABC)

Potential Attack Plan

The following information came from an interview with Dr.Ottolenghi. He said that the most likely route of entry would be either a northern route (through Turkey and Iraq or Syria and Iraq) or a southern route (along the Iraqi/ Saudi Arabian border). The southern route is much longer thus he said it would be less likely because the attack would test the outer limits of the Israeli Air Force, and might result in in-flight refueling. (ABC)

Dr. Ottolenghi further suggested that all of the countries involved in the attack passage (potentially Turkey, Syria, Iraq, and Saudi Arabia) would possibly face resistance from Iran if they opened their air space to an Israeli air strike. (ABC)

As far as the type of attack that Israel would exercise, Dr. Ottolenghi hinted that if the attack were to occur it would come from air attacks and missiles and not from a pre-emptive nuclear strike as such actions are unprecedented. (ABC)

Consequences for Attack

Debating the consequences of an Israeli attack we think it will be useful to look at the event of a failed destruction of the Iranian nuclear facilities. The former head of the Mossad, Meir Dagan, said during a recent interview on 60 Minutes that no attack could stop the Iranian nuclear effort, but rather only delay it. (CBS)

The entirety of his interview can be found below:

Dr. Ottolenghi’s view is that the primary issue with a failed attack is the fact that Iran would still have their nuclear facilities in tact and would then have a reason to back out of the Non-Proliferation Treaty. He said this would be the WORST case scenario, but he presented other more likely alternatives.

1. Hezbollah attack on the northern border from Lebanon

Mark Fitzpatrick, director of the Non-Proliferation and Disarmament Programme at the London-based International Institute for Strategic Studies (IISS) says, “the Shia Islamist group Hezbollah, has more than 10,000 rocket launchers in southern Lebanon, many of them supplied by Iran.” He went on to state that the arsenal of missiles stockpiled in Lebanon have the range capability to hit all of Israel.

2. Hamas attack from the Gaza Strip

Fitzpatrick added that the Hamas also had the capability to launch their own missile based attack from the Gaza Strip, which could be devastating for Israel as this combination amounts to a military strike from both the northern and southern borders simultaneously. (BBC) This strategic cooperation also poses the risk of the violence expanding into a bigger war in the Middle East. (CBS)

3. Closing the Strait of Hormuz

BBC News reports that if the Strait of Hormuz was blocked that could result in “extended naval conflict between the US and Iran, and in the short term, there could be a significant impact upon oil prices.” (BBC) It is reported that 17 million barrels of oil are transported through the Strait of Hormuz each day which amounts to 20% of global supply. (ECON) The Economist went on to say, “Even a temporary closure would imply a disruption to dwarf any previous oil shock”.

4. Attack against oil installations along the Arabian shore of the Gulf

Karim Sadjadpour, an Iran expert at the Carnegie Endowment for International Peace, said “If Iran tries to destabilize world energy supplies - whether launching missiles into Saudi Arabia's oil-rich eastern province or attempting to close the Strait of Hormuz - the U.S. isn't going to stand aside idly.” (BBC)

5. Iranian attack of American targets

If Iran were to retaliate with option 3, 4, or 5 Dr. Ottolenghi said this would draw the U.S. into the conflict. Dr. Ottolenghi made the repercussions of U.S. involvement clear when he said, “it could spell the end of the regime if the Americans were drawn into this conflict.” (ABC)

6. Regional war

Dagan said that he thought the result of an Israeli attack would, “ignite regional war”. Dagan also said that he thinks the U.S. should step in and intervene instead of the Israelis. (CBS)

While one would think, at least based on some government rhetoric, the decision to launch an attack could rally the people of Israel around the government, a recent study published by Tel Aviv University and the Israeli Democracy Institute suggests otherwise. They reported that only 31% of Israelis support a unilateral strike against Iran by Israel while 63% are opposed. Ultimately, the sentiment could be a key factor in any decision Netanyahu and his cabinet make.

Of course, there is also a view that that Netanyahu is bluffing and that if he really believed that the Iranian threat was comparable to another Holocaust, he would have already taken action. As Jeffrey Goldberg aptly wrote for Bloomberg yesterday:

“But, if true, Netanyahu is proving himself to be an adept poker player. Obama told me in an interview that, “as president of the U.S., I don’t bluff." Whether Netanyahu bluffs is perhaps the more important question.”

Indeed.

Daryl G. Jones

Director of Research