Positions in Europe: Short Greece (GREK), Short Spain (EWP)

Asset Class Performance:

- Equities: Top performers: Hungary 4.7%; Germany 4.0%; Belgium 3.7%; Italy 3.7%; Austria 3.6%. Bottom performers: Cyprus -1.7%; Portugal -1.4%; Romania -70bps.

- FX: The EUR/USD is up +0.40% week-over-week. Divergences: HUF/EUR +0.96%, GBP/EUR +0.68%; NOK/EUR -0.84%, PLN/EUR -0.76%. The HUF/EUR leads all major expanded currencies at +8.87% year-to-date.

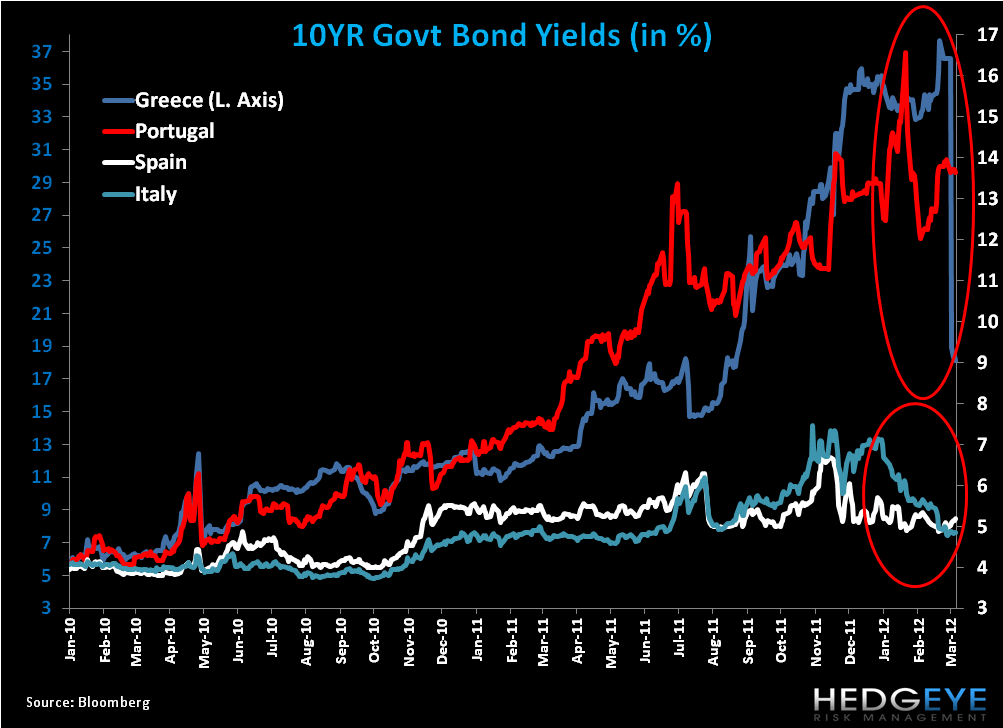

- Fixed Income: Greek debt was re-priced this week following agreement on the PSI; the Greek 10YR yield fell a monster 1844bps to 18.12% week-over-week. Portugal’s 10YR led to the downside, falling -22bps to 13.64%, while Spain saw the largest gain at +23bps to 5.19%.

Call Outs:

- Greece now has the highest gas price in the continent at over $9.00/gallon.

- Fitch upgraded Greece from restricted default to B-minus with a stable outlook following the completion of the country's debt swap with private investors.

- Greece’s Presidential election is to be held on April 29th or May 6th, spokesman Pantelis Kapsis.

- Spain - Finance Minister Luis de Guindos said Spain would comply with a demand by euro-zone finance ministers that it cut its deficit to 5.3% of gross domestic product in 2012, while sticking to its 2013 target of 3%.

- UK - Fitch revises UK outlook to Negative from Stable, and keeps country at AAA.

- Russia – President Medvedev’s human rights council urged him to pardon Mikhail Khodorkovsky in his last weeks in office, presenting legal advice that this doesn’t need an admission of guilt from the former Yukos Oil Co. owner. The recommendation will be discussed at the council’s meeting with Medvedev next month. [PM and President-elect Putin will take over as head of state on May 7].

In Review:

This week we added two European positions to the Hedgeye Virtual Portfolio, Spain (EWP) and Greece (GREK), both on the short side.

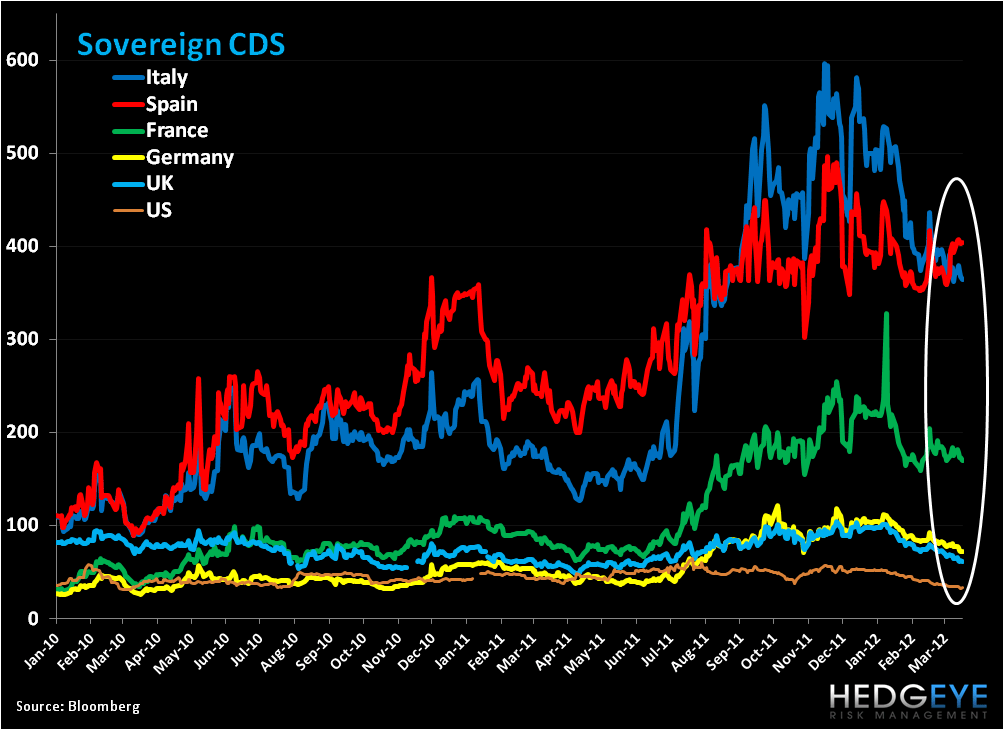

Despite the market’s recent optimism around the two rounds of 36-month LTROs and that we “cleared” Greece’s debt restructuring, we want to temper expectations that Europe is “out and in the clear”. While the LTROs have added needed liquidity to the system, there’s no evidence (yet) that this liquidity has enter the real economy. One negative data point we do continue to observe is Overnight Bank Deposits to the ECB, which is just off its high at €727.7 Billion. Further, this injection does nothing for solvency issues of banks; Spanish, Portuguese, and Italian lenders on the metric of 5YR CDS continue to flash risk levels that are comfortably above 350bps! While a re-pricing of Greek debt saw its 10YR sovereign bond yield fall nearly 1900bps in a straight line early this week, risk is clear and present in Portugal, with the 10YR at 13.6%. And while yields in Italy and Spain have trended lower YTD, there’s nothing that concretely justifies yields maintaining this retreat short of a Monti - Draghi handshake to take care of Italia.

While “cheap” credit flows should help to spark the region’s economy, it will be off a recessionary level in 2012, as outsized debt and deficits budge little and austerity takes a firm toll not only on confidence and spending but also government tax receipts. All this spells a very long runway ahead of slow growth, alongside threats of rising inflation, most notably from energy costs.

News out this week that Spain missed its 2011 deficit target was particularly representative of the structural fiscal imbalances versus expectations across much of the region. To review, Spanish PM Mariano Rajoy, elected in December of 2011, inherited a budget that was proved to be fudged, with the 2011 budget deficit now estimated at 8.5% of GDP versus a previous target at 6%. This gap has thrown off the 2012 budget deficit reduction program, and the government unilaterally (ex-EU agreement) revised its 2012 deficit target to 5.8% versus the original 4.4% promise. The EU this week said that wasn’t enough, and mandated that additional budget cuts worth 0.5% of GDP must be carried out.

Sound a bit like Greece? Can the market really believe Troika’s report that Greece can reduce its public debt to 120% of GDP by 2020? Does Troika even (truly) believe that given the myriad of variables between now and then? We don’t think so. What governments must realize is that shaving the fat off budgets is essential, but so are the expectations around meeting those cuts. Whether the EU or the countries themselves are responsible for setting goals that are too optimistic or too lenient (in trimming fat) is for another discussion, yet what’s important is that realistic targets are set around which markets can set expectations.

We do think that taking the pain now through fiscal austerity will sacrifice growth, but this is a necessary condition given the years of excess spending by the PIIGS (and others).

The road to maintain the existing Eurozone fabric is a clouded one. However, if it’s going to work, it will come at the hand of this fiscal consolidation and further bailouts to support the Eurozone project. There are plenty of arguments to justify an exit or dissolution of the Union, however here and now we won’t discount the fortitude of Eurocrats to hold the whole together, with shoe lace and all.

CDS Risk Monitor:

Short of Portugal, we did not see huge moves in 5YR CDS on a week-over-week basis. Portugal saw the biggest gain at +82bps to 1,311bps, followed by Ireland +15bps to 635bps. France saw the biggest drop (-10bps) to 169bps.

Data Dump:

Eurozone Economic Sentiment 11 MAR vs -8.1 FEB

Eurozone CPI 2.7% FEB Y/Y vs 2.7% JAN

Eurozone Industrial Production -1.2% JAN Y/Y (exp. -0.8%) vs -1.8% DEC

EU New Car Registrations -9.7% FEB Y/Y vs -7.1% JAN

Eurozone Trade Balance -7.6B EUR JAN (exp. -3B EUR) vs 9.1B EUR DEC

Germany Wholesale Price Index 1.9% FEB M/M (exp. 1.0%) vs 1.2% JAN [2.6% FEB Y/Y (exp. 2.6%) vs 3.0% JAN]

Germany ZEW Current Account 37.6 MAR (exp. 41.5) vs 40.3 FEB

Germany ZEW Economic Sentiment 22.3 MAR (exp. 10) vs 5.4 FEB (highest since June 2010)

Italy Q4 GDP Final -0.7% Q/Q (exp. -0.7%) vs previous -0.7% [-0.4% Y/Y (exp. -0.5%) vs previous -0.5%]

Italy CPI 3.4% FEB Final Y/Y UNCH

France CPI 2.5% FEB Y/Y (exp. +2.6%) vs 2.6% JAN [fell for 2nd month]

Spain CPI 1.9% FEB Final Y/Y UNCH

Spain House Transactions -26.3% JAN Y/Y vs -25.3% DEC

Spain House Price ToT Homes Y/Y -4.2% in Q4 Y/Y vs -2.8% in Q3

Switzerland Producers and Import Prices 0.8% FEB M/M (exp. +0.2%) vs 0.0% JAN [-1.9% FEB Y/Y (exp. -2.4%) vs -2.4% JAN]

Switzerland Credit Suisse ZEW Survey Expectations of Growth 0.0 MAR vs -21.2 FEB

UK Claimant Count Rate 5% FEB vs 5% JAN

UK Jobless Claims Chg 7.2K FEB (est. 5K) vs 7K JAN (12th straight increase)

UK ILO Unemployment Rate 8.4% JAN vs 8.4% DEC

Greece Unemployment Rate 20.7% Q4 vs 17.7% in Q3

Greece Industrial Production -5.0% JAN Y/Y vs -11.3% DEC

Sweden Unemployment Rate (SA) 6% FEB vs 6% JAN

Sweden Unemployment Rate 7.8% FEB vs 8% JAN

Ireland CPI 2.1% FEB Y/Y vs 2.2% JAN

Ireland Industrial Production -0.5% JAN Y/Y vs -3.5% DEC

Portugal CPI 3.6% FEB Y/Y vs 3.4% JAN

Interest Rate Decisions:

(3/14) Norway – Norges Bank CUT Deposit Rates 50bps to 1.75%.

(3/15) Switzerland – SNB 3M Libor Target Rate UNCH at 0.00%

The European Week Ahead:

Monday: Jan. Eurozone Current Account, Construction Output; Jan. Italy Industrial Orders and Sales

Tuesday: Greece 14.5 B Euro Bond Redemption; Feb. Germany Producer Prices; Feb. UK CPI, Retail Price Index, RPI, CBI Trends; Jan. Greece Current Account; Jan. Spain Trade Balance

Wednesday: UK BoE Minutes, Osborne Announces Budget Plans; Feb. UK Public Finances, Public Sector Net Borrowing

Thursday: Mar. Eurozone Consumer Confidence and PMI Manufacturing, Services, Composite – Advance; Jan. Eurozone Industrial New Orders; Mar. Germany PMI Manufacturing and Services – Advance; Feb. UK Retail Sales, Consumer Confidence; Mar. France PMI Manufacturing and Services – Preliminary

Friday: Feb. UK BBA Loans for House Purchases; Mar. France Production Outlook Indicator, Business Confidence Indicator, Q4 France Wages – Final; Jan. Italy Retail Sales

Extended Calendar Call-Outs:

22 April: French Elections (Round 1) begin, to conclude in May.

29 April: Potential Greek Presidential Elections.

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst