THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Commentary from CEO Keith McCullough

Top 3 Most Read (Bloomberg) this morning (Buffett, Billionaires, Morgan Stanley) all about Wall St comp; not about the “rally”; fascinating:

- INDIA – the Indians told the world they got off the Greenspan-put drugs (no rate cut), so the world sold their equity market down another -1% overnight (down -2.6% in 2 days). India is a net importer of inflation (oil) and has seen their yield curve go flat.

- OIL – after attempting to SPR global Consumers yesterday while they were watching some hoops, the Administration of Central Planning denied they’d ever politicize what the DOE defines (govt website next to the slide deck on Obama’s opinion on oil supply/demand) as “the last line of defense against a supply disruption." I bought oil on that as all 3 of my durations of support held like the rock of Gibraltar.

- USD – this is easily the most bullish development we’ve seen since Bernanke’s attempts to debauch the dollar (Jan 25th) – gravity. US Dollar Index should close up for the 3rd consecutive week – while it may not have been for Apple and BAC, this has been a huge headwind for anything Bonds, Gold, Foreign Currency, etc. this week. Yes, anyone who is diversified across Global Macro got tagged by this Correlation Risk.

Quadruple witching options expiration and a sequentially inflating US Consumer Price report up next.

KM

SUBSECTOR PERFORMANCE

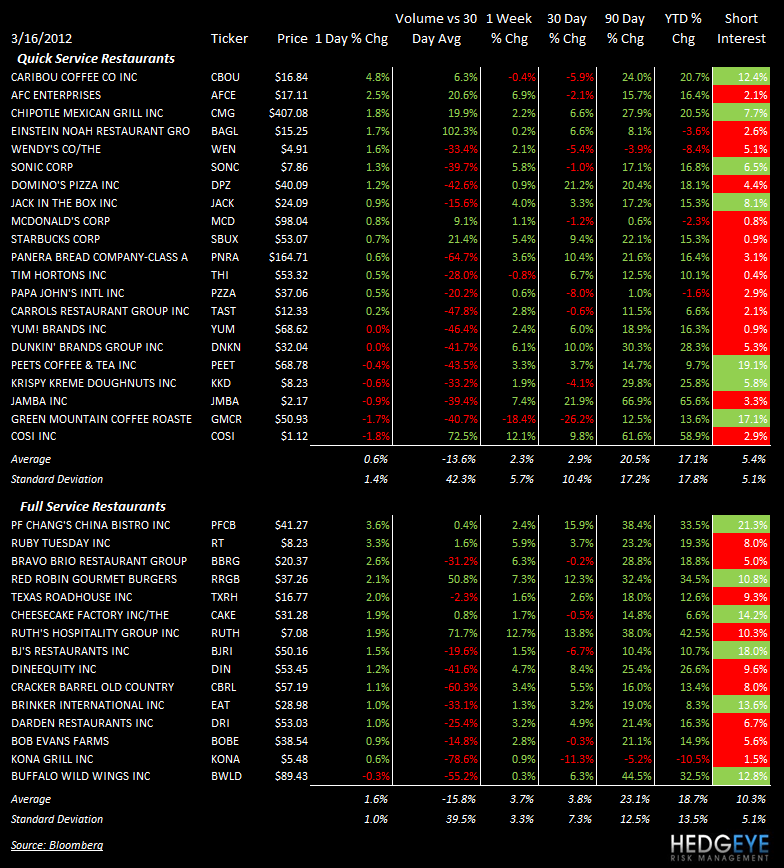

QUICK SERVICE

MCD: McDonald’s China executives were questioned by food safety regulators. According to media reports emerging this morning, McDonald’s sold chicken wings past their sell-by period. The McDonald’s restaurant in Beijing is reported to have sold chicken wings 90 minutes after they were cooked versus the company’s guidelines of a 30 minute limit. The company said that this is an isolated case.

SBUX: Starbucks was named one of the “World’s Most Ethical Companies” in 2012 by the Ethisphere Institute.

PNRA: Panera Bread founder Ron Shaich will share the title of CEO of the company with Bill Moreton, according to a press release published yesterday. The statement said, “The transition to co-CEOs formalizes a relationship that has evolved over the last year and is a reflection of the way in which Shaich and Moreton have been operating as partners. This change in titles is simply a statement of their partnership and shared commitment to Panera.”

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

COSI: Cosi declined -1.8% on accelerating volume.

CBOU: Caribou gained 4.8% on accelerating volume. Coffee’s price declining is helping the coffee retailers many of whom took price last year to mitigate shrinking margins.

CASUAL DINING

BWLD: Buffalo Wild Wings was cut to Neutral versus Outperform at Wedbush.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

PFCB: P.F. Chang’s gained 3.6% on flat volume. This is the best performing stock in casual dining over the 90-day duration.

Howard Penney

Managing Director

Rory Green

Analyst