Following a disappointing February sales release, MCD spoke at the UBS Global Consumer Conference yesterday and added some perspective to the long term outlook for the company. In particular, investors are asking if momentum is going to be maintained whether or not there are measures the company can take to counteract the negative impact of austerity in Europe on its top line.

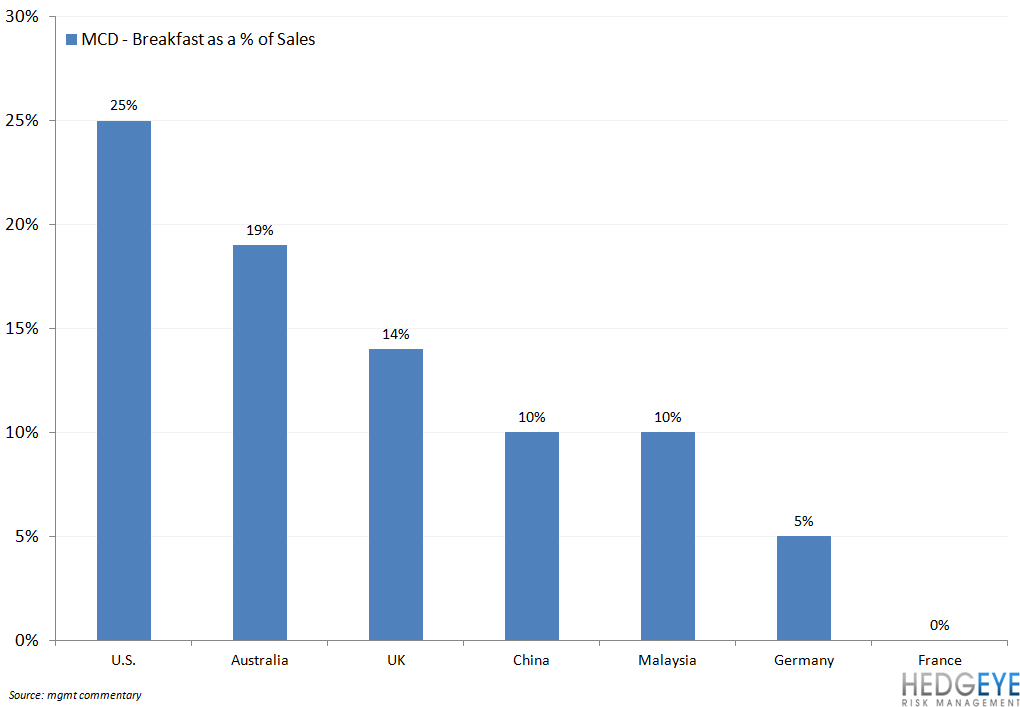

COO Don Thompson spoke to the audience at the conference and the standout comment from him was that “globally, breakfast is a huge opportunity”. Looking at the proportion of sales that breakfast represents in different geographies as a percentage of sales, it is clear that some markets are not leveraging breakfast as much as others.

Below we highlight some of the key topics that were discussed during the McDonald’s presentation yesterday along with our thoughts on several issues for the company.

BREAKFAST, BRAKFAST, BREAKFAST

MCD: “In the U.S., breakfast continues to be strong. Keep in mind as well, in breakfast, we've done a lot of things to make sure that breakfast continue to be a very viable strength for us, everything from operational changes and organizational changes in the restaurant to the products, to the breakfast value menu, even to the percentage of products relative to McCafés that are sold at a breakfast timeframe, albeit lower, still accretive to the overall sales at breakfast.”

HEDGEYE: The biggest issue facing the breakfast day part for all operators is employment. Increasing frequency in the breakfast day part on a global basis is important for the continued growth of the company. In the end, cultural differences may limit the ultimate potential of breakfast in international markets and the levels seen in the U.S. may not be an appropriate yardstick to measure success. However it is clear that the company is seeking to export its success in breakfast to other markets where possible.

THE STATE OF THE CONSUMER – TRAVEL BUNDLING

MCD: “When gas prices become elevated consumers do some things we call ‘travel bundling’… so rather than go out four or five times, one to go to the grocery, one to go to the cleaners, one to go someplace else, they tend to do a bundle and they'll make one travel path and get all three or four of those things done.”

HEDGEYE: Consumers are stretched and behavior is changing to better enable navigation of inflation, stagnant wage growth, and economic uncertainty. MCD’s stock performance is not as tightly correlated to initial jobless claims (inversely) as other restaurants but breakfast, especially, would be aided by employment gains and consumer uncertainty would be assuaged by a continuation of positive macro-related headlines. For the company’s side, management is focusing on the marketing message and paying close attention to its consumer’s behavior.

EUROPEAN CONSUMER COMMENTARY

MCD: “Some consumer confidence issues clearly around the world based up on the economies, but you have variances around the world. When you are in the U.S., we typically say whether U.S., Europe, Asia, well there is no country called Asia or Europe and so when you look at the various markets you see different things. So as an example in Europe, if I looked at a markets like the U.K., markets like Russia, tremendous growth, the GDP is solid, I mean we're just, we're rolling along. You go to a market like France, markets like Germany, these are markets that now we see consumer confidence weighing in the scales and there is a lot more trepidation.

HEDGEYE: Four companies that we follow have used the word “austerity” in describing risks to their businesses: YUM, MCD, SBUX, and DPZ. Clearly, any consumer-facing business with exposure to Europe faces this risk but on March 8th, MCD became the first company that we cover to state that austerity is having an impact on income growth. Don Thompson including Germany in his commentary above was incremental to our conversation with management following the February sales release. Perhaps Germany is somewhat on the fence but we left the conversation with management last Thursday under the impression that Germany was performing well.

INCREASED VALUE MESSAGE IN EUROPE

MCD: “There were two adjustments made in two of the major markets yesterday and the day before yesterday. And by adjustments what I mean, for us what an adjustment means is an opportunity we get with the franchisee base to talk about where we position in the marketplace and what lever we may need to pull more … So but some adjustment may be we've got bring in this new platform because things are bad now it just means we may do a little shifting … crank up certain messages a little bit more. We may focus a little bit more on P&L optimization efforts at a restaurant level as we stress value a little bit more in certain markets.”

HEDGEYE: Given that Don Thompson met recently with operators in Italy, Spain and France, we would be confident that those two markets mentioned above are two of the three he visited. All three markets have been struggling of late and McDonald’s needs to crank up the value message to improve traffic trends.

MORE ON EUROPE AND REMODELS

MCD: “We have 50% of our exteriors done in the U.S. versus 90% in Europe. In Europe they still have a way to go on exteriors. We will be close to 100% of all the sites that we've identified that we want to do by the end of 2012.”

HEDGEYE: In 2012, we are anticipating a slowdown in two-year average trends in Europe. Clearly the European market has also benefitted from remodels and the company selling premium products. The conclusion of the remodeling program and the result now-impactful austerity measures could nullify these positives.

For the majority of 2011, the two-year average trend for MCD’s Europe comps was just above 5%. McDonald’s has said that in the past that the remodel program has boosted sales by 6-7%. Heading into 2012, 85% of stores in Europe are remodeled. This program has allowed McDonald’s to increase capacity via the drive through, in particular, but the new look and feel has also enabled the company to sell more premium products.

INFLATION IN GROCERY AISLE IS GOOD FOR MCD

MCD: “I think the projection for 2012 is for the grocery store prices, the food at home to moderate a little bit in the maybe 4% to 5%, 3% to 4% range and food away from home to be more like 2% to 3%. So that gap is closing but the projections are still for the grocery stores to be a little higher. If that means for us, our back store cost won't increase as much, that's a good thing.”

HEDGEYE: As our chart below illustrates, the spread between food at home CPI and food away from home CPI has been narrowing over the past four months. If the trend over the last four months were to continue, assuming the average rate of narrowing since the spread stopped widening, by the end of the second quarter the spread would be closed. While this is not a foregone conclusion, it is important to note that – on the margin – the gap has been closing and offering less of a competitive advantage to restaurants versus grocery stores. CPI data released tomorrow will update us on this trend.

Howard Penney

Managing Director

Rory Green

Analyst